Services Finally Feeling the Drag of the Manufacturing Contraction, and U.S. CEO Confidence Hits a Decade Low

October 4, 2019 | FIRESIDE CHARTS

While we digest today’s job’s report (50-year unemployment low, 136,000 jobs added, lower-than-expected wage growth—it’s a lot of data), take a look at some of the other major economic trends we’ve had our eyes on this week:

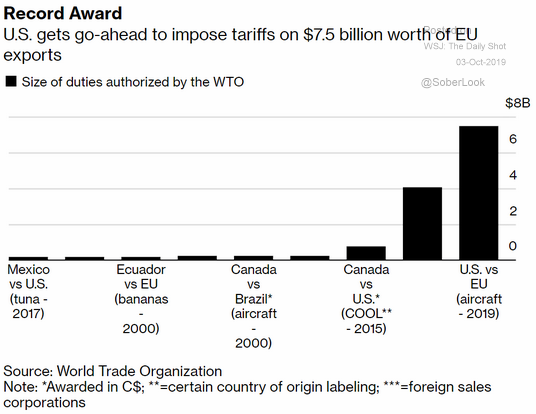

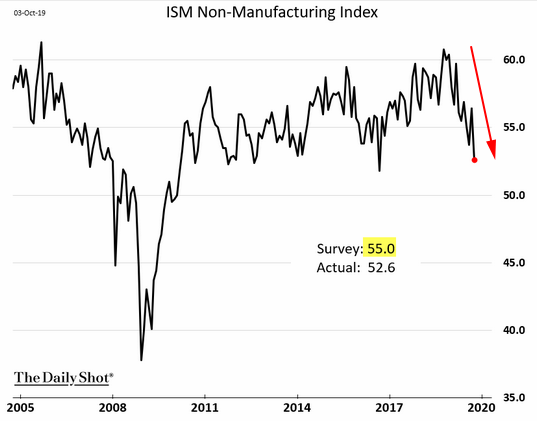

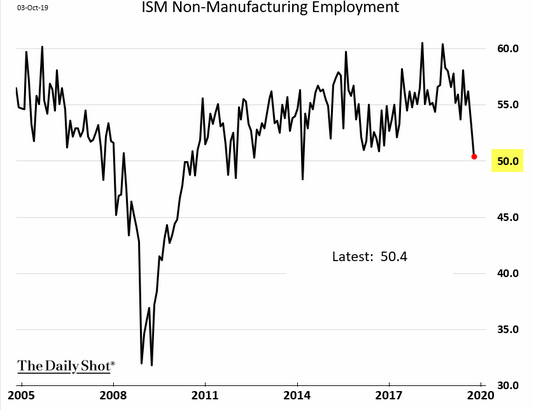

The trade war spread deeper into Europe this week as the WTO approved tariffs on $7.5 billion worth of EU exports on Wednesday. This comes in the same week that the organization slashed their forecast for global trade growth and attributed it almost entirely to the trade war—should we expect another revision lower when they meet again? And ISM data is still a hot topic this week as analysts turned their eye to the services sector yesterday: while manufacturing employment is firmly in contraction, non-manufacturing employment isn’t far behind at 50.4, and the non-manufacturing ISM index missed expectations at 52.6—a 3.8% MoM decrease and its lowest level since August 2016. Sorry folks, but it appears that the weakness in U.S. manufacturing that we’ve long been monitoring is finally bleeding into the broader economy… which we will discuss more in our quarterly commentary to be posted next week.

1. Here we go again… more tariffs on more countries. Europe is already a victim of the U.S.-China tariff trade war and now we open another direct assault?

