BCM 4Q22 Market Commentary—Entering the Year Cautiously Contrarian: Considerations of Key Market Levers and Emerging Opportunities

January 20, 2023 | TIMELY PM UPDATES

What a difference a year makes. In hindsight the markets entered 2022 on an unstable precipice. Conversely, 2023 is beginning to look like a valley, with much of the prior excesses already stamped out in a painful 2022 for investors.

2022 was an incredibly challenging investment environment. Although prospective investment returns look positive, the investment environment remains fraught. Global economic conditions are weakening, Central Bankers remain inflation obsessed, a war rages on in Ukraine and the world’s second largest economy re-opened in earnest despite medical missteps. If we are indeed headed for a recession, it may be the most anticipated in history.

And yet, market participants seem steeled for worse to come. We believe the investment environment is significantly risk-averse, returns are battered across virtually every asset class, investor sentiment is depressed, and hedging is widespread. On the corporate front, CEOs are taking decisive preventative measures in anticipation of falling demand. This caution is a positive for both the economy and investors as it reduces the likelihood of businesses blindly misallocating resources and building overcapacity, resulting in a deeper and longer economic contraction.

Entering the year (again) as contrarians. While our quantitative systems entered 2022 signaling caution, in this “prepared” and risk-averse environment, our systems are relatively contrarian once again, this time seeing favorable shorter-term risk-reward across a broad range of sectors. As a result, we begin 2023 with our Decathlon strategies near the high end of their equity exposure range at each risk level (Conservative, Moderate, Growth). Our bottom-up fundamental view is also constructive. Favorite contrarian sectors include Semiconductors and Homebuilding, but our systems see opportunity across a relatively diverse set of sectors.

However, continuing uncertainties temper our short-term outlook with some caution. None of this is to say we enter 2023 absent risk—it is still unclear whether the Fed’s aggressive interest rate hikes may have some unforeseen consequences or if they are actually as adamant about increasing unemployment as they imply. If some asset class or business was to “break” from the fallout, we would expect further market turmoil and would try to respond quickly.

Over the long term, we remain optimistic that technological innovation will continue to drive growth. While the focus is currently on the short-term economic outlook, in the long run economic prosperity is driven by innovation, not simply the tempering of economic cycles. We’ve enjoyed several decades of low inflation and rising quality of life from serial innovations in technology. First the personal computer empowered us, then the internet connected us to the world’s information, and most recently the mobile smartphone enabled us to access all this knowledge and transact at any place and time. Perhaps a new form-factor on the path towards further connectivity and integration with computers will emerge. The internet of things (smart appliances of all kinds), wearable healthcare, biological “programming” or the integration of useful artificial intelligence might be the next steps in this evolution.

On the Fed, Inflation and Interest Rates:

The modern world economy is an incredibly quick problem solver, likely far more adaptive than that of the 1970s.

- An increasingly digitized and interconnected economy can adapt quickly.

- Despite anti-globalist and onshoring rhetoric, we’ve seen some impressive Global coordination:

- Within 9 months of being declared a pandemic, the world sequenced Covid-19 and developed tremendously effective mRNA vaccines.

- After Russia’s invasion of Ukraine, the European economies innovatively sourced enough natural gas to completely fill storage for Winter 2022-23 and replace Russian sources. In this same vein, consider the coordinated response to the Russian invasion and Ukraine’s clever and efficient use of weapons to withstand and push back the Russian invaders.

- We expect the modern economy to continue to solve the recent inflation problem without potentially harmful Central Bank intervention.

Most inflation, aside from wages, appears to be transitory.

- Energy prices have dropped dramatically. [1]

- Shipping rates and Covid-related supply-chain bottlenecks have been solved. [2]

- Food prices are temporarily disrupted by weather and Ukraine.

- Thanks to the Central Banks’ rate hikes, any sectors that require credit financing such as housing and automobiles[3] have seen sharp declines in demand.

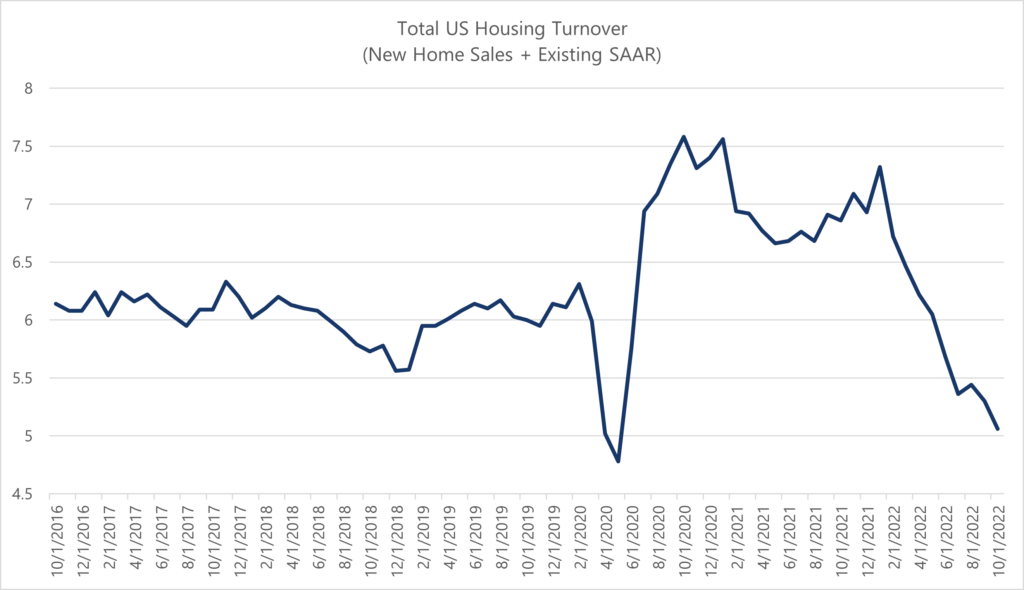

Source: Bloomberg, Data from 10/31/16 to 10/31/22

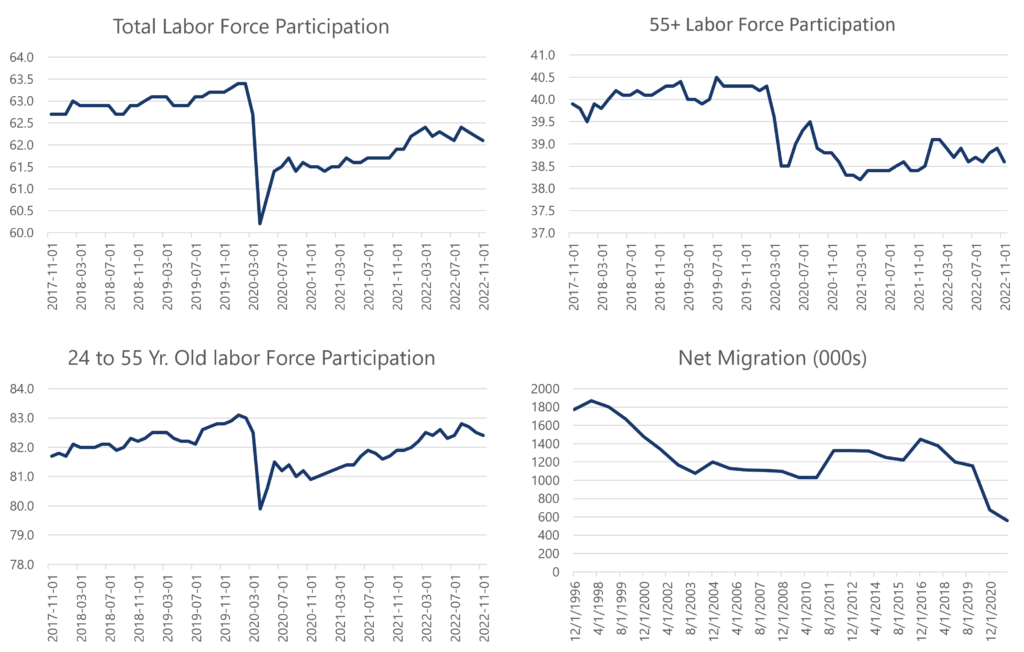

The labor market has structurally changed and the solution isn’t higher interest rates.

- The Covid-19 lockdowns and the work-from-home technological revolution revealed the tradeoffs of office work and the new life-enhancing possibilities of more flexible work-from-home arrangements.

- Financially secure Baby-Boomers have chosen to age out of the workforce while net immigration into the U.S. continues at depressed levels—due to Covid-19 restrictions—limiting the supply of workers in many service industries.

- The result is a large shortfall in the overall supply of labor, not excessive demand for labor which interest rates might curb.[4]

Source: For Labor Force Participation, FRED data from 11/1/2017 to 11/1/2022 by quarter. For Net Migration, Bloomberg with annual numbers from 1996 to 2021.

We expect Central Bankers will soon recognize they have played the part of an impatient doctor – continuing to over-dose their seemingly unresponsive “patient” with interest rate hikes.

- The FED’s successive interest rate hikes haven’t had the intended effect of slowing wage inflation.

- They have caused immediate and worrisome adverse effects on other important sectors, particularly housing-related and real estate.

- Housing turnover has skidded to a near halt, causing a dramatic recession in real estate, mortgage origination, home furnishings and construction trades. Heretofore, this same Federal Reserve would be racing to rescue the crucial sector.

- In another strange twist, existing homeowners have been spared from the pain of higher interest rates, as just about everyone refinanced their mortgage far below prevailing rates.

