The Anatomy of a Bear Market

December 6, 2018 | ECONOMICS & INVESTING

What does a typical Bear market look like? How long do they last? When are the majority of the losses incurred? Most investors believe that the losses occur fairly evenly throughout the Bear. Based on the past, with one notable exception, nothing could be further from the truth.

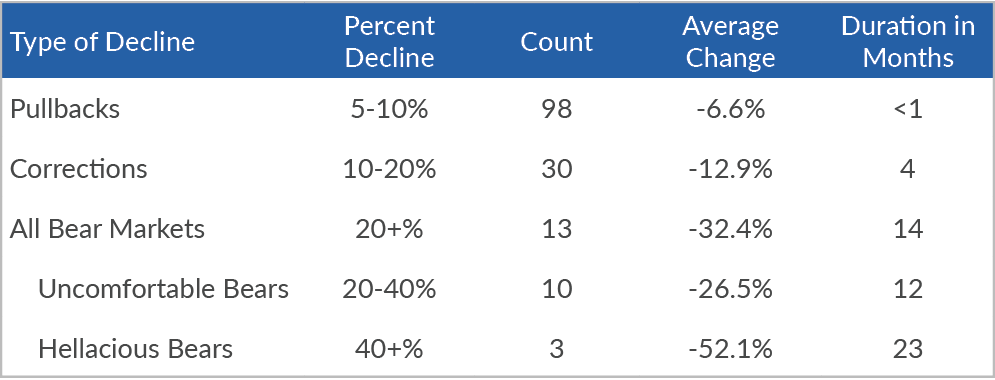

In our last educational paper on Bear markets, Tactical to Practical: Understanding the Importance of Market Declines, we wrote about the types, frequency, severity and duration of market declines. As a refresher, here are the results:

S&P 500® Index Price Declines (Excluding Dividends): 1946-September 2018

Source: Bloomberg, Beaumont Capital Management (BCM). Data as of 9/30/18 and does not include the current drawdown which has not ended.

Now let’s dig into what we really want to talk about: the anatomy of past Bear markets.

First, Black Monday in October 1987 was the exception. The vast majority of the losses occurred in one day; in fact, the 22.6% loss was the largest one-day percentage drop in the history of the Dow Jones Industrial Average. In my opinion, this was truly the first “flash crash” as the computers of the day were selling ahead of their human counterparts. There were no governors or rules limiting the computer trading at the time and this exacerbated the fall. Regardless of the cause, this Bear was unlike any other in the post WWII era.

