BCM 2Q22 Market Commentary: Capturing Opportunities in an Otherwise Painful Market Environment

July 1, 2022 | TIMELY PM UPDATES

Overview

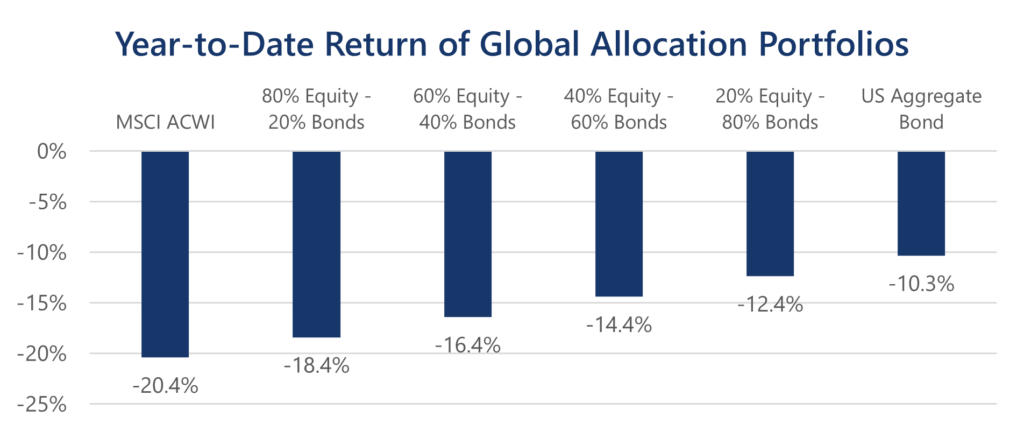

The first half of 2022 has been one of the most difficult investment environments in the past 40 years due to the simultaneous decline of bonds with stocks, and an unprecedented mix of external shocks. Although our quantitative investment system has been cautious since the fall of 2021, the relatively conservative portfolio allocations have not preserved capital this time as they have in the past. Due to rising interest rates, fixed income securities have so far failed to act as a safe haven during this period of high volatility.

Source: Bloomberg, Beaumont Capital Management (BCM). Data from 1/1/2022 through 6/30/2022.

Both our quantitative systems and our fundamental macroeconomic analysis suggest that a moderately defensive, or cautiously optimistic investment approach continues to be warranted. Although balanced allocation strategies have endured outsized suffering this year, we believe they are the best path forward. Stocks are at their most reasonable valuation in several years and bonds have become attractive again on their current yield.

The bubbles in cryptocurrency, SPAC stocks, meme stocks, and profitless growth stocks have burst in a fraction of a year. Although this exuberance and wealth destruction have adversely affected our portfolios, we are encouraged by the return of rationality to market valuations. We believe there are now special opportunities for those that can identify the downtrodden profitless growth companies that will transition to long term success.

We are not currently anticipating a quick and strong market recovery unless there is a positive external surprise, such as an end to the conflict in Ukraine. While economic indicators remain somewhat mixed, much of the real time data points suggest that consumers and businesses have already braked enough to put the economy in recession.

We have prepared educational materials on managing portfolios in extreme volatility that we would be happy to share. Please consider us as a resource and we thank you for your continued support.

