Equities Slide Ahead of Election Day, Historic Surprise Earnings Beats, and Positive Signals from the Bond Market

November 2, 2020 | FIRESIDE CHARTS

U.S. equities appear to be growing nervous ahead of the election—the S&P 500® Index suffered its worst week since March and fell nearly 6% last week—but could the dip leave them with more room to grow? Surprise earnings beats are at historic highs, though they are aren’t being rewarded in the typical fashion—investors seem aware of just how difficult a job analysts were tasked with in 2020’s unprecedented landscape. Over in the bond market, could higher yields finally be on the horizon?

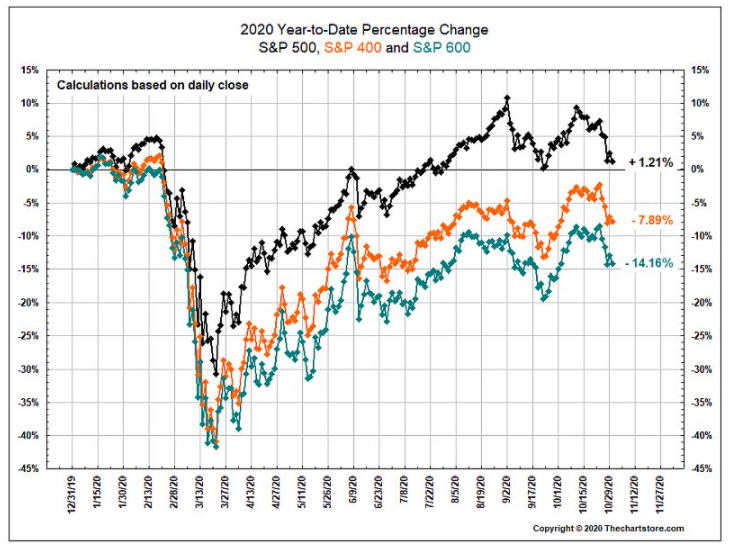

1. Just about every U.S. stock index pulled back 4-7% last week…

Source: The Chart Store, from 11/2/20

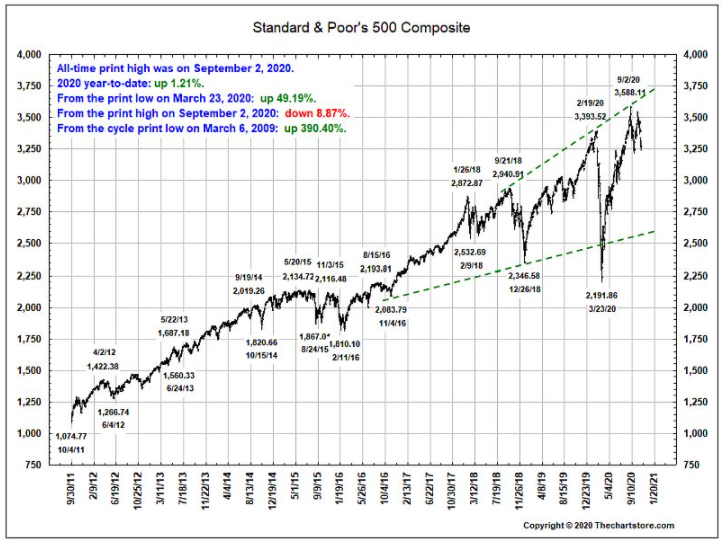