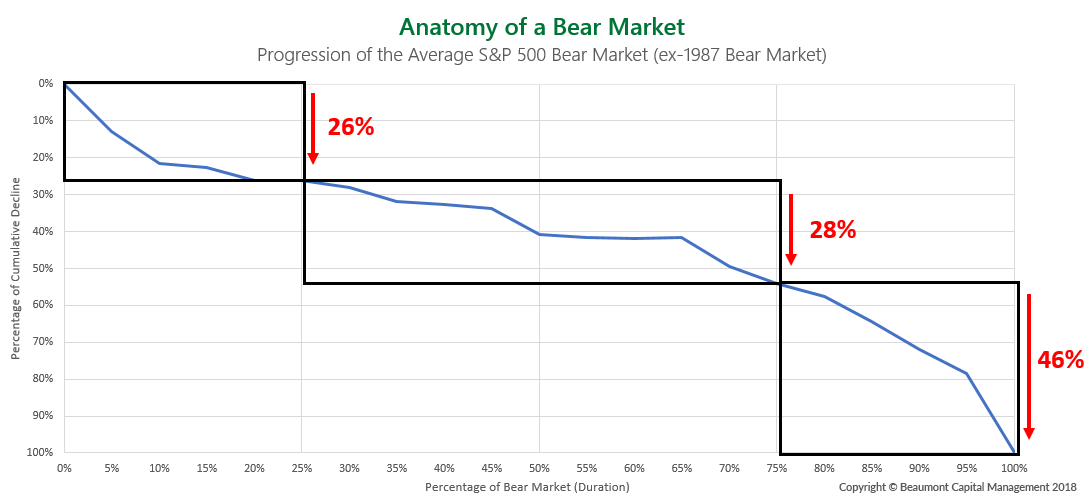

As the chart above shows, most Bear markets take time. It takes a year or two to lose such a large percentage of your portfolio. Yet within this timeframe, the losses are not evenly distributed. The chart below breaks down the average Bear market for the S&P 500 Index. What is striking is that most of the losses occur during the beginning and the end of the Bear, and that the losses occur faster during the beginning and end.

Source: Bloomberg, Beaumont Capital Management (BCM). The chart shows the distribution of losses throughout the progression of the average S&P 500 bear market (with dividends reinvested) since the end of WWII, excluding the 1987 bear market.

Every Bear starts as an ordinary pullback, grows into a Correction and then continues into a Bear. Ordinary pullbacks tend to be sharp and quick, so it makes sense that the beginning of a Bear shares this trait. Of all Bear markets since WWII (except 1987), the first quarter of the Bear market declines ~9% on average, the upper range of the Ordinary Pullback. On average, the first quarter of a Bear will incur about 26% of the total Bear market drawdown (source: see chart source above).

The next phase, or the next half of the Bear including the second and third quarters, is more of a complacency period. Combined, the average losses in this phase is -28%. The Bear takes its time. It pulls you in. There are recovery rallies sprinkled in giving hope. The shallower downward slope does not compel action but by the end of the third quarter the Bear has essentially doubled your loss. Complacency turns to denial. Lots of investors stop opening their statements. And then it happens.

Almost half of Bear market losses, 46% on average, occur during the final panic and capitulation stages of the Bear. During this final quarter, the declines tend to accelerate, and the markets start to cascade down. Even the most resolute investors have doubts. People freeze with fear not knowing what to do, and then most reach their breaking point. Emotions, particularly fear, begin to take control and fear about future goals, such as education and retirement, becoming unachievable grow unbearable (pun intended). Most investors capitulate and sell at or near the bottom.

What is the lesson? Investment math teaches us to keep our losses small. The larger a loss becomes, the greater the gain the remaining assets in the portfolio need just to get back to even.

Source: Bloomberg. Loss shown for S&P 500 Index is based on daily pricing and includes dividends reinvested from peak to trough for the most recent Bear market (time period 10/9/2007-3/9/2009).

Another lesson is to acknowledge the shape of a Bear and the length of time it takes to unfold. As we mentioned above, the first 10% or so is almost impossible to avoid as it is quick and most often just an ordinary pullback. But as losses extend, it is time to re-assess. Taking action before your losses leave the teens is quite easy to recover from as the loss diagram above illustrates. Keep your losses small and don’t be afraid sell into a rally.

So where are we today? Truthfully, no one knows if this is the next Bear or not. But to further illustrate what may happen, let’s overlay the last two Bear markets with the current market action:

Source: Bloomberg, Beaumont Capital Management (BCM). 2000-2002 Bear market dates between 3/24/2000-10/9/2002. 2007-2009 Bear market dates between 10/9/2007 and 3/9/2009.

Of course, every Bear is slightly different but the first 10% drawdowns look mighty similar. And the circles around the capitulation selling are quite obvious.

If this current correction is going to continue, then where are we on the Bear market continuum? We have already lost the first quarter making up the ordinary pullback. It is the beginning of the second quarter. What are you going to do? Freeze or take action? Put another way, it is January third, 2008. If you could go back in time, what would you have done differently?

If you are still fighting indecision, perhaps BCM can help. What if this is the mother of all head fakes? To BCM, it is simple: Follow a rules-based system that is designed to remove emotion. We provide growth systems designed to prevent large, devastating losses. Our systems ebb and flow as the market action unfolds, but without fear and greed clouding decisions, the path suddenly becomes crystal clear.

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)