Inflation Admittedly Not Transitory, Energy Volatility and Effects of Rising Yields

January 13, 2022 | FIRESIDE CHARTS

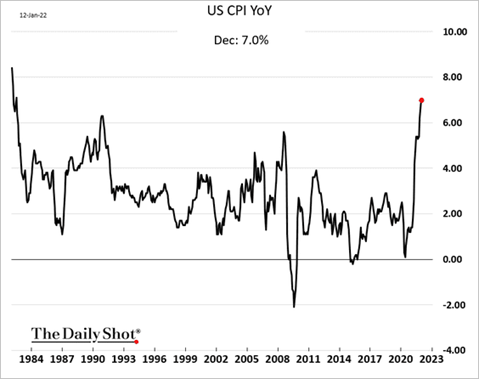

Is the Fed behind the curve? It wouldn’t be the first time! Recently they started admitting that many of the inflationary inputs are not transitory. We show you some reasons why. If inflation is here for at least a while, can history show us what might happen to the various markets, sectors and profits?

1. Yesterday, the World Health Organization predicted that half, yes half, of all Europeans will have or will just have had Covid. The ports of Los Angeles and Long Beach are so short of healthy workers that the backlog of ships to unload is growing again. China just closed its third city so far due to a Covid outbreak. It is reasonable to assume bottlenecks are going to get worse before they get substantively better. This is likely to help prevent overall inflation from being transitory.

Source: The Daily Shot from 1/12/22

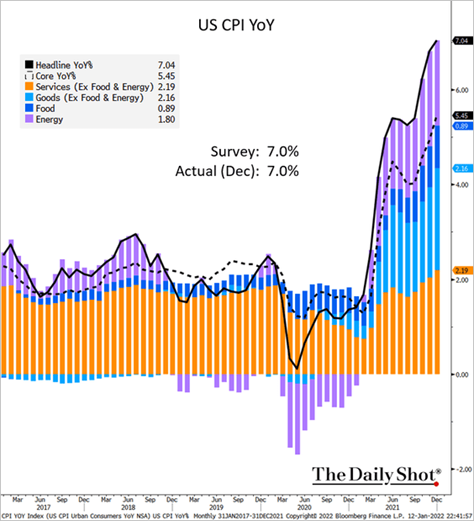

2. Many inputs to inflation are long-term/permanent. A rent increase is for one or more years. Salary increases are annual. These are not transitory! Focusing on core inflation is a fool’s errand…Do you need to heat your home/office, travel or eat? Volatility does not erase reality.

3. Energy prices are volatile, but over the last 12 months oil is up almost 50%. This will infiltrate into almost every facet of our economy and our lives. It also takes time. For example, fuel and fertilizer price increases today will not be felt by consumers until the farmers produce is brought to market months from now.

Source: The Daily Shot from 1/12/22

4. Steel and lumber prices are surging again. Here is lumber:

Source: The Daily Shot from 1/12/22

5. Will a USD retreat further strengthen the costs of commodities?

The Daily Shot from 1/12/22

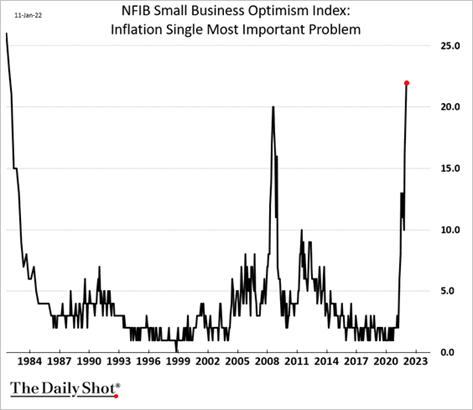

6. “Hello Houston…”

Source: The Daily Shot from 1/11/22

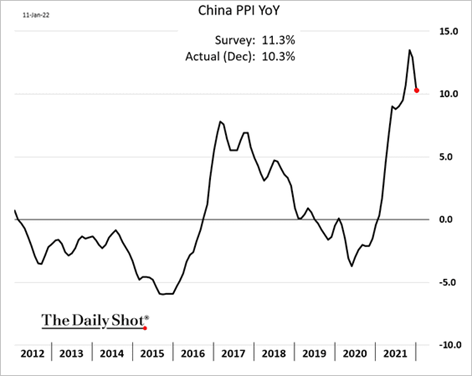

7. Producer price inflation was peaking, but with more than 25 million people contracting Covid in the last two weeks alone, what will happen next? Here are the world’s second and fourth largest economies. Please note the percentages:

Source: The Daily Shot from 1/11/22

Source: The Daily Shot from 1/12/22

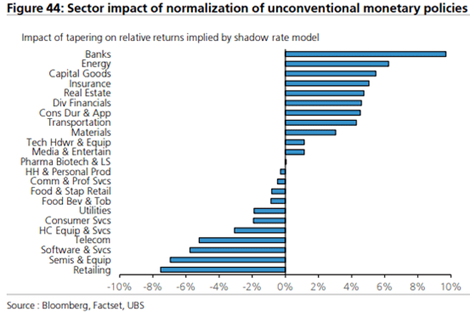

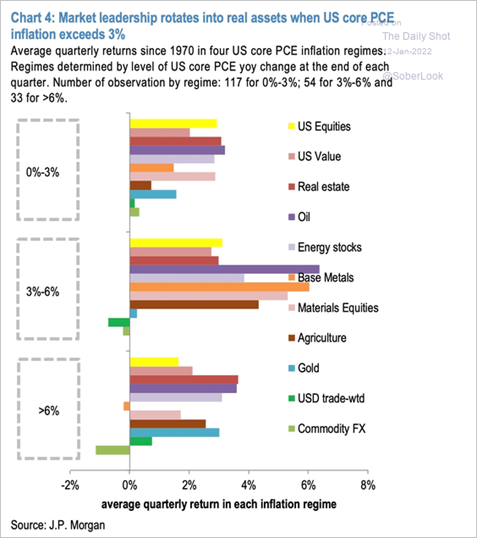

8. What are the effects of inflation on markets?

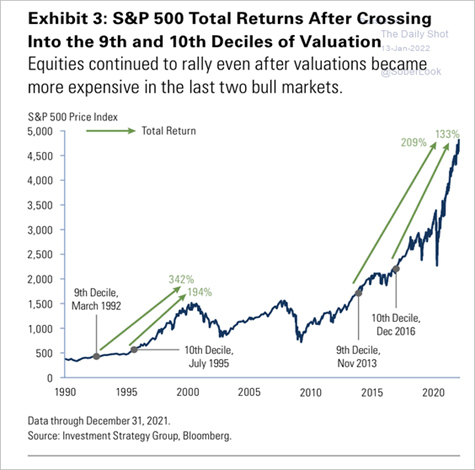

9. Now for the important question: Will rising yields derail the equity markets? By many measures, the markets are at extreme valuations:

Source: Goldman Sachs

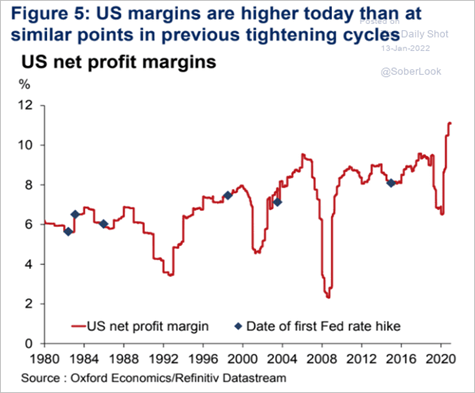

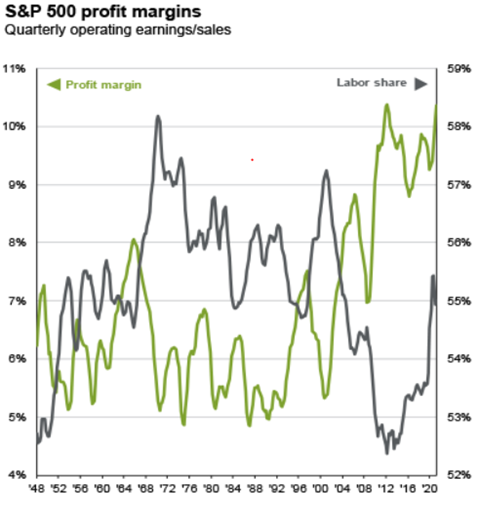

10. Equity valuations have been helped by profit margins. Will goods and labor inflation eat into these margins?

Source: Oxford Economics

Source: JP Morgan Guide to the Markets as of 12/31/21

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)