2. Will the “election correction” infuse enough pause and doubt to allow for a sustained post-election rally?

Source: The Chart Store, from 11/2/20

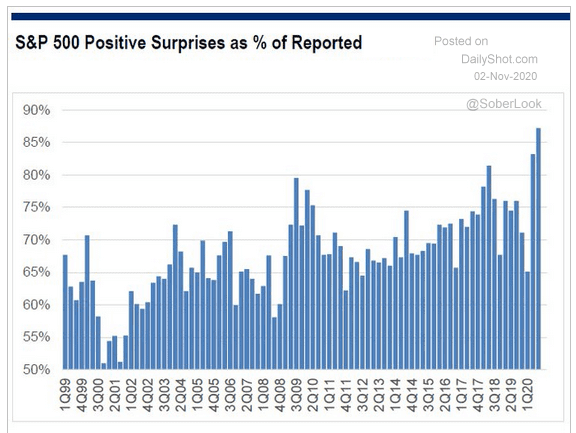

3. Did managerial/analyst caution drive earnings estimates too low?

Source: The Daily Shot, from 11/2/20

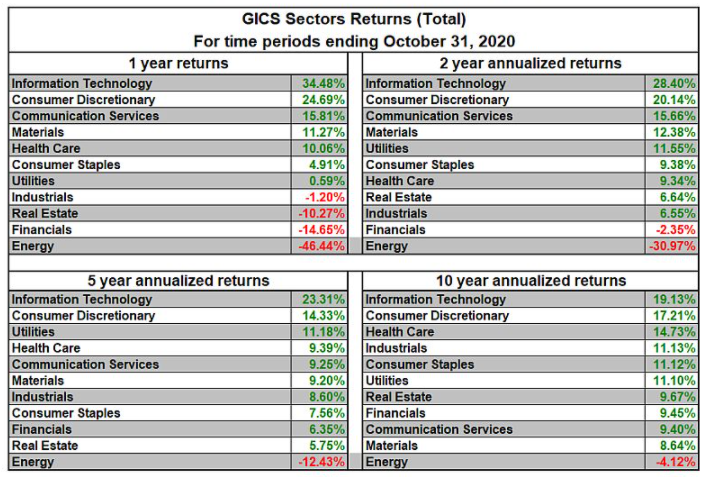

4. Since we emerged from the Great Recession, market leadership has been clear and consistent:

Source: The Daily Shot, from 11/2/20

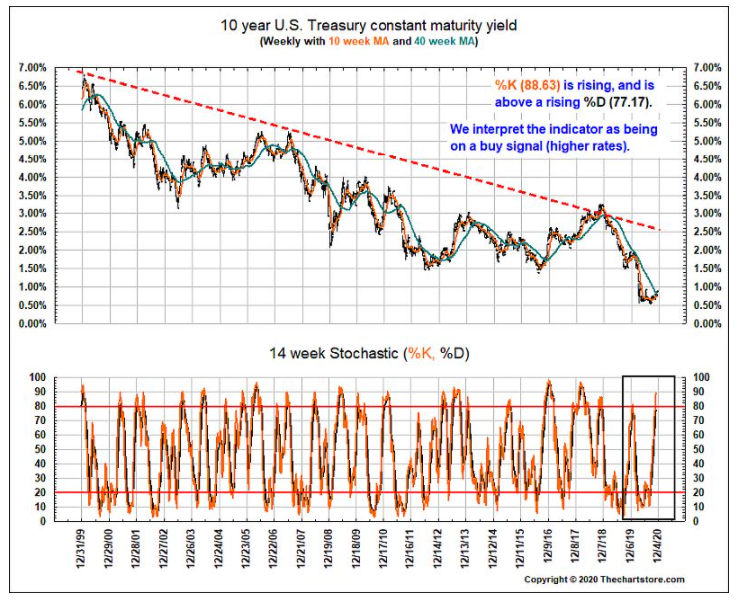

5. Has U.S. interest rate limbo finally ended?

Source: The Chart Store, from 11/2/20

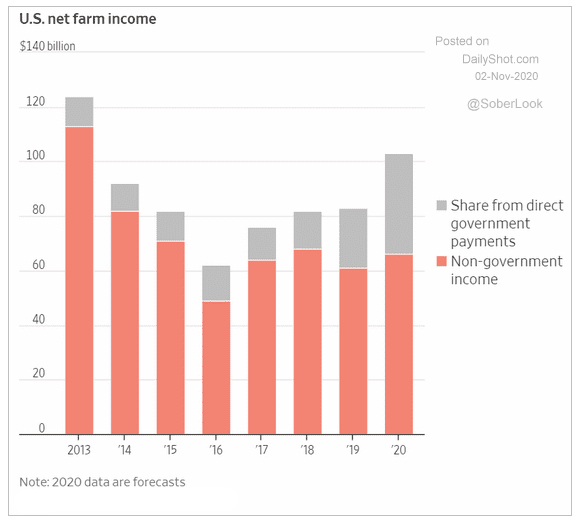

6. A hidden cost of the trade wars? We have to pay to keep our farmers afloat?

Source: The Daily Shot, from 11/2/20

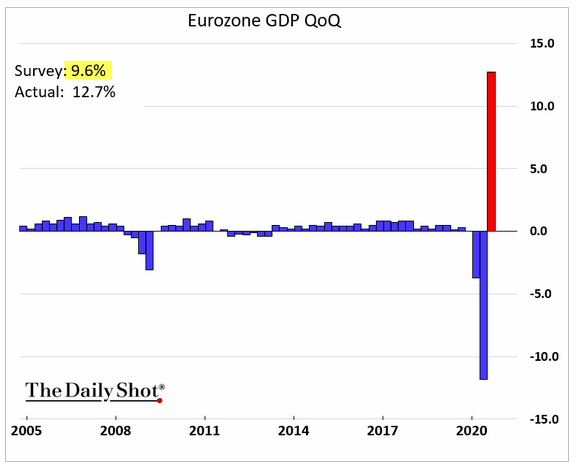

