Debt Ceiling Redux: What Lessons Can Market Participants Learn From 2011?

May 16, 2023 | ECONOMICS & INVESTING

In 2011, the United States was rapidly approaching its debt ceiling—the legislative cap on the total amount of debt that the U.S. government can incur to finance its operations. The debt ceiling at that time was set at $14.3 trillion[1], and the Treasury Department projected that it would be reached by August.

The Republicans, who had gained control of the House of Representatives in the 2010 elections, demanded significant spending cuts as a condition for raising the debt ceiling. They argued that reducing government spending was crucial for long-term fiscal stability.

On the other hand, the Democrats, led by President Barack Obama, insisted on a balanced approach that included both spending cuts and revenue increases through tax reforms. They warned that failing to raise the debt ceiling would have severe consequences for the U.S. economy and could potentially trigger a default on the country’s financial obligations.

Sound Familiar? History may not repeat but it often rhymes. After several weeks of intense negotiations and heightened tensions, a last-minute deal was reached on August 2, 2011. The Budget Control Act of 2011 was passed, which raised the debt ceiling by $2.1 trillion and included provisions for spending cuts over the next decade.

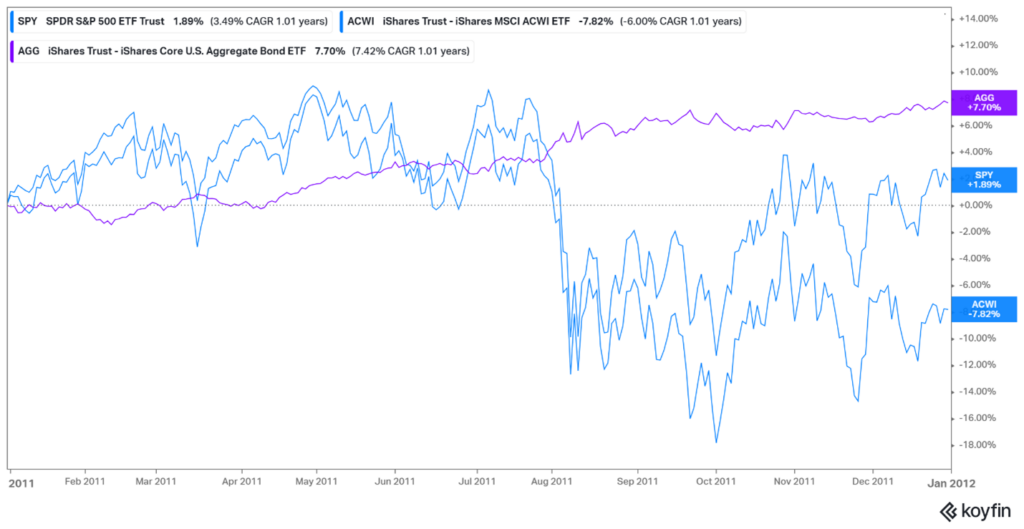

Although the crisis in 2011 was eventually averted, the stock market experienced significant volatility. The chart below shows the price action of the SPY, ACWI, and AGG ETFs. Note the sharp drop beginning at the end of July when the debt ceiling negotiations approached, and eventually reached, the deadline. Interestingly, 10% of the SPY ETF’s 16% decline between July 22nd and August 8th occurred after the Budget Control Act had been passed. By the end of the year, U.S. markets had mostly recovered while international markets, facing their own issues, remained depressed.

Source: Koyfin. Data from 12/31/2010 through 12/31/2011.

Another exercise that we find insightful is to sort the ETF universe that we use to implement our Decathlon strategies by forward return, what we call the “Perfect Knowledge” rankings. The Decathlon ETF universe contains just over 130 ETFs from every major asset class, and roughly 120 of these ETFs have price history spanning back to at least 2011. The “Perfect Knowledge” rankings reveal the best ETFs to own for the month following each of the dates below, allowing us to examine what would have been the best places to be at a more granular level.

Source: AIM, Bloomberg. ETFs ranked by total return for the month following the date indicated in the table.

