Soft Retail Sales Spark Concern About the U.S. Consumer, and Has the End Come For the 60/40 Portfolio?

October 18, 2019 | FIRESIDE CHARTS

U.S. retail sales dropped unexpectedly in September for the first time in seven months in what many analysts consider an early sign that the global manufacturing slowdown and trade war anxiety are finally starting to weigh on consumers (re: the driving force behind ~70% of the U.S. economy). Is this a blip—especially given that numbers are still up YoY, unlike Industrial Production—or the onset of a new pattern? Treasury yields dipped slightly following the soft retail numbers, but seem to have stabilized, and yields are starting to rise in Europe despite ongoing weakness. Are the positive Brexit headlines to thank? And speaking of bonds: the recent volatility, shifting relationship between asset classes, and growing correlation between bonds and equities lead Bank of America to declare “The End of the 60/40″ Portfolio”—the title of a research note published this week that argues investors should shift their allocations more fully towards equities and “reconsider the role of bonds in [their] portfolio.” Could this mark the end of an era in financial planning?

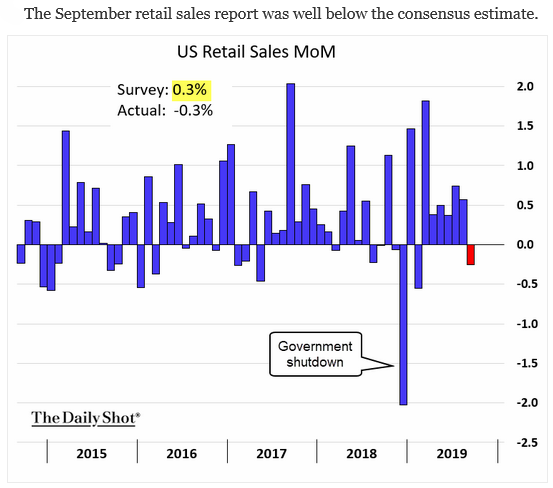

1. September retail sales missed expectations and dropped for the first time since February.

Source: WSJ Daily Shot, as of 10/17/19

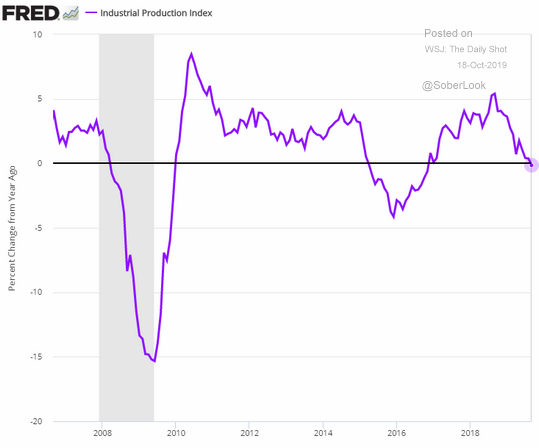

2. Yesterday saw the U.S. Industrial production disappoint to the downside and it is now negative on a year over year basis.

Source: WSJ Daily Shot, as of 10/18/19

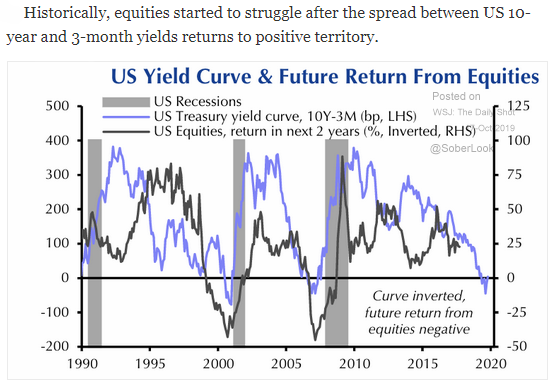

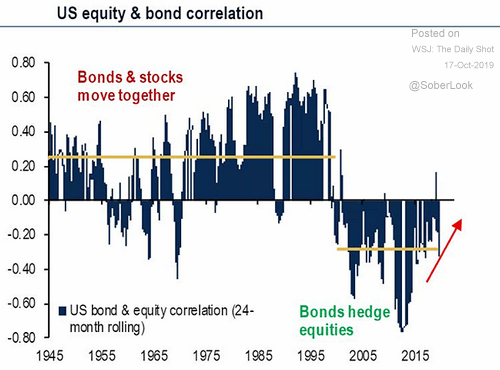

3. Are we nearing a watershed moment?

Source: Capital Economics, as of 10/17/19

4. If the current trend continues, bonds will be less likely to moderate equity volatility and returns. Will MPT, the concept of diversification, and a 60/40 portfolio still work?

Source: BofA Merrill Lynch Global Research, as of 10/16/19

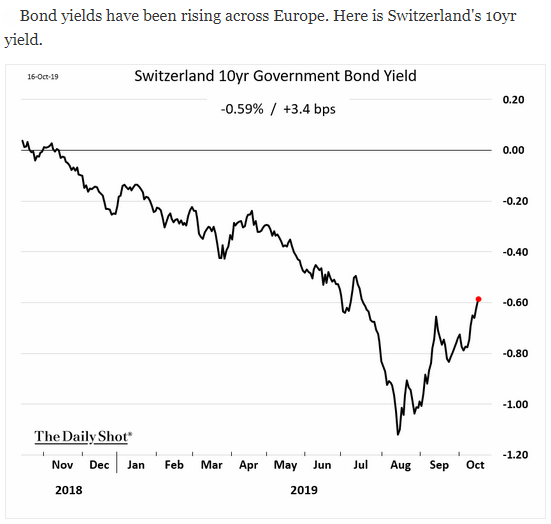

5. Most still have negative yields…

Source: WSJ Daily Shot, as of 10/17/19

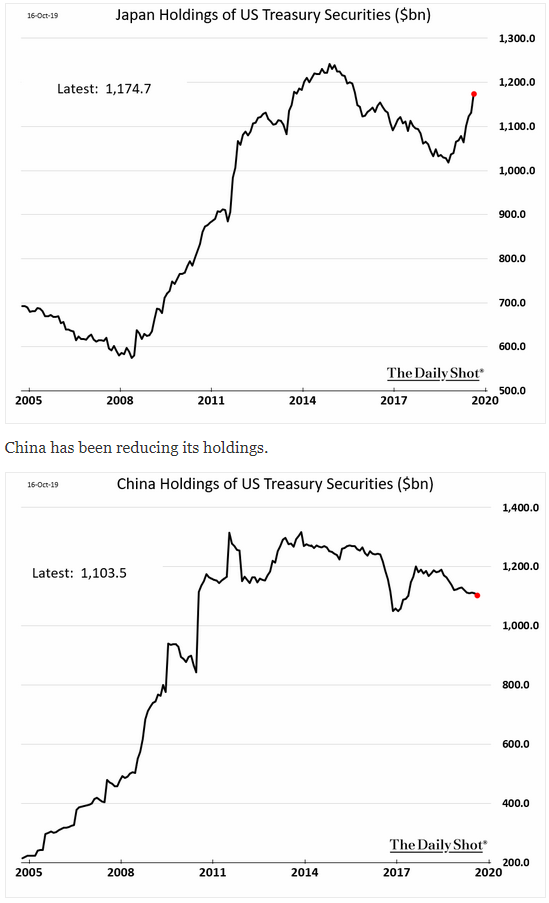

6. An update on two of the largest foreign owners of U.S. Treasuries:

Source: WSJ Daily Shot, as of 10/17/19

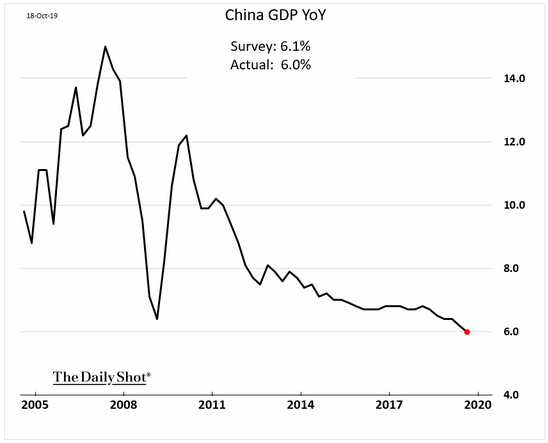

7. China’s GDP continues to slow. Do you trust their data?

Source: WSJ Daily Shot, as of 10/18/19

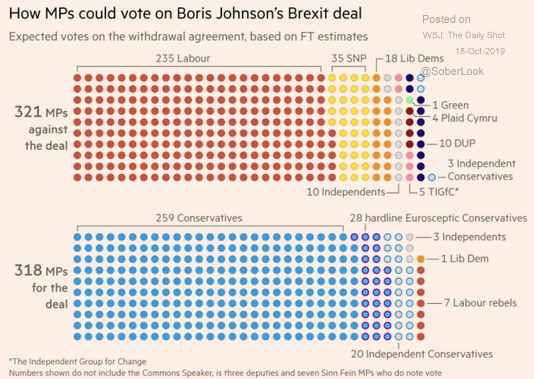

8. Now, if they can only get this deal through Parliament… an uncertain prospect at best as PM Johnson has no majority…

Source: CNBC, as of 10/17/19

9. The U.K.’s Financial Times is predicting a loss. Wouldn’t it be nice to just have this end?!

Source: Financial Times, as of 10/17/19

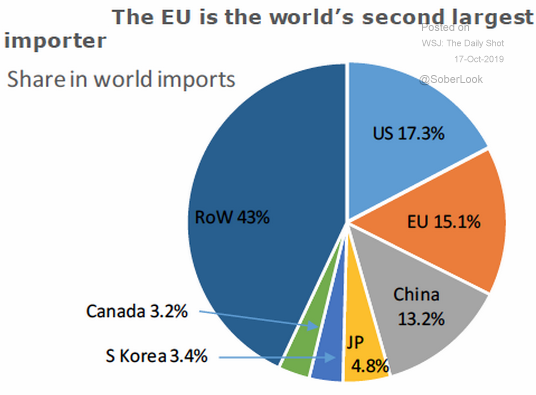

10. Germany and the rest of Europe account for 15% of the world’s imports…their growth slowdown affects us all!

Source: ANZ Research, as of 10/17/19

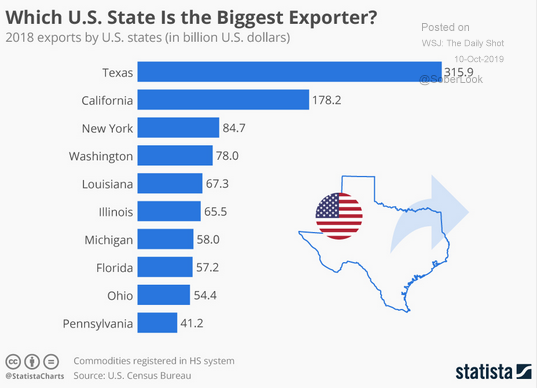

11. And a look back at U.S. exports in 2018:

Source: Statista, as of 9/25/19

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)