Household Net Worth Hits an All-Time High, A More Hawkish Fed, and a Look Ahead at GDP

September 24, 2021 | FIRESIDE CHARTS

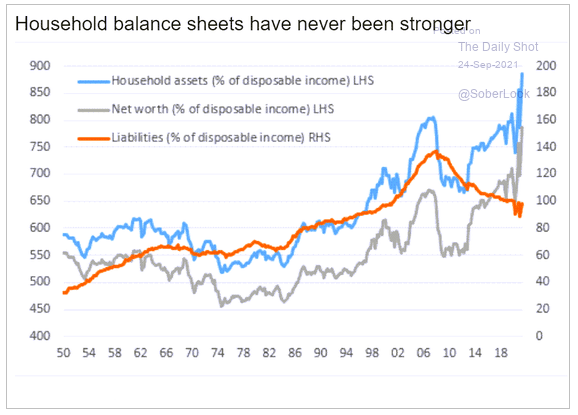

U.S. household net worth hit an all-time high of $141.7 trillion in Q2 after a 19.6% year-over-year gain, per the Fed’s report Wednesday. Household assets are also at a record high, which may come in handy if consumers’ personal finance expectations prove prophetic. Services and manufacturing PMI have both moderated, removing some fuel from the inflationary fire, but Fed governors don’t appear calmed with a growing number of Committee members viewing inflation risk as on-the-rise. And what happens when we factor in J.P. Morgan’s expectations for global GDP growth? We didn’t see any major policy shifts out of the Fed this week, but it did lay the groundwork for a QE unwind to begin in November and hint that interest rates could begin to climb in 2022. But with so many factors brewing beneath the surface, could the climb spin out of their control? Finally, a global check-in shows moderation in services and manufacturing isn’t limited to the U.S. and just how much perspective can distort reality. We’re looking at you Greenland…

- Great news for the aggregate American household! Are we near a peak?

Source: The Daily Shot, from 9/24/21

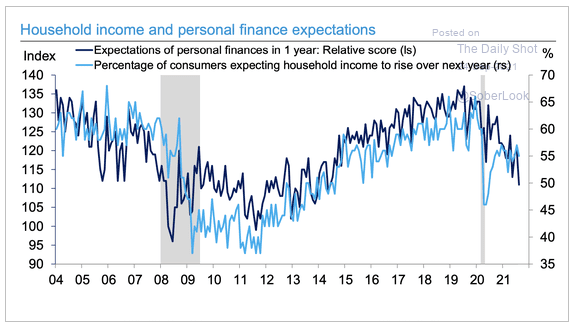

2. Americans expect their financial situation to be worse going forward, which may keep much of the excess savings from the pandemic in savings.