A Deeper Dive

An Anomalous Market Environment – Nowhere to Hide

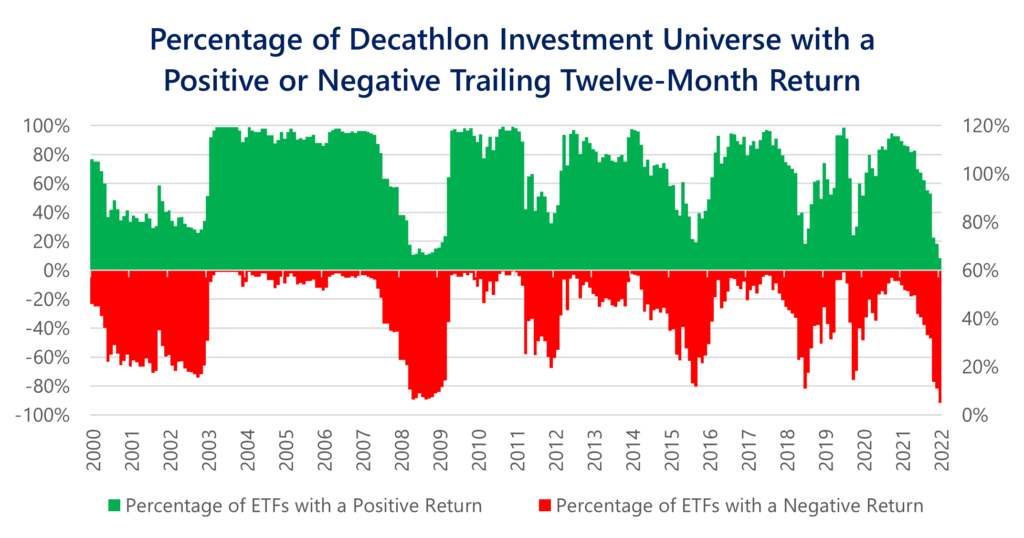

There have been few places to hide for a long-only investor. In the diversified investment universe of 132 ETFs from which we select the 10 holdings for our Decathlon strategies, as few as 9 had a positive twelve-month return in mid-June. That is the lowest number seen in the 22-year period stretching from June 2000 through June 2022. While the limited opportunities for success have been a headwind for performance it is also worth noting that outside of 2008, these periods have been short-lived. We believe there will be ample opportunities to identify attractive securities going forward even if markets remain volatile.

Source: AIM, Bloomberg. Data from 6/15/2000 through 6/23/2022.

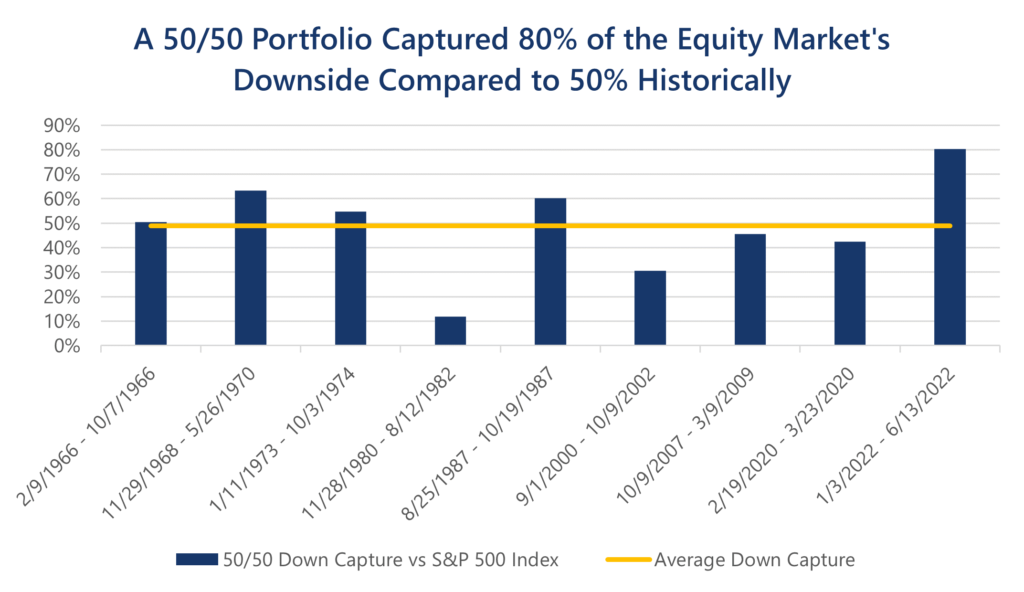

Fixed income is the asset class that investors and asset managers have historically relied on to manage volatility in their portfolios and smooth out the market’s gyrations. During this current drawdown in equity markets, fixed income has failed to act as a safe haven. From peak to trough, the 10-Year Treasury Index[1] has realized a drawdown of -21.4%, its largest drawdown since at least 1962 and nearly equal to that of the S&P 500 Index. Additionally, nearly 14% of this drawdown occurred after the S&P 500 Index’s peak in early-June. This is the largest loss coincident with an equity drawdown since at least 1962.

