China Attempts to Calm Markets, Small- and Mid-cap Equities’ Relative Attractiveness, Update on the Fed’s Latest Rate Projections

March 18, 2022 | FIRESIDE CHARTS

The Chinese government is attempting to calm markets after steep price declines. Employees may be returning to the office, but companies aren’t leasing new office space just yet. Performance of small- and mid-cap equities has been much worse than large-caps, but they may be more attractive now on a fundamental basis. Demand for houses remains strong. The composition of inflation is shifting. Semiconductor supply is still strained. This week’s Federal Reserve Board meeting was widely anticipated, their updated projections for short- and long-term policy rates are contained within.

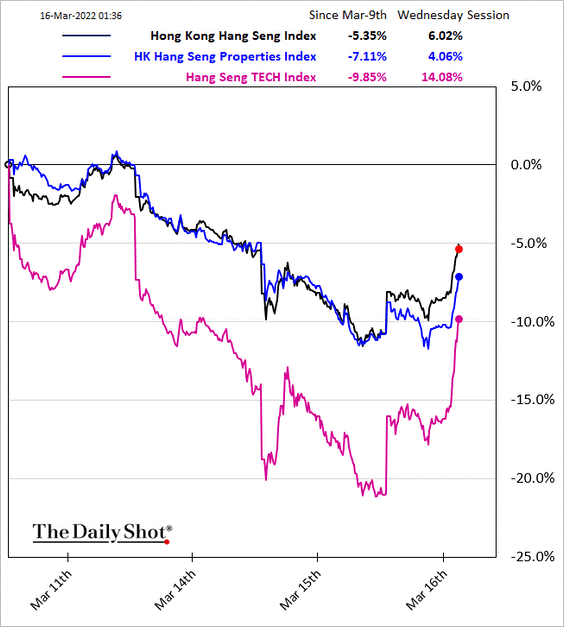

1. Only time will tell but this statement was an extremely positive development for investors in Chinese equities:

Source: @SofiaHCBBG

Source: The Daily Shot from 3/16/22

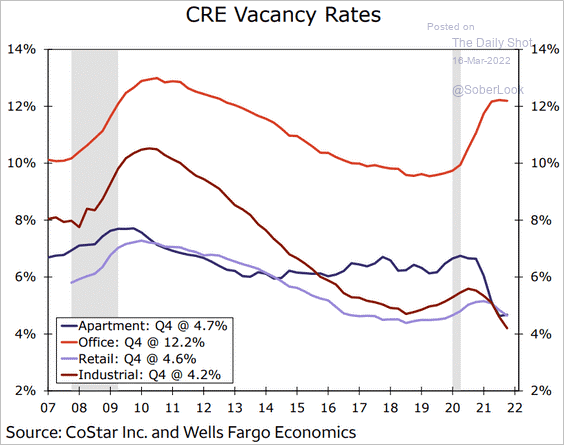

2. Vacancy rates remain elevated in office buildings:

Source: Wells Fargo Securities

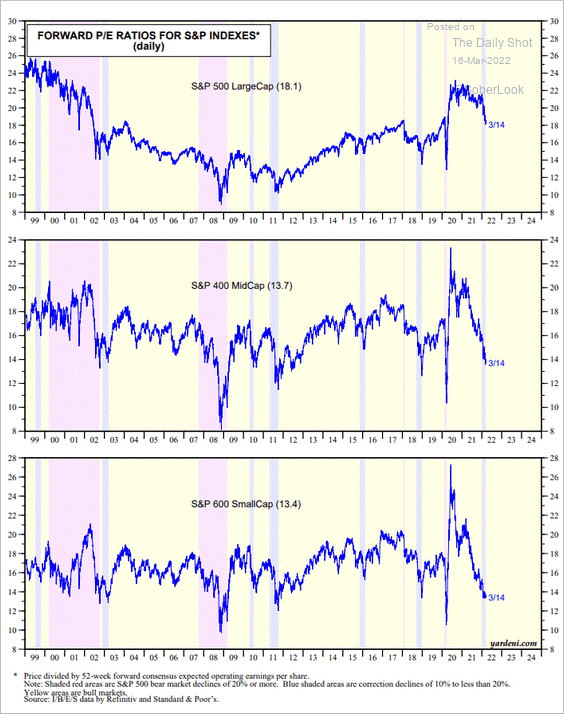

3. If forward estimates are correct, mid-cap and small-cap equites are beginning to look attractive:

Source: Yardeni Research

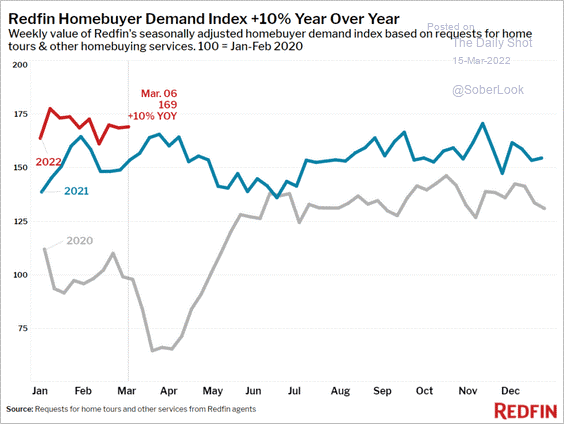

4. Increased mortgage rates have hurt housing affordability, but potential demand remains strong:

Source: Redfin, @tayloramarr

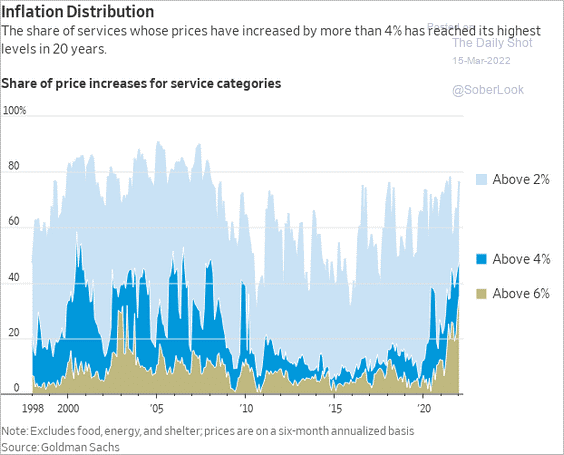

5. Rises in services inflation, largely driven by wage increases, may be more enduring than goods inflation:

Source: @NickTimiraos Read full article

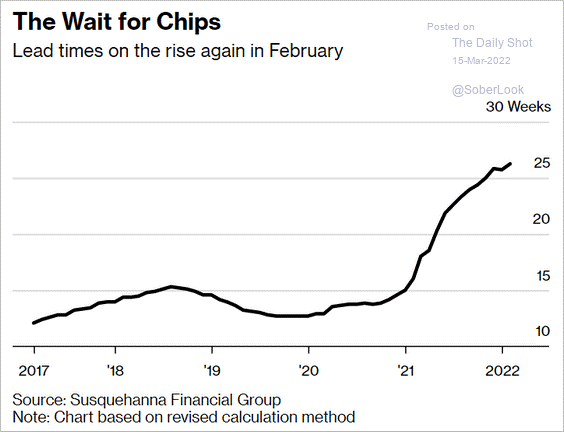

6. Semiconductors are crucial to the modern economy, lack of availability will continue to stress supply chains:

Source: Bloomberg, Read full article

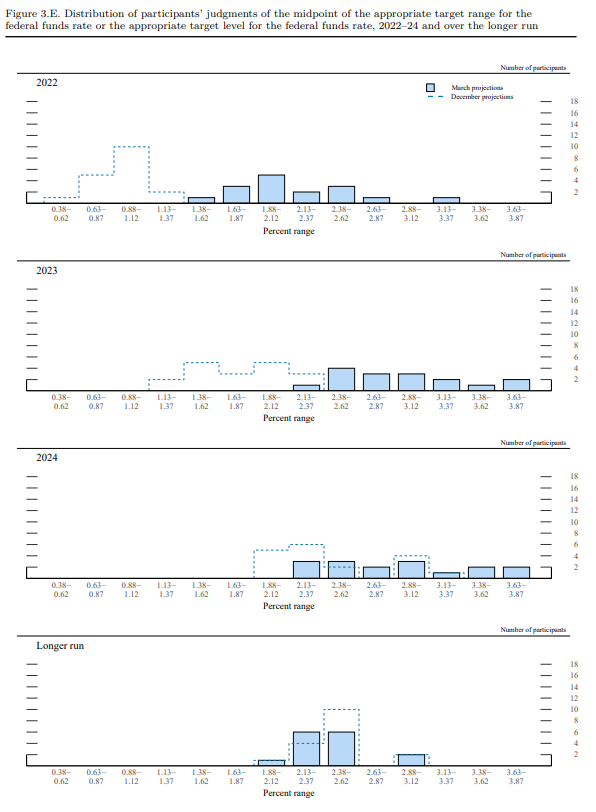

7. The Federal Reserve Board’s projection for policy rates over in 2022 and 2023 increased materially, but projections for appropriate long-term rates were little changed:

Source: Federal Reserve Summary of Economic Projections, 3/16/22

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.