Inflation as a Recession Indicator, Increased Consumer Spending, and Semiconductor Imports Above Recent Highs

June 10, 2022 | FIRESIDE CHARTS

China’s economy is beginning to re-open. While this is a positive development for the global economy, it may lead to increased oil demand at a time when supply is already tight. Historically, periods of high inflation in the U.S. have been followed by a recession. So far there’s no sign of a slowdown in consumer spending. Credit card debt has returned to pre-Covid levels, but consumers still have more in savings than they did prior to the pandemic. Mortgage rates are elevated relative to the 10-year treasury. Imports of semiconductors continue to surge. As supply chain issues are resolved, retailers may end up with more inventory than they need.

1. The Chinese government is declaring “victory” in it’s most recent battle with Covid:

Source: @GregDaco, Bloomberg Read full article

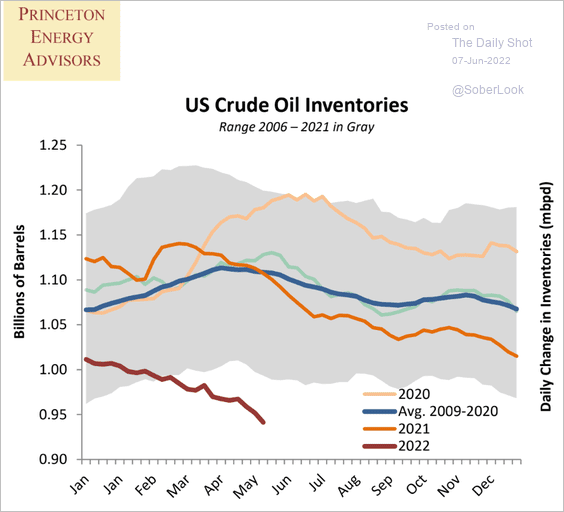

2. U.S. Oil inventories are at their lowest point in the past 15 years:

Source: Princeton Energy Advisors

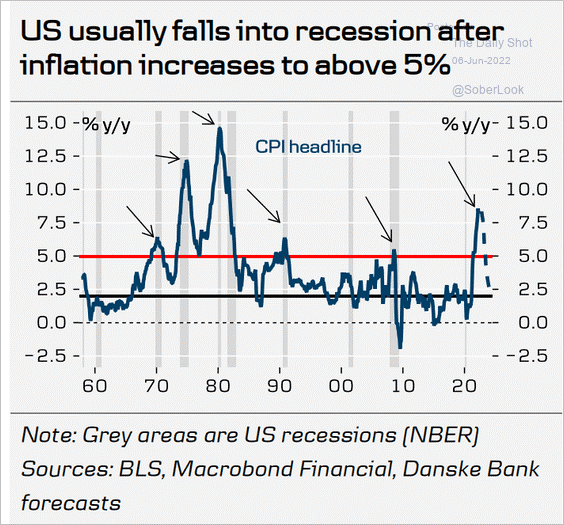

3. Rising inflation is often a late-cycle indicator, leading to tighter financial conditions and reduced consumer demand:

Source: Danske Bank

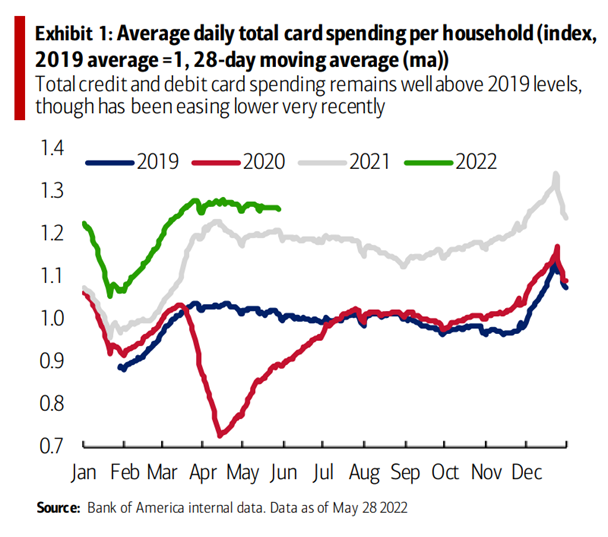

4. As noted by Bloomberg’s Joe Weisenthal “aggregate 2022 levels remain well above recent years. However [Bank of America] notes that total growth y/y is running below the headline rate of inflation, which means that real consumption may be running lower — people are spending more but taking home less real stuff”:

Source: Bloomberg, Five Things to Start Your Day

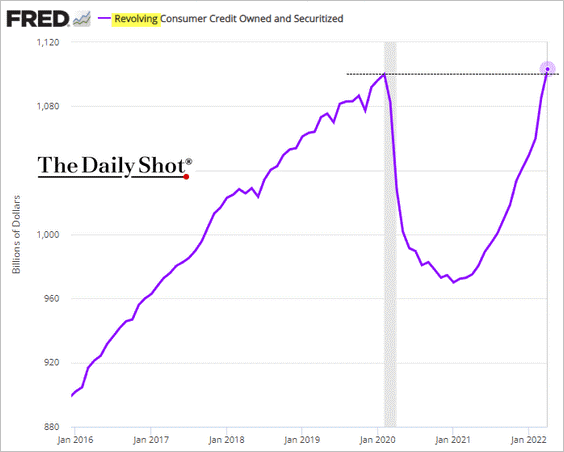

5. Higher credit card debt may be a function of spending returning to “normal” as opposed to a stressed consumer:

Source: The Daily Shot from 6/8/22

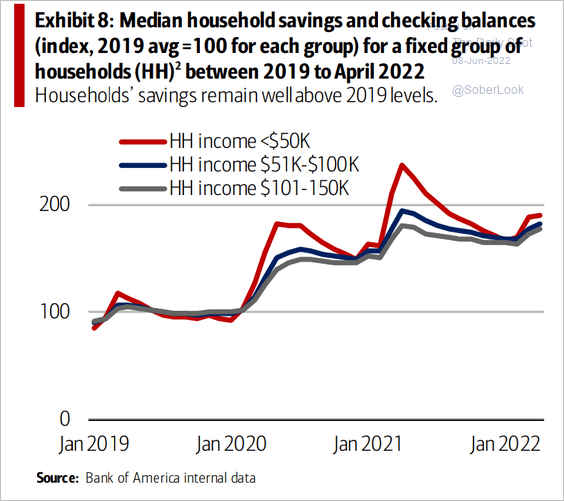

6. Household savings and checking balances remain nearly double pre-pandemic levels:

Source: @SamRo, BofA Read full article

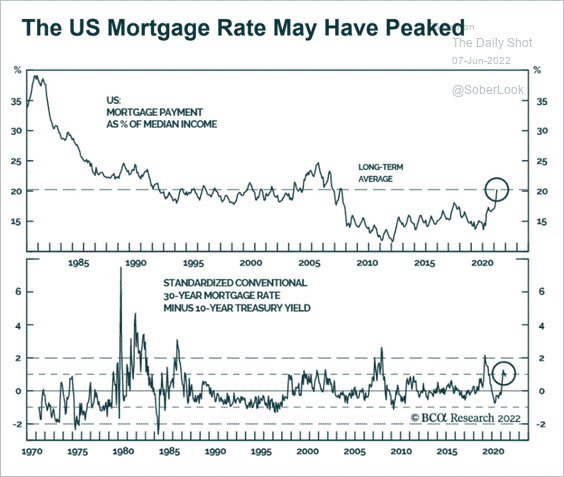

7. Mortgage-backed securities may be attractive due to their relatively higher yield:

Source: BCA Research

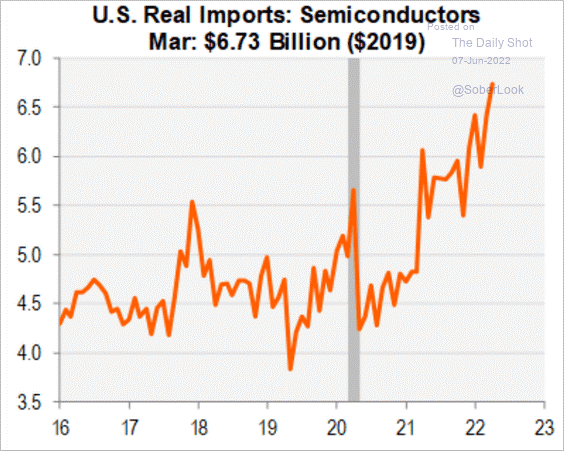

8. More semiconductors could help alleviate shortages in key industries, most notably automobiles:

Source: Piper Sandler

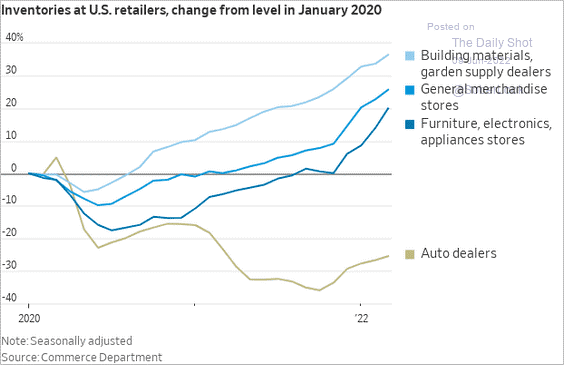

9. Retailers may want higher inventories to mitigate the impact of future supply chain issues, or they may have simply misjudged the level of future demand:

Source: @WSJ Read full article

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)