7. Like the U.S. last week, Europe’s GDP had a nice rebound but has a long way to full recovery…and Covid has them back in shutdown mode…

Source: The Daily Shot, from 11/2/20

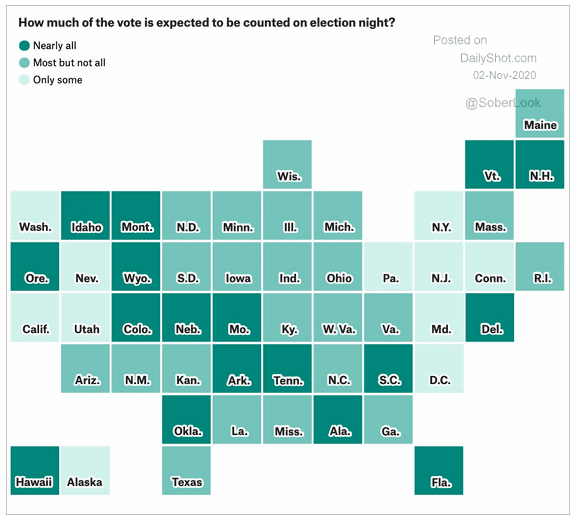

8. Forget the hanging chads…we have a wonderful problem: a lot more Americans have/plan to vote so don’t expect a quick answer tomorrow…

Source: The Daily Shot, from 11/2/20

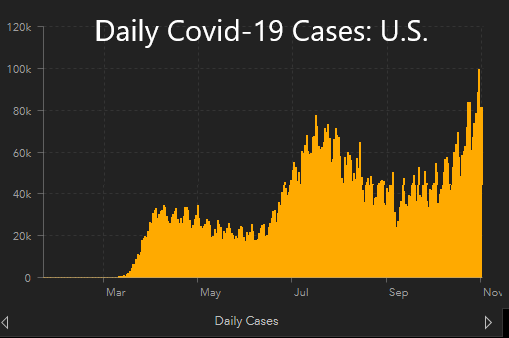

9. The only thing we are sick of more than the elections is Covid. Yet by week’s end we will have over 50 million cases world-wide and 10 million here in the USA…

Source: The JHU CSSE, as of 11/2/20

10. Why is Europe locking down again? Note the scales!

Here are the new daily cases in the U.K:

And here’s Germany and Italy:

Source: The JHU CSSE, as of 11/2/20

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.