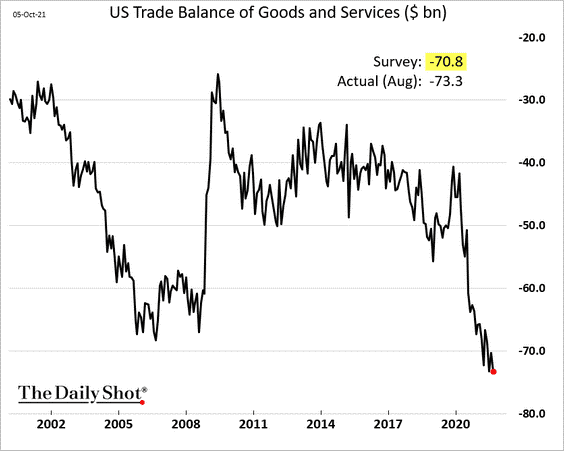

The $73.3 Billion Trade Deficit, Surprising Payroll Gains, and Skyrocketing Commodity Prices

October 7, 2021 | FIRESIDE CHARTS

Despite a strong recovery in manufacturing activity, the U.S. trade deficit climbed to a record high of $73.3 billion in August. Sentiment is already split on what to expect from Q3 GDP, and a complex labor market is unlikely to be much help. The ADP payroll report surprised to the upside with gains in all primary sectors in September, but worker expectations—and their conditions for returning to work—have changed. And how will the shocking number of workers who retired completely during the pandemic affect economic growth going forward? Meanwhile, it’s no secret that equities have grown more volatile in recent weeks, but how does index composition affect investor experience of market swings? And the debt ceiling reprieve and surprising strength of the ADP report helped steady stocks after losses earlier in the week, but will it be enough to carry them through an uncertain earnings season? Finally, inclement weather and persistent supply chain disruptions have sent the price of cotton, natural gas, and shipping skyrocketing. How long will it be until true inflation follows suit?

1. USD strength has other contributing consequences. Our trade deficit hit a new record:

Source: The Daily Shot, from 10/7/21

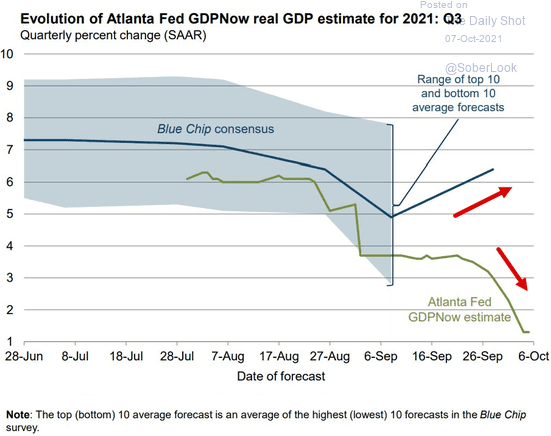

2. So who is going to be right? (Hint: they both are often wrong!)

Source: The Daily Shot, from 10/7/21

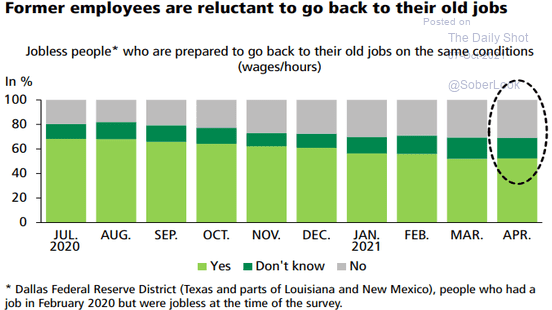

3. While job openings are near records, the ADP jobs report was strong (again, often inaccurate), and the surplus unemployment benefits have ended, many Americans are reluctant to return to work:

Source: Dallas Federal Reserve, from 10/7/21

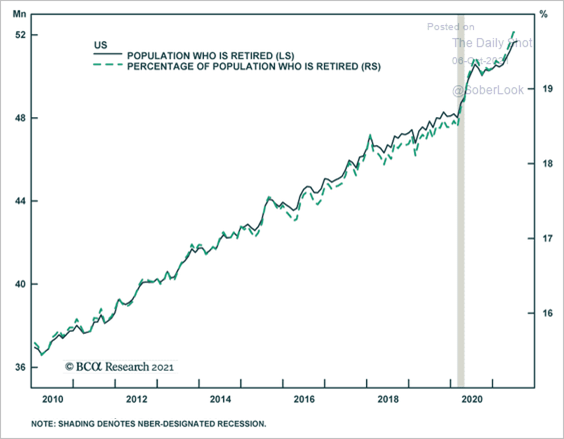

4. “OKaaaay, boomer!” Time to chill! Covid induced ~4 million boomers to retire. Seriously, aging demographics will be a headwind much like the 1970’s.

