Changes to the Aggregate Bond Index that Advisors Should Know About: Part Two

March 5, 2020 | TIMELY PM UPDATES

Last week, we shared some facts about the Bloomberg Barclays Aggregate Bond Index (BBAB). (Missed it? Click here). Outside of the BBAB, there are a few more items that you may want to know about in the corporate bond landscape that may also surprise you and your clients.

Today, the largest cohort of bonds in the Bloomberg Barclays Investment Grade Index is the lowest level of investment grade (IG) credit, BBB. Back in 2009, the level of BBB bonds in the index was about 32%. Now, BBB credits represent over 50% of the Index. With interest rates so low in recent years, U.S. corporations have taken advantage and issued massive amounts of debt. We’ll get to the amount of debt in a moment, but the point here is that the credit status of half of the investment grade corporate bond universe is in the lowest rating before dropping to junk bond status.

Since the demarcation of Investment Grade versus junk has such a draconian effect on what a corporation pays in interest, there seems to be a reluctance by the rating agencies to downgrade BBB bonds when in fact a junk rating is warranted. Why would this be?

- The rating agencies don’t want to see their customers pay more in interest

- The rating agencies don’t want to be fired

- The rating agencies can’t find enough higher rated debt

- It is a massive undertaking when debt changes to junk status

- All of the above

The answer is E! …but C needs to be fleshed out.

Moral Conflict of Rating Agencies

In my humble opinion, the rating agencies have a moral conflict. To put this moral conflict in perspective, bond issuers, including companies, municipalities, and State and Federal issuers, must pay fees to one or more rating agencies to get rated. These fees are typically assessed annually. Therefore, if a rating agency downgrades an issuer, they stand a much higher chance of being fired or losing that rating fee. So, what tends to happen? Nothing.

Falling from investment grade to junk bond status has dire consequences for the issuer. The cost of borrowing for that company increases dramatically, and their bonds must then be sold by investment grade funds, ETFs, or managers and hopefully bought by junk bond managers. Yet the size of the junk bond market is tiny compared to the investment grade universe, so the prices of these newly rated junk bonds tend to suffer.

You can begin to see why the rating agencies are reluctant to make these downgrades due to the cause and effect on the companies and their profits alike. This leads us to ask: how many companies should be downgraded to junk? On February 28th, Jeff Gundlach of Double Line Investments estimated that 55% of all BBB rated bonds would be rated as junk today if they were “properly” rated.

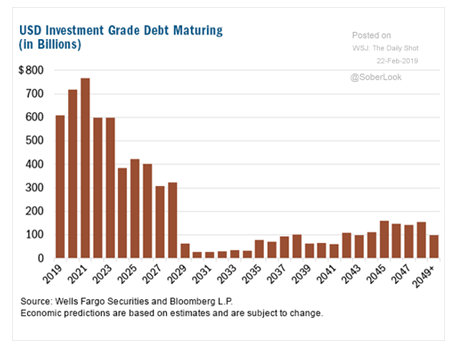

Investment Grade Debt Maturing

Bonds in general, regardless of rating, have maturity dates. Many investment grade and corporate bonds are issued with relatively short maturities. However, in the aggregate, ~55% of the ~$6 trillion of investment grade debt matures in the next 5 years and ~75% matures in the next ten.

This is important because if interest rates rise even modestly, the renewal rates and increased interest expenses could prove to be a real challenge. Competing with these bonds is the massive $22 trillion of U.S. Treasury debt, an annual federal deficit of $1-1.5 trillion needing treasuries to finance, and even $600 billion of QE reversal. All this supply must be bought by somebody, and the only real question is: at what interest rate?

Click here for Part 1 of this piece on bonds if you missed it!

Sources and Disclosures: