Service Sector Growth, Potential Inflation Triggers, and Has the 10-Year UST Hit Bottom?

January 25, 2021 | FIRESIDE CHARTS

The January Markit flash PMI report offered two pleasant surprises last week with manufacturing growth coming in above expectations and even the battered services sector surprising to the upside. Will this growth, in combination with a booming housing market and stimulus-induced liquidity, be enough to spark inflation? And if so, what can we expect from equities in response? Treasury yields meanwhile slipped on stimulus talks and climbing Covid concerns, but the 10-year UST has also doubled off the bottom. Could a trend reversal be ahead, even as high-yield issuances hit a 10-year YTD high?

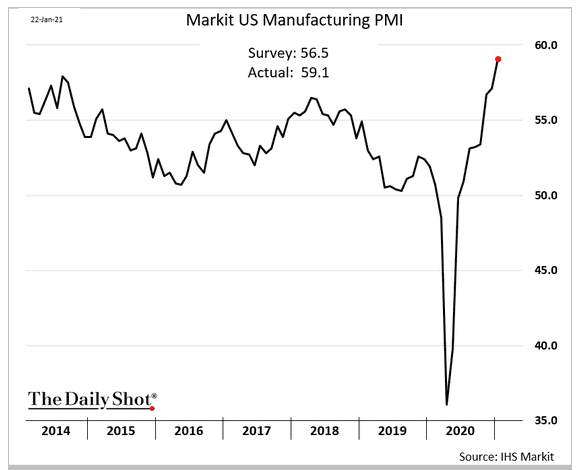

1. U.S. manufacturing continues to exceed expectations:

Source: The Daily Shot, from 1/25/21

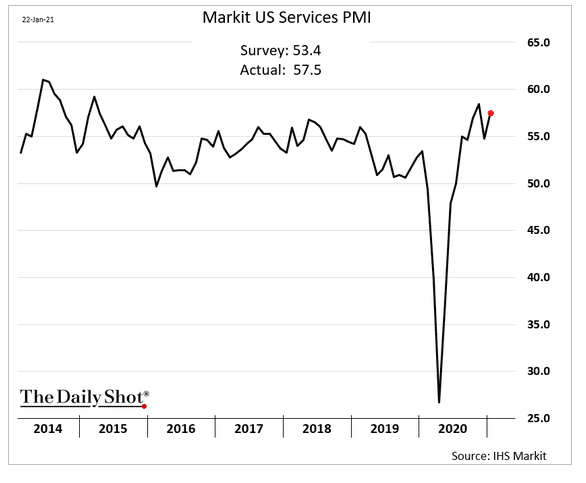

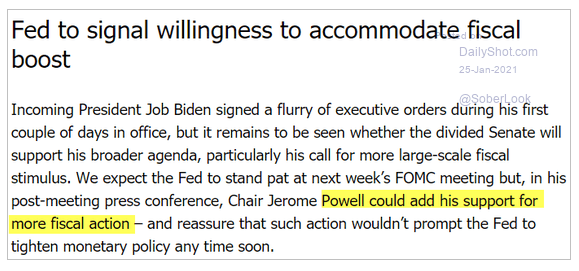

2. Since the service sector comprises about 70% of the economy, this result is even more significant and is in spite of the pandemic’s effect on many service sectors….

Source: The Daily Shot, from 1/25/21

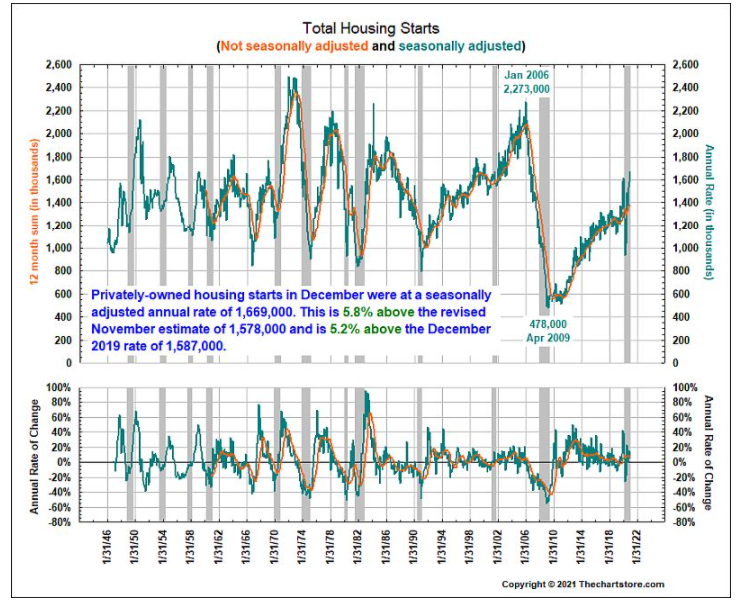

3. It has taken a decade, but U.S. housing is finally beginning to reach levels that will impact the growth in inflation…