The combination of poor returns in fixed income coincident with a drawdown in equity markets has led to disappointing returns for many investors. This is particularly true in conservative portfolio allocations which have experienced declines consistent with a much larger drop in the equity markets historically. Historically, a 50/50 portfolio has only realized 50% of the equity market’s downside and never more than 65%. At odds with this history, through the S&P 500’s low on June 13th, a 50/50 portfolio had captured 80% of the equity market’s downside. This result is anomalous even when compared to the last period of sustained high inflation in the 1970’s.

Source: Bloomberg, Federal Reserve Bank of St. Louis, Beaumont Capital Management (BCM). Data from 1/3/1962 through 6/13/2022. The 10-Year Treasury Index is a proprietary index created by BCM, please see the disclosures for calculation methodology. Past performance is not a guarantee of future results. One cannot invest directly in an index.

The Hyperconnected Global Economy

We believe the economic feedback mechanism in our hyper-connected global economy works faster than ever. Consumers can mark the value of their homes and portfolios to market at any time allowing “wealth effects” to drive spending decisions much faster. Businesses collect and utilize more data than ever before and can quickly incorporate the actions of competitors and market signals into their operations. This responsiveness causes the economy and financial markets to anticipate and adapt, hopefully reducing the misallocation of resources which took place in prior times when business decisions were often made independently.

Bubbles are Bursting Faster

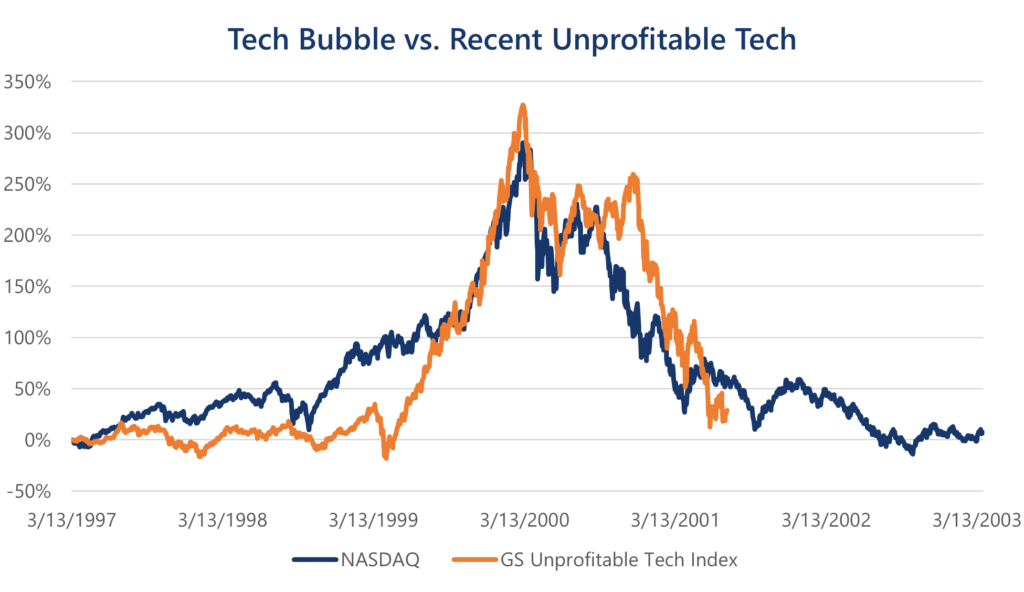

The bubbles in cryptocurrency, SPAC stocks, meme stocks, and profitless growth stocks have burst in a fraction of a year, compared to the much lengthier, and see-saw declines seen in the bursting of the dotcom bubble. This has sent a decisive signal that the years of prioritizing growth over profitability are over. Now that the market has stopped paying for promises of growth and begun demanding profitability, businesses which have relied on cheap external funding are likely to have their judgment day. Some may pivot to profitability successfully, but others are likely to find out they have an unviable business model reliant on cheap external funding.