Source: BCA Research, from 10/7/21

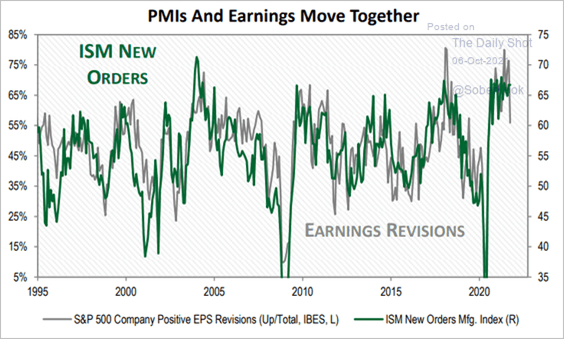

5. Will the moderation in the PMIs lead to a moderation in earnings?

Source: The Daily Shot, from 10/7/21

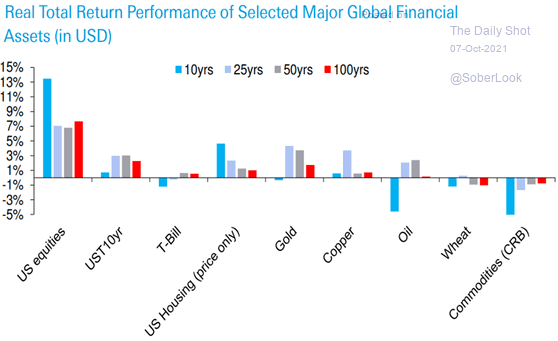

6. Remember, whenever someone says “This time it’s different”, the markets remind us it is not so. When the 10-year U.S. equity return is about twice the 25-, 50- and 100-year returns, we stop and wonder what is next.

Source: Deutsche Bank Research, from 10/7/21

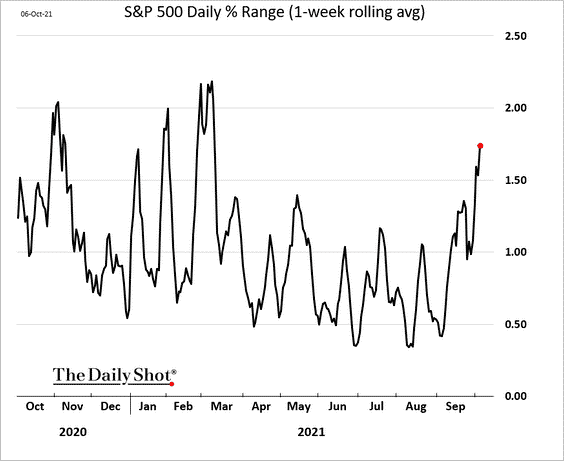

7. Stock market volatility is increasing:

Source: The Daily Shot, from 10/6/21

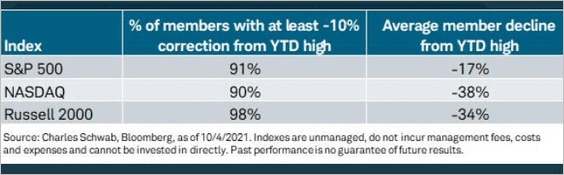

8. The market cap weighting of these major indices “hides” the underlying magnitude of the recent pullback/correction/bear:

Source: Charles Schwab from 10/7/21

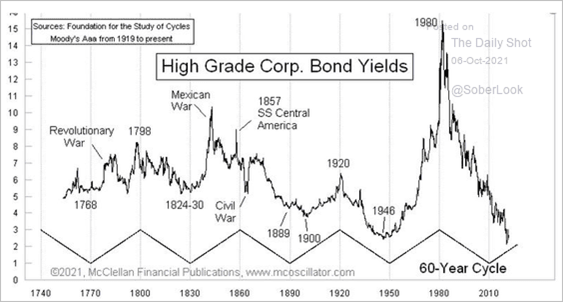

9. Bond macro-cycles are longer than most working careers. Most research and bond “wisdom” ignores these cycles:

Source: The Daily Shot, from 10/6/21

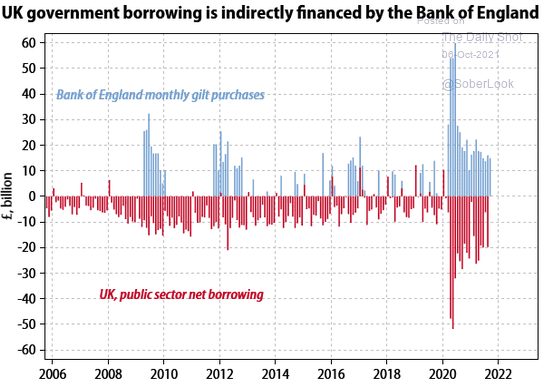

10. It is not just the Fed who has been offering massive support to buy bonds with QE. As central banks move to taper, the amount of bond supply hitting the market will skyrocket. Will interest rate increase be driven by the supply-demand equation?

Source: The Daily Shot, from 10/7/21

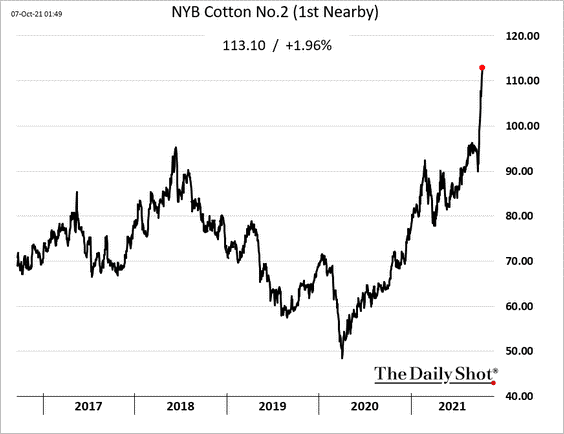

11. Extreme weather is to blame for this price spike; now clothing prices are rising quickly:

Source: The Daily Shot, from 10/7/21

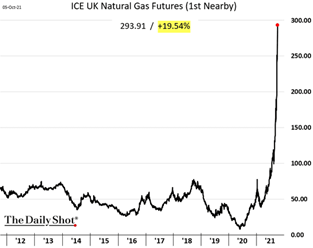

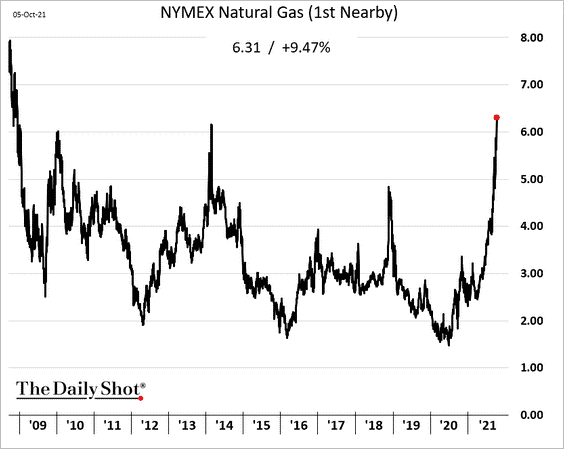

12. Covid related supply disruptions (no truck drivers), together with the conversion to clean energy (lower than expected wind and solar output), has created a massive shortage and price hikes in European natural gas. This will cause a jump in European inflation:

Source: The Daily Shot, from 10/7/21

13. The global supply chain means the U.S. feeling it too:

Source: The Daily Shot, from 10/6/21

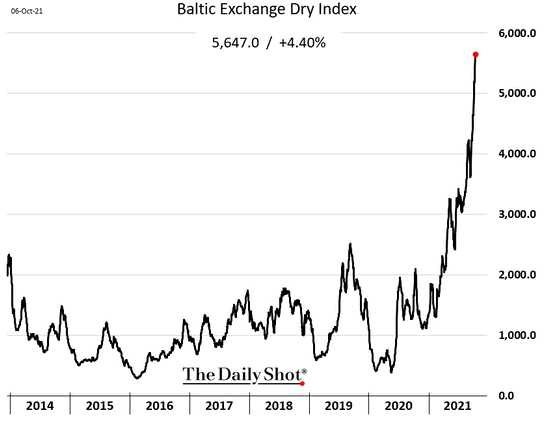

14. Shipping costs have gone ballistic:

Source: The Daily Shot, from 10/7/21

15. This is not a drill!:

Source: The Daily Shot, from 10/7/21

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)