A Busy Fed, a 20+ Year Record for the S&P 500, and Bracing for Further Supply Chain Pressures

November 9, 2021 | FIRESIDE CHARTS

November will be a big month for Federal Reserve developments, with more actionable talk of rate hikes and plans to start tapering asset purchases before the end of the month. With a balance sheet above $8.5 trillion though, it’s going to be a long haul—even with the planned decreases of $15 billion per month. A strong jobs report—the U.S. soared past expectations to add more than 530,000 jobs in October and bring the unemployment rate down to 4.6%—and the passage of the Biden infrastructure package seemed enough to cool investor tempers though. There’s been no sign of a repeat of 2013’s taper tantrum as the S&P 500® notches its longest stretch of closing highs since 1997 and the three major indices approach six straight weeks of gains. But how frothy are the markets and just how vulnerable is the massive—and still growing—population of novice investors? We may not be seeing a repeat of 2013, but are we living one of 1999? Meanwhile, international travel restrictions eased in the U.S. this week, but the Delta variant remains a major concern as Germany’s infection rate spikes to its highest since the onset of the pandemic. Are supply chains set to face even further headwinds?

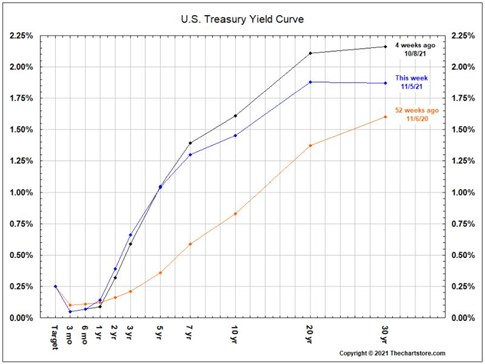

1. The intermediate and long end of the curve saw rates retreat as central banks talk up a slower cycle for rate hikes. Instead of another taper tantrum, the markets seem to have cheered:

Source: The Chart Store, from 11/7/21

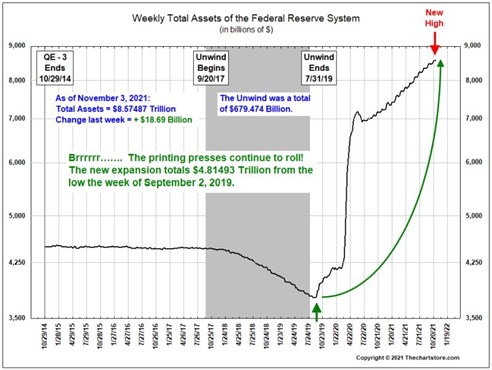

2. So far, the Fed has purchased $4.8 trillion in bonds to support the Covid-ravaged economy. The taper of new purchases now starts, but barring the unforeseen, it will be over $5 trillion before it is done. As these bonds mature, and the trillion-dollar annual budget deficit is added to the new trillion-dollar transportation bill, we ask: “Who is going to buy the additional $~7 trillion?!” Percentage-wise, our federal debt has gone from ~$22 trillion to ~$29 trillion in two years, about a 1/3 increase add anything new passed in Washington…

