4Q24 Commentary: Priced for Perfection – S&P 500 Increasingly Dependent on the AI trade

January 21, 2025 | TIMELY PM UPDATES

2024 was a spectacular year for U.S. equity indices, but only a normal one for the typical stock which pulled back appreciably in December. Headline equity performance continued to be driven by the very largest of, primarily U.S., Technology companies. Increasing prospects of a “soft landing” in the economy as well as enthusiasm over AI technology encouraged overall investor optimism throughout the year.

After the U.S. election, this optimism boiled into something more akin to speculation as Trump’s firm victory ushered in the prospect of potentially lower taxes and less regulation. The prices of cryptocurrencies surged as did those of the most speculative companies, such as tiny firms engaged in the far from economically viable technology of quantum computing. These companies saw their share prices increase anywhere from 5 to 20 times in a matter of weeks[1].

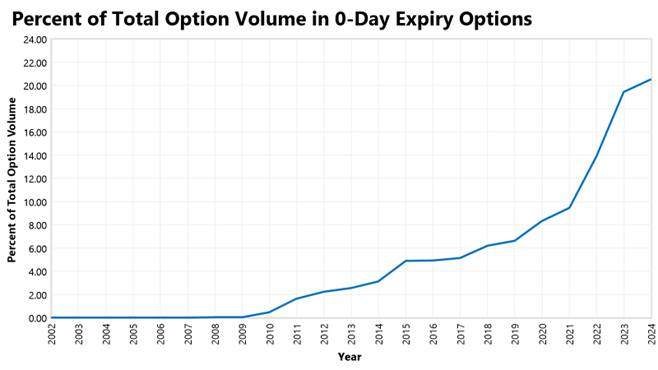

We’ve spoken about the gamification of markets at times over the past 5 years and continue to believe it has created material distortions in parts of the market as retail trading remains extremely accessible and popular. The financial industry has sought to capitalize on this with the proliferation of 0-day options and the release of cryptocurrency and single stock levered ETFs[2]. This type of “innovation” is often a tell-tale sign of speculation just as the wave of SPACs and IPOs proved to be at the end of 2020 into 2021.

Source: Algorithmic Investment Research, retrieved from Delta Neutral Historic Option Data for dates 1/1/2002 to 12/31/2024

The current backdrop is highly reminiscent of 2021, and we believe 2025 might look a bit like 2022, albeit with some mitigating factors:

- Stocks look expensive and have done anomalously well.

- Broad speculation has returned to markets and investors are very bullish.

- Inflationary pressure may be upward.

A major caveat to 2025 looking like an echo of 2022 is that we are now starting from a modestly restrictive monetary stance, which makes a historically large “yield shock” unlikely. However, if inflation remains a bit higher than desired, we may see minimal rate cuts and a directionally similar reaction in global markets – with pro-inflationary assets doing relatively well and overall diversification paying off versus top-heavy market cap indices.

None of this is to say the current economy looks weak, but we believe it is unlikely to improve further. Stocks appear uniquely risky due to how highly concentrated, correlated and priced for perfection the largest companies are. 2022 was a poor year for equities, and all cash flowing assets, but it was not a poor year for economic growth or unemployment.

Portfolios

We find ourselves entering another year positioned in a relatively contrarian manner. The Growth, Moderate and Conservative portfolios hold at or marginally above expected levels of equity. However, those equities are decidedly more diversified and arguably defensive compared to the large cap indices. Over the year, our models moved away from the equity market leaders and into the laggards, with an acute change near the end of the second quarter when we took a concentrated bet in the financial sector. At the beginning of the third quarter, this positioning was rewarded as Powell’s dovish comments temporarily reversed the trend of large-cap growth outperformance.

Unfortunately, our portfolio’s diversified positioning was not additive within the 4th quarter as we saw a very large spread between the largest Technology companies and the rest of the market indices, particularly in December. The S&P 10[3] returned 3.62% in December while the average S&P 500 stock lost 6.28%.

For the year, each of our portfolios exceeded the performance of their risk-weighted universe and the Conservative portfolio exceeded the performance of both its risk-weighted universe and its target benchmark. The Growth portfolio delivered a double-digit return on the year, while the Moderate and Conservative portfolios returned mid to high single digits. The portfolios faced a large headwind compared to capitalization weighted benchmarks, as the average equity ETF in our investment universe returned just 10.12% on the year versus 18.03% for Global Stocks (ACWI). While our positioning could change and bring us back into growth-oriented equities, as we have been for the majority of the last 5 years[4], we are optimistic that 2025 will be a year in which other equities provide a tailwind for relative performance rather than a headwind. If 2025 does indeed look similar to 2022, our current positioning would likely be advantageous.