Source: Deutsch Bank Research, from 9/24/21

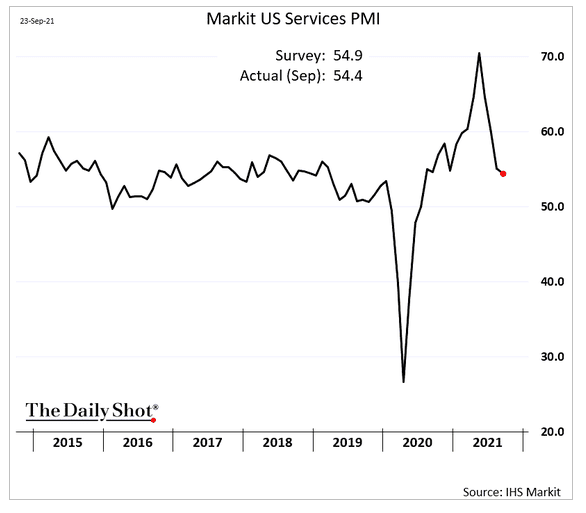

3. Our services sector has “normalized” back to into the slow growth range. The Manufacturing PMI also moderated.

Source: The Daily Shot, from 9/24/21

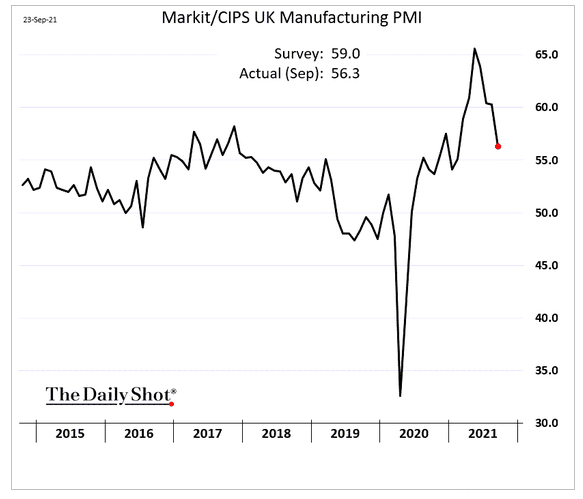

4. All in the face of moderating Manufacturing activity:

Source: The Daily Shot, from 9/24/21

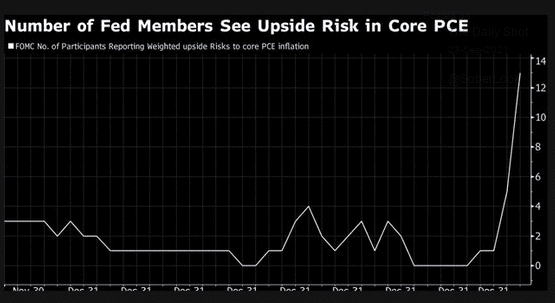

5. As we showed in Monday’s blog, rents are surging. Housing, or equivalent rents, makes up over 42% of the CPI index. It is not a surprise that now the Fed governors are weary:

Source: Markets Reporter-New York, from 9/23/21

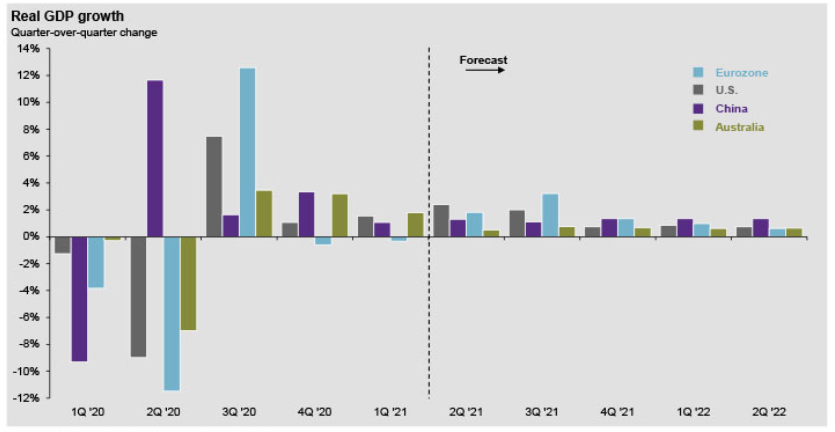

6. If JPM’s predictions for a return to sub-2% global GDP growth is coupled with higher inflation, the ’70” taught us that stagflation is not a whole lot of fun:

Source: J.P. Morgan, from 9/23/21

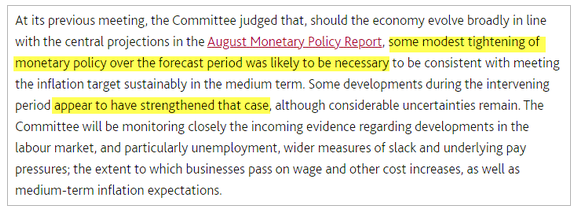

7. Here we go–the BOE also signaled QE tapering and/or rate hikes are coming:

Source: The Daily Shot, from 9/24/21

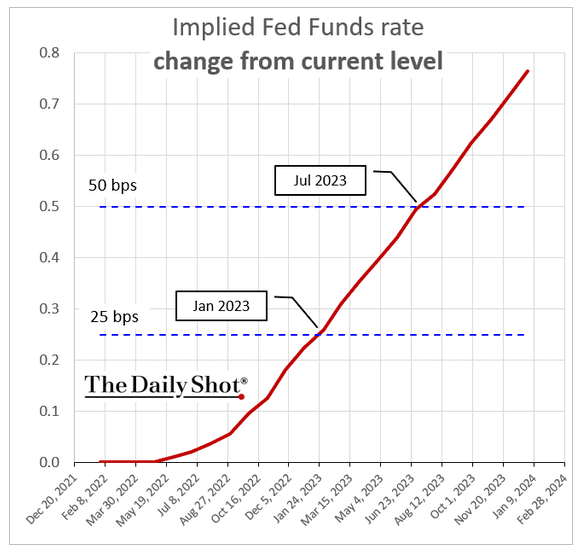

8. Zoom out to a historical perspective. 50 bps is still incredibly accommodative. Is the QE taper, together with the $5.4 trillion of proposed legislation and the $1 trillion deficit, going to cause rates to climb beyond the Fed’s control?

Source: The Daily Shot, from 9/23/21

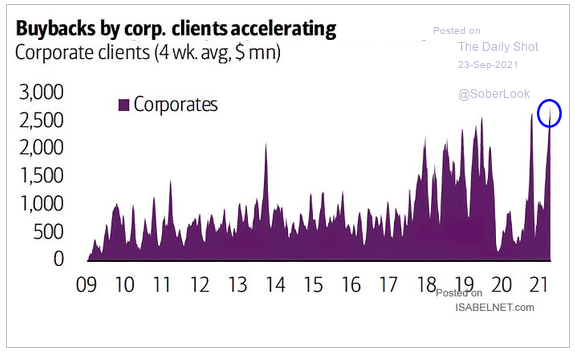

9. Still the best use of eared cash? Is R&D suffering?

Source: The Daily Shot, from 9/23/21

10. Europe is following the U.S.:

Source: The Daily Shot, from 9/24/21

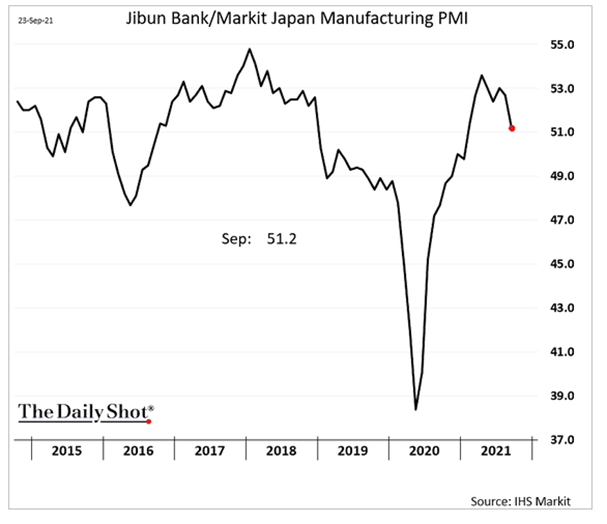

11. Japanese manufacturing is at lower levels than pre-pandemic.

Source: IHS Markit, from 9/24/21

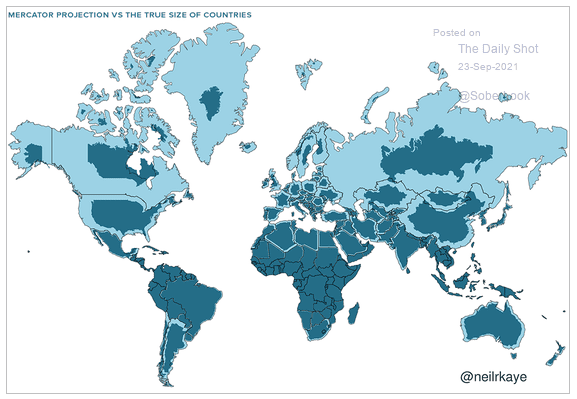

12. Scale and perspective matter! The same can be said for the use of statistics and economic data in investing…

Source: The Daily Shot, from 9/24/21

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.