On the Economy:

We believe the prospective recession of 2023 may look very different than those of the past.

- It would likely be self-inflicted, rather than forced through a major misallocation of resources and accumulation of bad debt.

- Neither Consumers nor Businesses are encumbered with debt. Only the Federal government has accumulated large amounts of debt from the Covid response.[5] Setting aside the potential future tax obligation, interest expense is historically low as a percentage of disposable income, and household wealth remains high which should add resilience.

Source: FRED database 1/1/1980 through 7/1/2022 by quarter

Nearly every industry that experienced a surge in growth during Covid-19 has reverted towards trend. Most have already taken steps to correct these errors.

- Many businesses falsely read the changes in demand as permanent and, subsequently, over-invested in human resources and inventory. It wasn’t just startups like Peloton, DoorDash and Shopify, but some of the best growth companies in the world including Amazon, Google, and Target.

- We expect many of these companies to resume their successful growth after they digest the excesses and recalibrate their trajectory. Amazon, Apple, Google, Meta and Microsoft all are meaningfully reducing staff or limiting growth to selective areas, as are young gig-economy companies, like Lyft, DoorDash and Shopify.

- In some cases, these mis-calibrations are likely to present healthy businesses with attractive M&A opportunities as otherwise valuable businesses struggle to find capital to internally fund their operations.

On Innovation:

The recent Electric Vehicle bubble is reminiscent of the dot.com bubble.

- The recent fall from grace of Tesla’s high-flying stock price[6] and the whole electric vehicle sector is reminiscent of the ending of the dot.com stock bubble.

- In hindsight, after the dot.com share prices collapsed, there was somewhat of a “golden age” for the leading internet companies with truly revolutionary products, like Amazon.com, E-Bay, and Google.

- By analogy, with all sorts of innovative electrical vehicles on the horizon from both start-up and incumbent auto manufacturers, we might be beginning a great period for “electrification” investments, and perhaps electric vehicles will evolve into “smart cars” with unanticipated capabilities in the same way the cellphone became the smartphone.

In healthcare, the “War on Covid-19” catalyzed many innovations.

- Certainly, MRNA technology has many exciting applications.

- Also on the healthcare front, breakthrough medicines from Novo Nordisk and Eli Lilly originally developed to treat diabetes appear to have extraordinary potential as weight-loss medications. Obesity is a common underlying factor of many life-shortening healthcare problems and affects quality of life. The new medicines might quickly become the biggest sellers and most impactful of all-time.

AI and Deep Learning technologies are reaching a consumer-facing stage.

- Microsoft recently announced a $10B investment into Open AI after their Chatbot ChatGPT reached over one million users in online beta testing[7].

- It is likely AI will augment humans and potentially increase productivity in unforeseeable ways in the near future.

Looking ahead:

Asset markets are forward-looking discount mechanisms. In a potential reverse of 2022—when the economy held up while asset prices fell in anticipation of weaker economic conditions—economic conditions are likely to further deteriorate into 2023, and yet attractive investment opportunities may emerge.

While both our fundamental view and quantitative models are currently constructive on risk, we acknowledge that it may be seductive to chase risk after a poor year for all assets while the environment remains very uncertain. Lower risk assets like fixed income may also be attractive given their higher yields. Acting nimbly is likely to be more beneficial than simply increasing risk.

[1] Crude oil fell from a high of $123 in March to a price of $77 on 12/31/2022. Source: Bloomberg

[2] The Baltic dry index, a measure of the cost of ocean freight has declined 55% from its highs in May. Source: Bloomberg

[3] The Manheim US Used Vehicle Value Index has fallen 14.9% year-over-year through December 2022. Source: Bloomberg

[4] The Federal Reserve has hiked rates at the most aggressive pace in history starting in April, yet the U.S. economy didn’t have as many people employed as Pre-Covid until August.

[5] Government debt increased $5 Trillion or roughly $16,000 per capita

[6] Tesla’s stock price reached a high of $409.97 on 11/4/21 and closed 2022 at $123.18 a decline of 70%. Source: Bloomberg

[7] Microsoft in talks to invest $10 bln in ChatGPT-owner OpenAI, Semafor reports | Reuters

Copyright © 2023 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The Standard & Poor’s (S&P) 500® Index is an unmanaged index that tracks the performance of 500 widely held, large-capitalization U.S. stocks. Indices are not managed and do not incur fees or expenses. The MSCI ACWI Index is designed to represent performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 24 emerging markets. The ICE BofA US Broad Market Index tracks the performance of US dollar denominated investment grade debt publicly issued in the US domestic market, including US Treasury, quasi-government, corporate, securitized and collateralized securities.

“S&P 500®” is a registered trademark of Standard & Poor’s, Inc., a division of S&P Global, Inc.

For Investment Professional use with clients, not for independent distribution.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)