Some new themes which are emerging or re-emerging within our rankings are energy-related equities, which stand to benefit in a more inflationary or more geopolitically tense environment; financials, which stand to benefit from a more accommodative regulatory environment; and China. While there is certainly risk with China, we see some potential opportunity and it is possible investor sentiment has begun to turn more positive[5]. Whether or not that becomes a long-standing position in our portfolios remains to be seen, but it will be an interesting development to watch in 2025.

Will Diversification pay off in 2025?

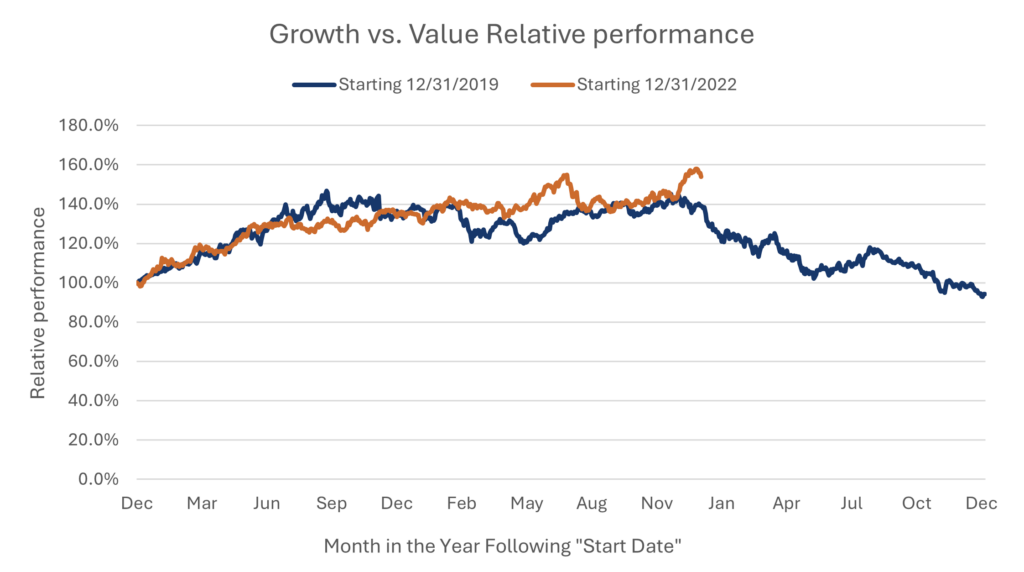

2022 brought a reversal to the extreme outperformance of growth over value that occurred following the pandemic. While it’s common knowledge that fixed income performed poorly, it’s less well known that lower-risk equity sectors, the average sector, and the average S&P 500 stock all outperformed the index after lagging in 2021.

The path of growth substantially outperforming value over the past two years looks eerily similar to the one that preceded 2022.

Source: Bloomberg, 12/31/2019 through 12/31/2024. Value is represented by CRSP US Large Cap Value TR Index and Growth is represented by CRSP US Large Cap Growth TR Index

Upon closer examination the recent “surge” in relative outperformance of growth versus value to end the year mirrors the one that ended the second quarter of 2024. Our system is likely to have repositioned away from growth-type equities in both cases as it often tries to sell anomalously strong short-term performance.

Although the Magnificent 7 (Mag-7) companies seem unstoppable, having yet to materially participate in the recent December pullback, “the generals often get shot last” and that was the case in 2022 as well. The Mag-7 ultimately returned -40% in 2022, while the S&P 500 lost just 18% despite these stocks performing roughly in line with the market through the first 10% of the market drawdown[6].

We are increasingly in a thematically driven market, and the general theme of AI binds almost all the largest companies in the world at the moment. This has allowed them to prosper in unison, but it also creates a substantial risk should something derail that theme in 2025. While most indications are that the largest technology companies intend to keep the pedal down on AI-related spending, there is some evidence that models are not improving at the same rate[7], implying that more computing power doesn’t necessarily translate directly into better models – a key tenant known as “scaling laws” which has driven progress and investment fervor thus far. While we view this predominantly as a market risk specific to this subset of companies, rather than an economic one, the immense capital spending towards infrastructure to support this technology has been a tailwind to the general economy thus far.

While we expect AI will continue to be integrated into computation and generally improve overall productivity, we believe the results will be gradual – an evolution rather than a revolution. The pace of spending within the technology industry appears more “urgent,” which we believe presents a significant risk to the sustainability of its current growth trajectory in the near term.

Economic Outlook

The economy looks relatively strong, albeit with unknown potential new policy impacts. Our view is that the stock market is more at risk in the near term than the broad economy. That said, the prospect of less fiscal support (via curtailed government spending) and a relatively weak lower-end consumer is likely to offer more downside risk to growth than upside.

The wealthiest consumers in the U.S. have arguably never been better off with the recent massive appreciation in both equity and real estate values. We have long believed that the U.S. has increasingly become a more wealth-based economy:

- A combination of deleveraging post 2008 and rising asset values has allowed assets to appreciate far faster than incomes.