For a great look at all our debt, please go to: https://www.usdebtclock.org/

Source: The Chart Store, from 11/7/21

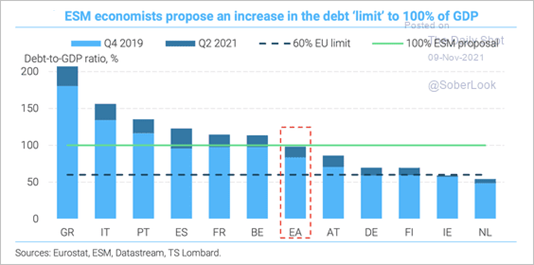

3. If you cannot hold the line, move the line. Is the EU now “incorporating” government debt into their fiscal rules?

Source: TS Lombard, from 11/9/21

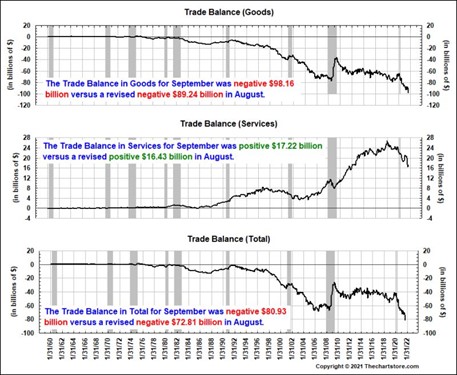

4. Speaking of deficits, our trade deficit hit a new record:

Source: The Chart Store, from 11/7/21

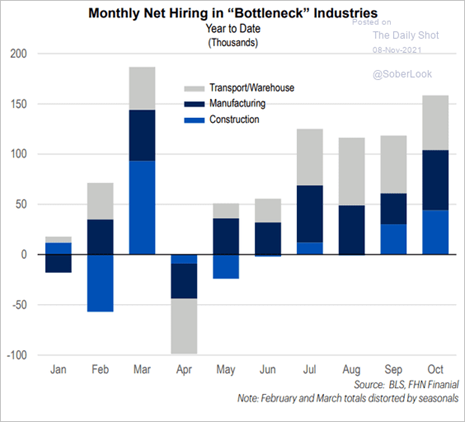

5. The strong jobs report showed alleviation in the bottleneck industries:

Source: FHN Financial, from 11/8/21

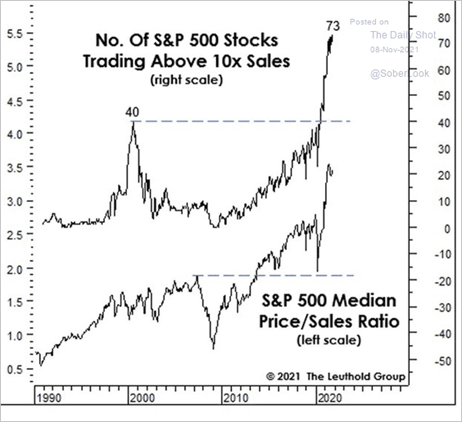

6. There are many signs that the stock markets are frothy:

Source: The Daily Shot, from 11/8/21

7. Just how healthy is the market? Despite new index highs, only 16% of the S&P 500 stocks are at new highs. With just the big boys moving higher, it reminds us of 1999…

Source: Bloomberg, from 11/8/21

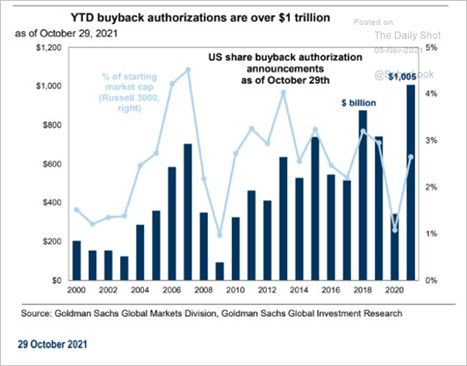

8. Buybacks are a main driver:

Source: Goldman Sachs, from 11/8/21

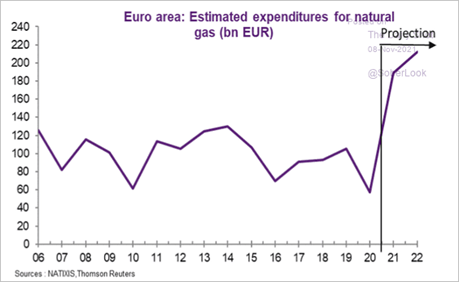

9. A confluence of events has almost quadrupled European natural gas costs:

Source: Natixis, from 11/8/21

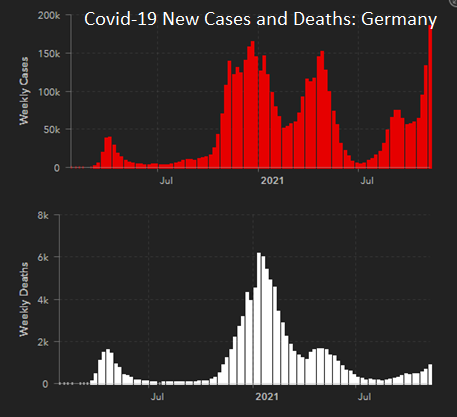

10. Delta Covid is ravaging eastern Europe and it is spreading west. This is one reason the central banks are taking a more cautious tone. Coupled with the Chinese outbreaks in 15 provinces, will supply chains get screwed up again? Here’s Germany:

Source: JHU CSSE, as of 11/8/21

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.