In July 2011, when the debt ceiling was being negotiated, it was best to own long term treasury bonds, inflation protected bonds, and precious metals (gold and silver). It was essentially a “fear” portfolio. Owning Gold and Silver became sub-optimal immediately after the resolution of the debt-ceiling crisis.

It’s certainly interesting to know what was best to do in hindsight, but the future is rarely a carbon copy of the past. In 2011 Europe was struggling with a double-dip recession and a banking crisis of its own. There was worry that the U.S. would fall into a double-dip recession as well at a time when the unemployment rate was still over 9%[2]. Today’s banking issues pale in comparison to those of the Financial Crisis, and labor markets are tight across the globe. Additionally, unlike politicians, markets learn lessons from the past and often react differently when similar events occur in the future.

Historically, increases to the debt ceiling have been fairly routine. Since 1960, congress has increased the debt ceiling seventy-eight times[3]. Another potential outcome is a suspension of the debt ceiling. While comparatively rare historically, congress has suspended the debt ceiling seven times since 2013[4].

Ultimately, we believe both parties will reach some form of settlement to avert default. The United States faces no near-term spending constraints and refusing to fund our near-term obligations would be incredibly foolish. The current Federal deficit is unsustainable, but reforms should take place during the budgeting process, not by refusing to pay when the bill comes due.

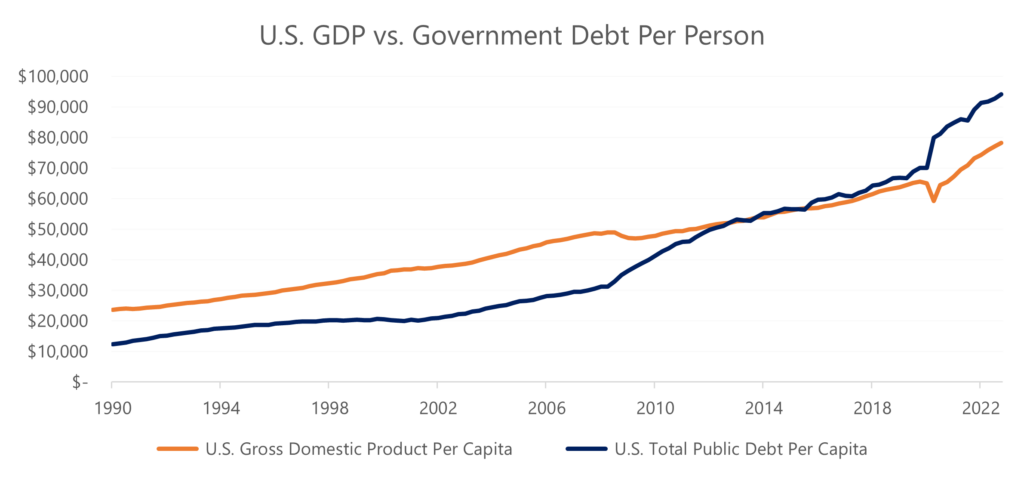

Source: Federal Reserve Bank of St. Louis (FRED), U.S. Department of the Treasury, U.S. Bureau of Economic Analysis. The following data series were retrieved from FRED on May 11, 2023: Federal Debt: Total Public Debt, Gross Domestic Product, Population. Data from 1/1/1990 through 12/31/2022.

We hope this analysis is helpful. We continue to be encouraged by the resilience of the U.S. economy in the face of one surprise after another. We also believe investors are very cautiously positioned (hunkered down) in 2023, making for a favorable risk-reward ratio for thoughtfully selected equity sectors.

[1]https://www.cfr.org/backgrounder/what-happens-when-us-hits-its-debt-ceiling

[2] https://fred.stlouisfed.org/series/UNRATE. Data as of August 2011.

[3] https://www.cfr.org/backgrounder/what-happens-when-us-hits-its-debt-ceiling

[4] https://www.cfr.org/backgrounder/what-happens-when-us-hits-its-debt-ceiling

Copyright © 2023 Beaumont Capital Management LLC.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are those of the author and are subject to change based on market and other conditions. Information presented in this report may be based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.