Source: Bloomberg, as of 10/2/19

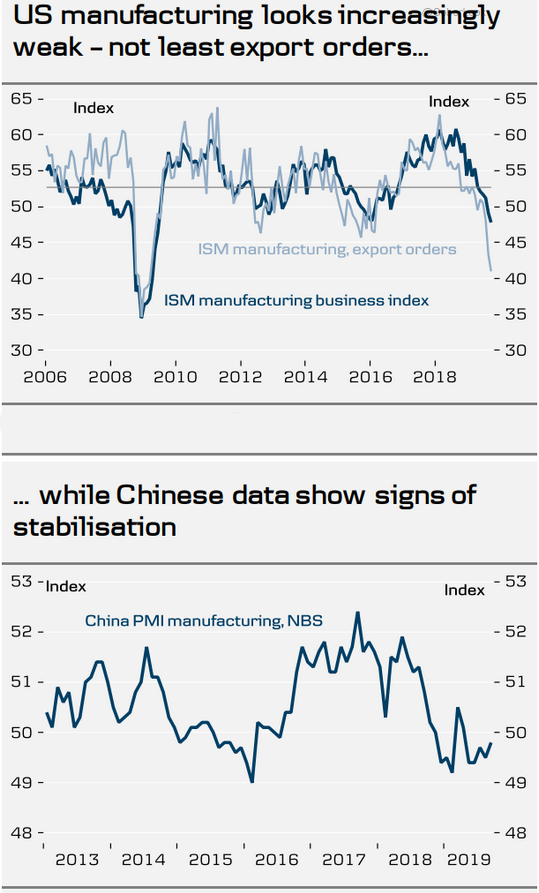

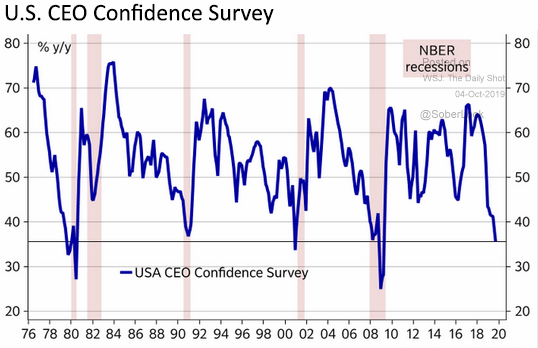

2. It appears the U.S. economy is getting the worst of the trade war…

Source: WSJ Daily Shot, as of 10/3/19

3. We have focused our concerns on manufacturing, but now the effects of the trade war appear to be affecting services and other areas of the economy. Will this trend continue?

Source: WSJ Daily Shot, as of 10/4/19

4. As we wrote in our quarterly letter—which will be posted to the blog next week—after a yield curve inversion, the coincidental indicator of a pending recession is an uptick in unemployment. The data from today’s job report will be crucial!

Source: WSJ Daily Shot, as of 10/4/19

5. Another data point; should we start preparing for an inevitable recession?

Source: Macrobond and Nordea, as of 10/4/19

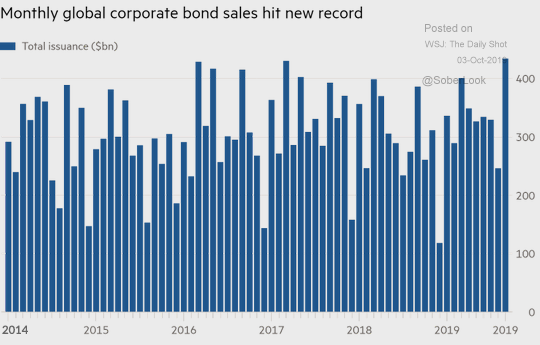

6. Given the low rate environment, this is not surprising…

Source: Financial Times, as of 9/30/19

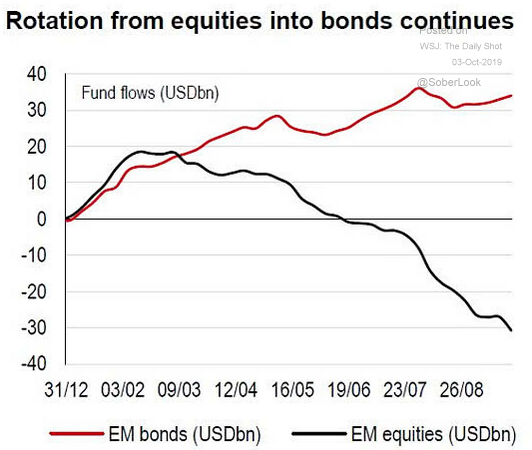

7. EM investors have been voting with their feet!

Source: IsabelNet, as of 10/1/19

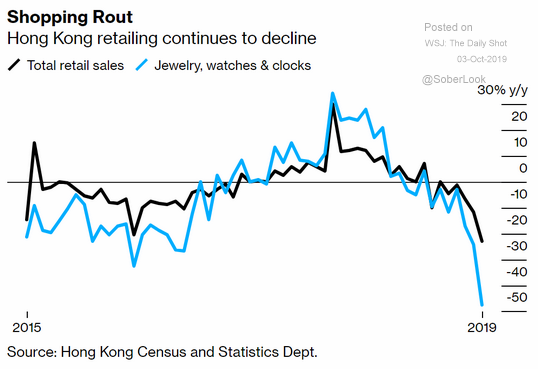

8. It is hard to go buy luxury goods when there is daily rioting in the streets…

Source: Bloomberg, as of 10/1/19

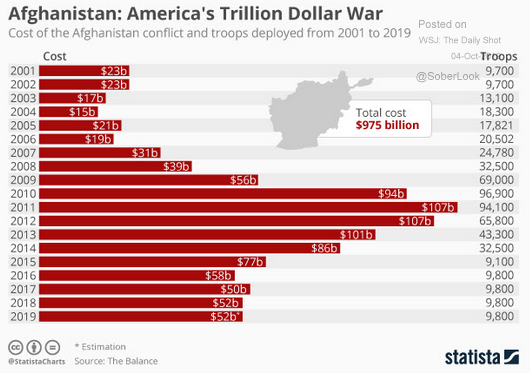

9. Was Charlie Wilson right? Imagine if half of this was spent on rebuilding infrastructure, schools, etc.

Source: Statista, as of 10/4/19

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)