- An aging society has less income as a percentage of wealth and spends against wealth in retirement.

- Wealth is more transparent than ever with real-time housing and stock prices accessible anywhere via mobile phones.

In the near term this should continue to boost the general economy but may present an economic risk if equity markets falter. If mortgage rates remain elevated and homeowners decide or need to start listing their homes, this could create negative price discovery for homes as well. Homebuilders, the marginal suppliers of homes, have already cut prices substantially and their inventories are increasing[8].

Upside Risks to Inflation

While inflation looks relatively subdued, with most of the above target contribution due to lagging prices of housing and insurance, inflationary pressures could resume depending on how fiscal policy evolves in 2025. On the surface, tariffs and lower taxes would be inflationary, while reduced government spending would be deflationary. However, many potential changes have off-setting impacts. If demand is relatively sensitive to price for goods, higher tariffs may simply cause consumers to buy less in aggregate, leading to a larger impact on growth than inflation. While over time smaller government, if it can be achieved[9], may have positive benefits for the economy, in the near term it is likely to have a negative impact on overall consumption from job or income losses. Regardless of how the effects net out, we see short-term risks from potential changes in policy against an otherwise relatively healthy economy.

We continue to believe any remediation of the very significant fiscal debt and deficit would require painful consequences. In much of the developed world sovereign debt levels have become a larger focus, and the United States may be heading in that direction as well.

China

While domestic investors continue to gyrate on whether or not China is “univestable”, China’s contribution to the global economy remains substantial.

China is currently facing the aftermath of a real estate bubble, akin to our own in 2008, in which prices have fallen nearly 20% from peak. This, combined with the government’s heavy-handed pandemic restrictions, has crushed consumer confidence. Consumers are hoarding cash rather than spending and investing, and it has substantially curtailed overall economic growth.

Despite weak consumption, China’s centrally planned economy has funneled capital to high growth industries such as electric cars, AI and clean energy. In many of these new industries, China appears to be competitively advantaged, further cementing its importance in the global economy.

The U.S. governments recent and ongoing trade restrictions on advanced technologies have the potential to backfire if they encourage China to become self-sufficient in these technologies. While providing a near-term boost to U.S. competitors they may unintentionally incubate future stronger Chinese competition in addition to diminishing growth opportunities inside China for dominant U.S. firms. It will likely prove difficult to prevent U.S. and European consumers from buying cheaper, better products long-term (from China or elsewhere) – capitalism will find a way.

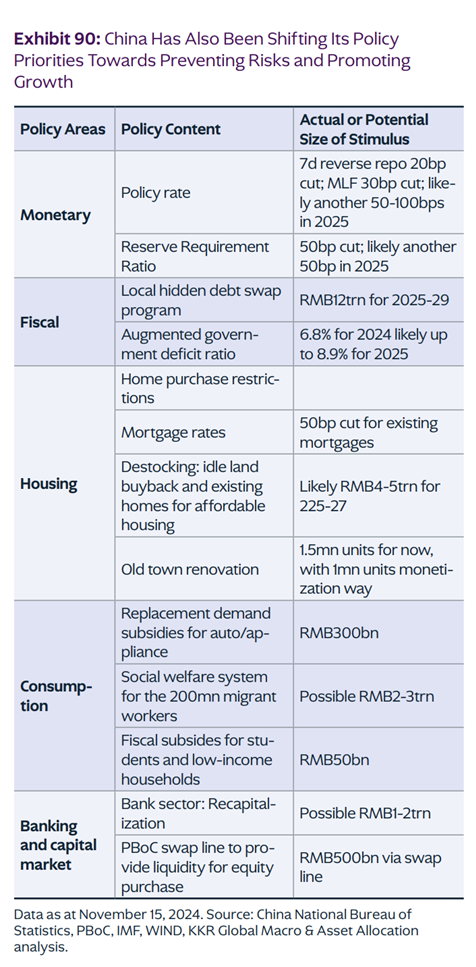

While their economy presents major current challenges and will need ongoing monetary and fiscal stimulus to re-ignite consumers spending, it appears as though this process has begun. While it is unclear how long it will take, Chinese stocks are historically cheap and in attempts to signal financial strength, the largest, most foreign-owned equities are now returning large amounts of capital to investors via dividends and buybacks.

While thus far the Chinese government’s attempts at re-igniting consumer growth have been insufficient, the list of projects is large and expanding.