Source: The Chart Store, from 1/25/21

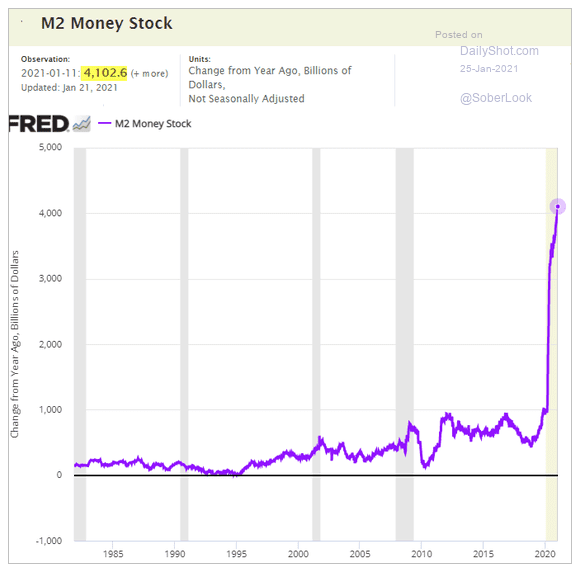

4. Our government’s and the Fed’s stimulus efforts has put $4 trillion of “extra” liquidity into the system. Not only can this be inflationary, it also has to eventually get paid back or withdrawn from the system…

Source: The Daily Shot, from 1/25/21

5. Meanwhile the likelihood of additional stimulus, Fed bond purchases, and the money supply will surge even higher. How much is too much?

Source: The Daily Shot, from 1/25/21

6. Instead of a blast of money to all families making $300,000 or less, would a more targeted approach to those who need the help the most make more sense?

Source: The Daily Shot, from 1/25/21

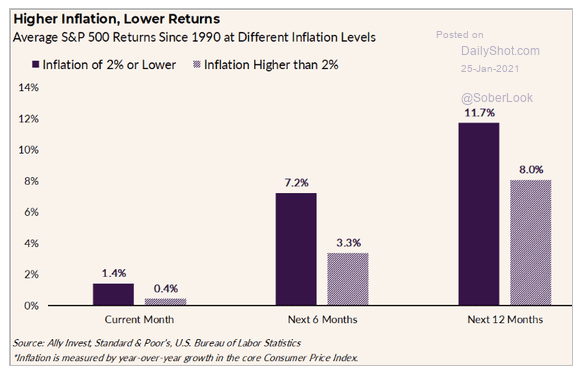

7. Historically, as inflation and eventually interest rates move higher, equities have faced a headwind. Part of the rally has been due to ultra-low rates and a paltry risk-free rate of return which have boosted equity’s relative appeal. Now static 60/40 portfolios will have to rely almost solely on the equity returns as bonds struggle with rising rates and near-zero coupons. Given the past, overall return expectations may be way ahead of reality…

