Earnings, Consumer Spending, China

May 2, 2024 | FIRESIDE CHARTS

Earnings season is well underway, and thus far, the data has exceeded expectations. This may be partially explained by an unexpected surge in consumer spending in March, following a weak start to the year. Although there are signs of weakness in the labor market, it has yet to impact wage growth and consumer spending in any meaningful way. Strong wage growth and spending are likely to complicate the downward trajectory of inflation. China is staging a quiet comeback. The rising Dollar hasn’t knocked the shine off commodities. Big vs small.

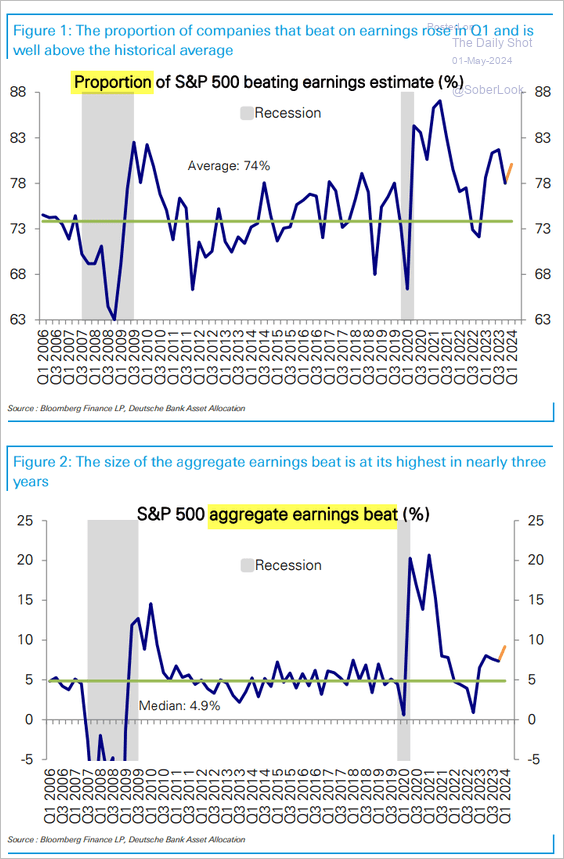

1. It’s normal for most companies to beat earnings, but expectations were lower than usual in the first quarter:

Source: Deutsche Bank Research

2. Earnings beats have been higher than normal nearly across the board:

Source: Deutsche Bank Research

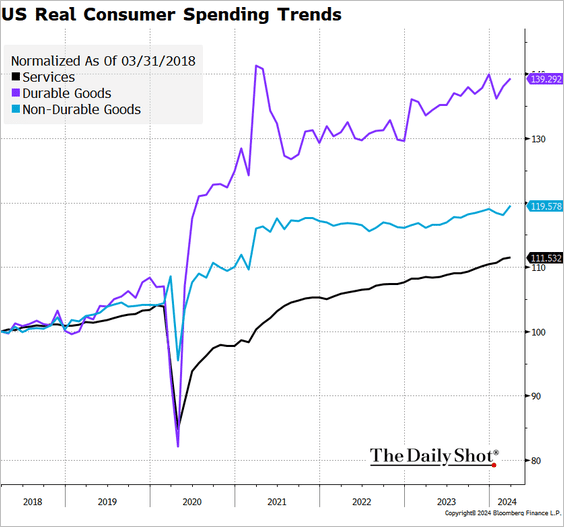

3. Service spending tends to dominate the headlines, but goods spending has remained remarkably strong:

4. More workers are staying put at their current jobs, which has historically led to slower wage growth:

Source: @economics Read full article

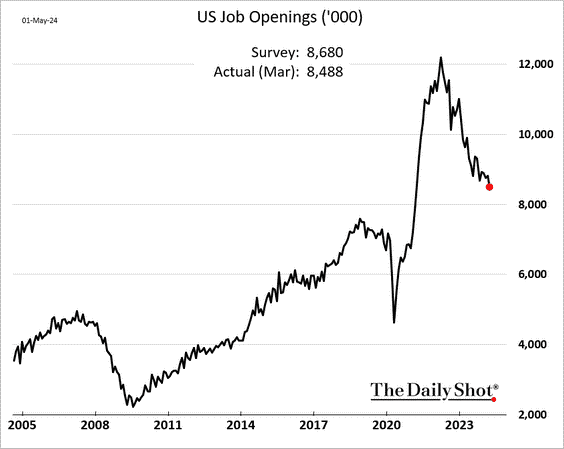

5. Job openings have also continued to fall:

Source: The Daily Shot 5/2/2024

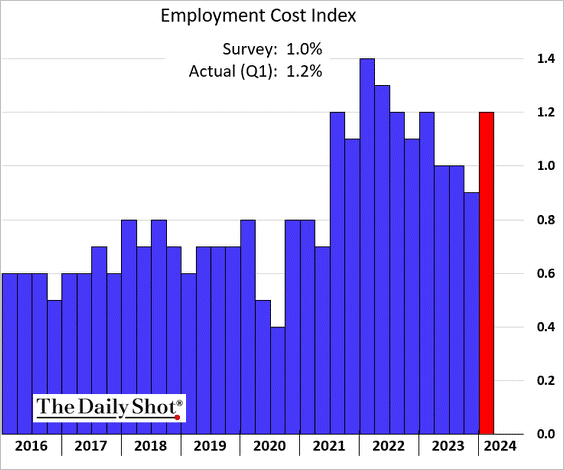

6. Employers have yet to see much relief in employment costs:

Source: The Daily Shot 5/1/2024

7. Both headline and core PCE inflation are running above 3% in recent months:

Source: The Daily Shot 4/29/2024

8. Chinese equities have quietly hit their highest level in months after being left for dead by most investors:

9. The highest rates in the developed world have boosted the Dollar:

Source: @opinion Read full article

10. Increased infrastructure spending continues to push the price of copper higher:

Source: The Daily Shot 4/30/2024

11. Profitability for large cap companies is near multi-decade highs while small cap profitability has fallen to recessionary levels:

Source: @IanRHarnett

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.