Historical Perspective

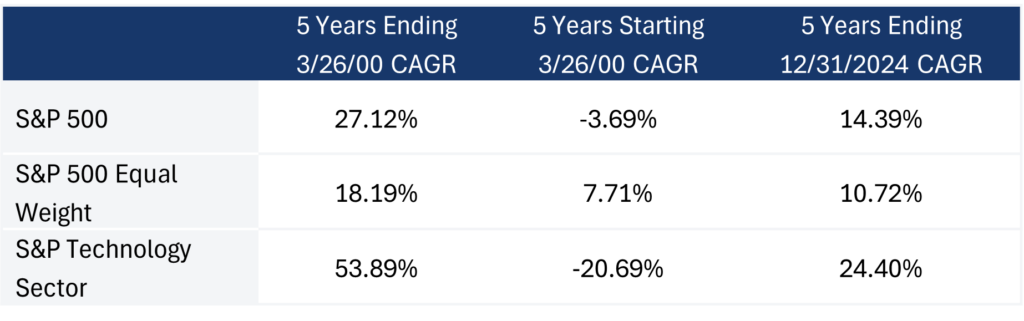

It is tiresome to continue to point out the narrow market leadership and the risks it presents to passive investors, or holders of the S&P 500, but history has shown that diversification does end up “paying off” in the end. One of the largest and increasingly relevant example is the late 90’s technology bubble. As the chart below shows, technology companies (then far smaller with more potential appreciation from size alone) drove the market. Indices became concentrated and market-cap weights substantially outperformed the average stock – no surprise there. Most investors think of the ensuing years as terrible ones for equities as the major U.S. indices yielded negative returns.

Source: Bloomberg, total return index for 3 separate date ranges. 3/26/1995-3/26/2000; 3/26/2000-3/26/2005; 12/31/2019-12/31/2024

However, against the backdrop of a relatively benign economy, the “average” equity did just fine and presented a major opportunity for outperformance against equity indices for the stock picker or the more diversified investor. In fact, many now famous “value investors” likely owe a good deal of their fame and success to this market environment. Our diverse universe of options will give us a “target-rich” environment should 2025 mark the beginning of this “rebalancing”, and if it is not, our models are free to buy as much of the largest companies as they can until that day does come.

[1] For reference the share prices for QBTS, QUBT, IONQ, and RGTI 4 public quantum computing stocks appreciated 692%, 1377%, 178%, and 1056% in the two months starting 10/31/2024 and ending 12/31/2024, with many of the stocks considerably off their highs. Source: Bloomberg

[2] On 11/20/2024 MSTR traded $18.56 Billion in volume, making it the most traded stock in America that day—roughly $1B more than Nvidia which sports a market cap more than 30x that of Microstrategy. In addition, MSTU, an ETF that is designed to replicate the return of MSTR with 2x leverage, was also one of the most traded securities in the market with over $2b in volume! Source: Bloomberg.

[3] The largest 50 companies in the S&P 500

[4] Since expanding our ETF universe in 2023, the top 3 highest ranked average equities in the Growth strategy have been GRID, SOXX and XLK. Since inception XLK has been the highest average ranked security. Source: Rankings produced by Algorithmic Investment Models’ proprietary ranking system that uses machine learnings to analyze patterns in past ETF performance that may be indicative of desired future outcomes.

[5] Fueled by a massive late September rally Chinese equity markets actually outperformed the S&P 500 in 2024, with the FTSE China 50 Index returning 28.95% versus the S&P 500 returning 25.0%. Source: Bloomberg.

[6] Source: Bloomberg. UBS Magnificent 7 index, 12/31/2021 to 12/31/2022. 10% S&P 500 index drawdown occurred between 1/5/2022 and 3/8/2022

[7] Raghavan, Sudarsan. “OpenAI and Others Seek New Path to Smarter AI as Current Methods Hit Limitations.” Reuters, 11/15/2024.

[8] Median home price of new homes sold has declined from a high of $436,400 in March to $402,600 in November. U.S. Census Bureau and U.S. Department of Housing and Urban Development, Median Sales Price for New Houses Sold in the United States [MSPNHSUS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MSPNHSUS, January 2, 2025.

[9] Spending cuts would likely need to come from some combination of healthcare and entitlements, given the narrow margin in the House of Representatives this may prove difficult.

Disclosures:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The S&P 600 Index tracks small-cap U.S. stocks and reflects the performance of smaller companies. The S&P 500 Index measures the performance of 500 large-cap U.S. companies and is widely used as a benchmark for the overall U.S. stock market. The CRSP US Large Cap Value Index includes large-cap U.S. stocks that exhibit strong value characteristics, while the CRSP US Large Cap Growth Index tracks large-cap stocks with high growth potential. The MSCI All-Country World Ex-US Index captures the performance of global stocks, excluding the United States, representing developed and emerging markets. The Russell 1000 Index tracks the performance of the largest 1,000 U.S. companies by market capitalization, representing approximately 92% of the U.S. equity market. The Russell 2000 Index focuses on small-cap stocks, tracking the smallest 2,000 companies in the broader Russell 3000 Index.

For Investment Professional use with clients, not for independent distribution.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC

125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)