Source: The Daily Shot, from 1/25/21

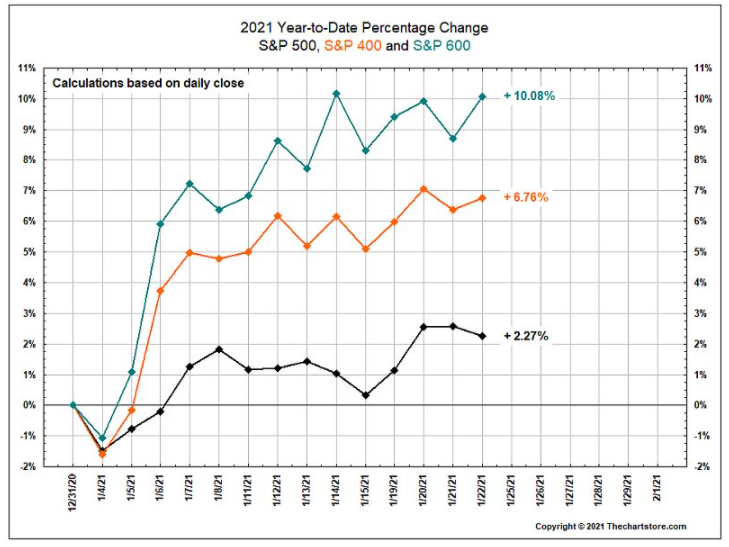

8. Half of the small cap surge came in one day…

Source: The Chart Store, from 1/25/21

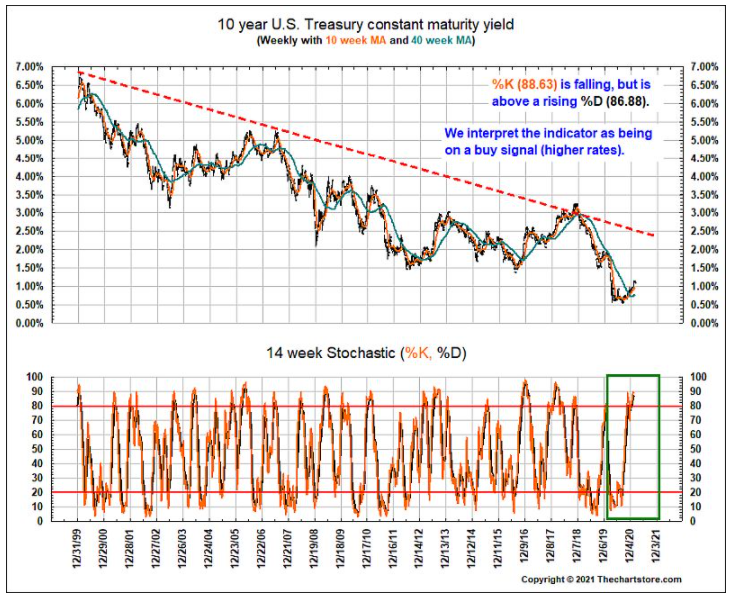

9. 10-year UST rates have doubled off the bottom. Was it really the bottom for the 35-year trend?

Source: The Chart Store, from 1/25/21

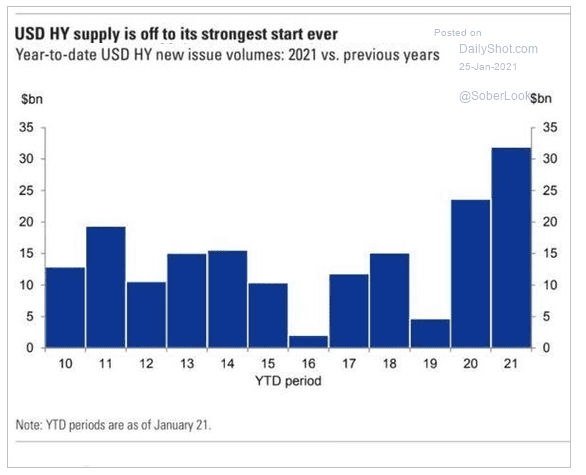

10. Companies whose financial conditions warrant junk status are taking advantage of the historically low rates and the insatiable appetite for yield…

Source: The Daily Shot, from 1/25/21

11. Is this ten-year downtrend broken as well?

Source: The Chart Store, from 1/25/21

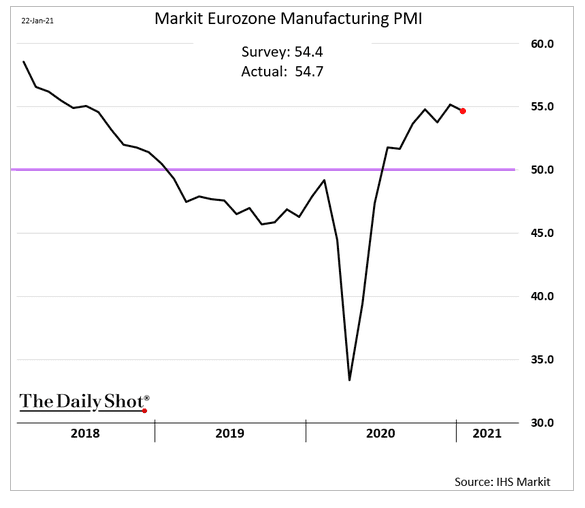

12. European manufacturing, while more tepid, is still solidly in expansion mode (reading greater than 50):

Source: The Daily Shot, from 1/25/21

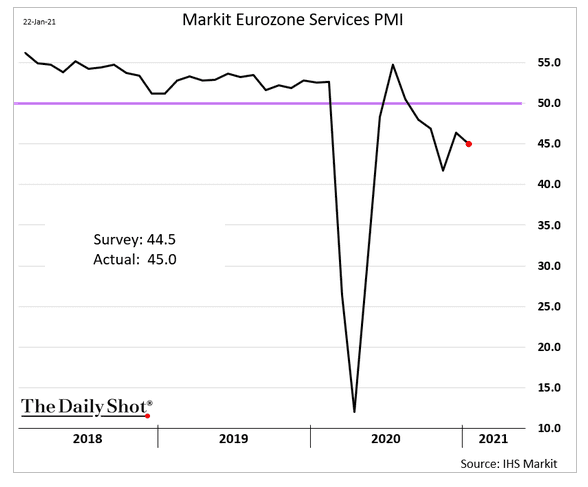

13. …And their service sector is still contracting under the weight of the pandemic and renewed shutdowns

Source: The Daily Shot, from 1/25/21

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)