Source: Federal Reserve Bank of St. Louis, Goldman Sachs Research. GS Unprofitable Tech Index is a proprietary index created by Goldman Sachs. Data for NASDAQ are from 3/13/1997 to 3/13/2003. Overlaid data for the GS Unprofitable Tech Index is from 2/16/2018 to 6/21/2022

A Burgeoning Recession

Source: freightwaves.com, company filings. Amazon numbers January through March, Walgreens December through February, all others 3 months ending March or April.

The markets are far ahead of the Federal Reserve’s telegraphed interest rate increases, and both businesses and consumers are hunkering down in response to the destruction of wealth that has taken place in the stock market and the reduction in purchasing power due to the recent extraordinary inflation.

It is now obvious that many of the retailers who saw a boom in growth from Covid stimulus and lockdowns incorrectly judged forward demand. After a multi-year supply bottleneck major retailers now have far more goods than they can immediately sell. Large retailers, such as Walmart and Target, who released earnings in late-May reported a $44.8 billion increase in inventories, a 26% increase from last year equivalent to roughly 1% of quarterly GNP[2].

Car sales and housing turnover are declining. Automobile sales in May were down nearly 25% year-over-year[3]. In the housing market, which is a large driver of economic activity, inventories are increasing, and buyers have pulled back on mortgage applications, though median home prices have yet to decline meaningfully.

The pandemic empowered workers, giving them both higher wages and more freedom in the way they work and spend their money. We think this has run its course, especially as the economy slows, layoffs occur, and profitability and efficiency become the prime focus. Layoffs have already begun to occur at preeminent firms such as Meta and Netflix.

We believe a recession will be relatively short lived—barring further external shocks like the Ukraine War and Covid-19. We anticipate that corporate earnings may decline, and stocks along with them before resuming steady growth. Severe recessions, such as in 2008, are nearly always driven by private sector debt. The debt accumulated in the recent cycle sits mostly on the government’s books with no due date—at least for now. Currently the average consumer has a very healthy balance sheet and corporations have less debt to profits than any time in over 30 years[4]. Without these obligations we expect both consumers and businesses to bounce back quickly.

Inflation Is Likely to Slow

It is likely that supply bottlenecks have alleviated: retailers have overshot on inventories and semiconductor companies, another major economic bottleneck, are expecting inventory to normalize. Increases in inventory along with waning demand will likely lead to markdowns, furthering the deceleration of Core CPI.

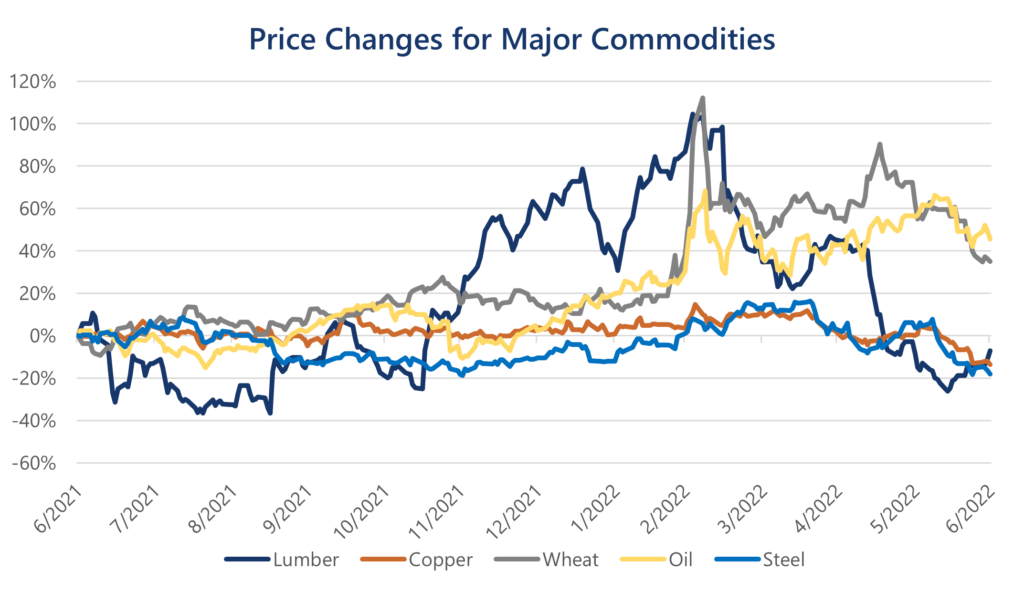

Many commodities have fallen substantially from their recent highs. Energy prices remain elevated primarily due to the Ukraine War, which has been the major source of the recent oil and food inflation. Other agricultural commodities and industrial metals are showing signs of weakness. Lumber, Copper, and Steel have now seen their price decline outright over the past year. The biggest potential positive surprise for inflation would be the sudden end of the Ukraine War. We believe inflation will otherwise be transient even though it is taking longer to subside than many expected.

Source: Bloomberg. Data shown is from 6/30/2021 through 6/30/2022.

Concluding Thoughts

Enhancements to our Investment Management Process

While our ETF investment pool currently contains exposure to energy, materials, gold, silver, and commodity producing countries, it has become clear that it does not reflect the full array of commodities available, particularly agricultural commodities. Liquidity can be a challenge in many specific commodity funds but adding additional funds to our investment universe and analyzing them on an ongoing basis will provide additional information for us to make better decisions.

When managing fixed income securities in the portfolios we have begun incorporating more advanced analytics surrounding interest rate and credit sensitivity to conduct better cost benefit analysis for trades and better target the portfolio’s fixed income composition while lowering portfolio turnover.

The Importance of Staying the Course

Over time, investors are paid for accepting risk and uncertainty. The markets will never give an obvious “all clear” signal and the best times to invest are often the times when it feels the worst. After a large drawdown in broad equity markets the odds are skewed in the favor of longer-term investors, and it’s incredibly important to stay the course with a responsible financial plan. Drawdowns are painful, but a portfolio can only recover through continued investment.

It’s clear that there’s not much to be happy about when looking backwards, but the future may be brighter. Even if the overall market stays flat or trends down further, with so many asset classes beaten up, history suggests that at least some of them may begin to trend in a positive direction. Staying invested and diversified may be the best chance to capture these opportunities.

[1] The 10-Year Treasury Index is a proprietary index created by BCM, please see the disclosures for calculation methodology.

[2] https://www.bloomberg.com/news/articles/2022-05-28/walmart-gap-and-others-amass-45-billion-in-extra-stuff-to-sell

[3] Source: Federal Reserve Bank of St. Louis. Total Vehicle Sales

[4] Source: Bloomberg. S&P 500 debt to EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)

Copyright © 2022 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The Standard & Poor’s (S&P) 500® Index is an unmanaged index that tracks the performance of 500 widely held, large-capitalization U.S. stocks. Indices are not managed and do not incur fees or expenses. BCM’s proprietary 10-Year Treasury Index is calculated using the Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity series. The Index’s daily return is the price change of a 10-year treasury bond issued at the prior day’s yield, plus any accrued interest. “S&P 500®” is a registered trademark of Standard & Poor’s, Inc., a division of S&P Global, Inc.

For Investment Professional use with clients, not for independent distribution.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)