Global Manufacturing at ~2-year High, Soaring Government Debt, and Europe’s Second Wave

October 7, 2020 | FIRESIDE CHARTS

Global manufacturing growth has staged a massive recovery to hit a ~2-year high, but cost cutting in other nations is causing a headache for the U.S. as the trade deficit surges to $67.1 billion—its highest level in 14 years. As the debate (and messaging) around additional stimulus measures wears on, federal and local government debt has already soared to historic heights and is raising concerns about both inflation and a potential oversupply of muni bonds. Over in Europe, a second wave of infection has taken hold and already dealt a blow to the Eurozone services PMI. Could this further erode the region’s already-shrinking share of global GDP?

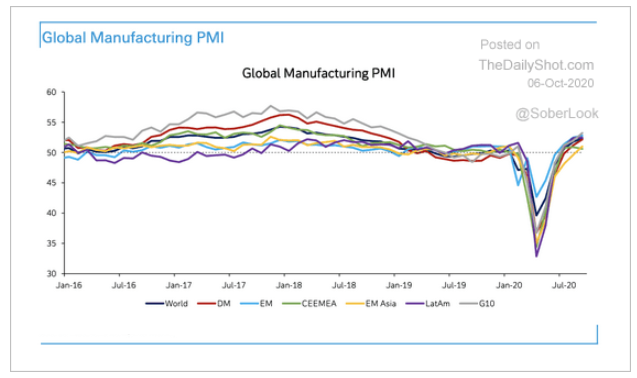

1. It’s as if nothing ever happened, right?

Source: The Daily Shot, from 10/6/20

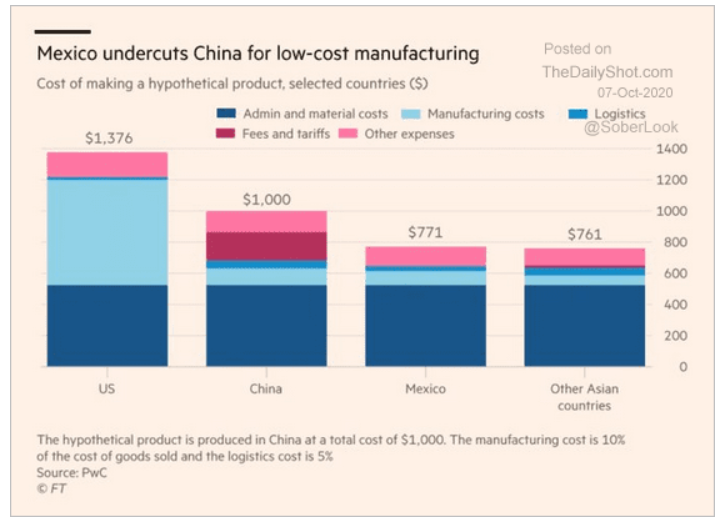

2. A major reason why U.S. companies still want to move manufacturing overseas…although the geography is shifting with the costs…

Source: The Daily Shot, from 10/7/20

3. Massive amounts of new government debt are raising inflation expectations. This has been countered by a Fed with “unlimited” QE and a pledge to keep rates low through at least 2023. Are we going to see an epic battle unfolding?

Source: The Daily Shot, from10/6/20

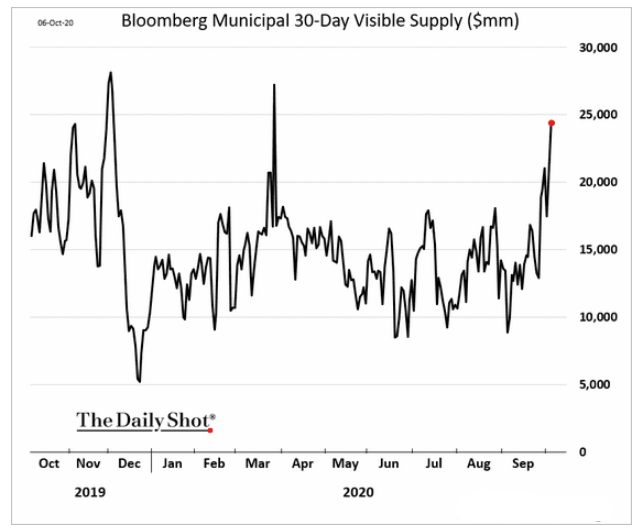

4. Given the legal necessity to balance town, city and state budgets, will we see a lot more muni bond supply in the months ahead? Will supply overwhelm demand and cause a rise in rates?

Source: The Daily Shot, from 10/6/20

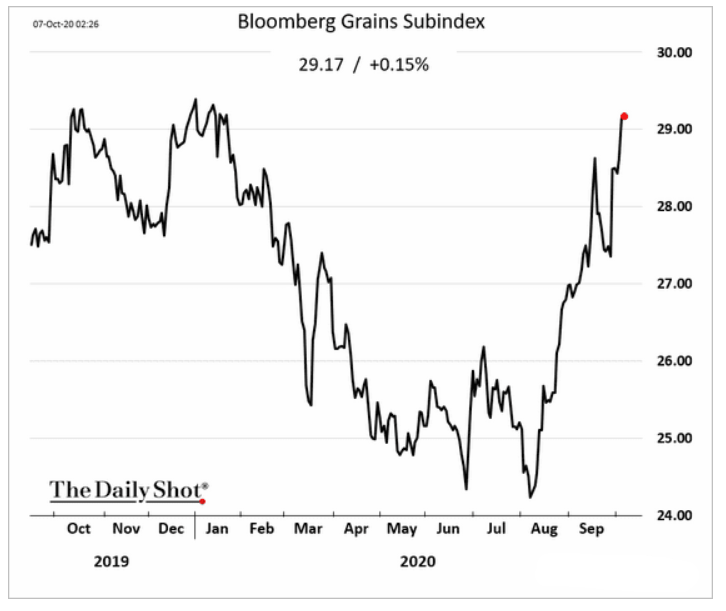

5. This looks like good news for U.S. farmers, but prices are rising largely due to drought…

Source: The Daily Shot, from 10/7/20

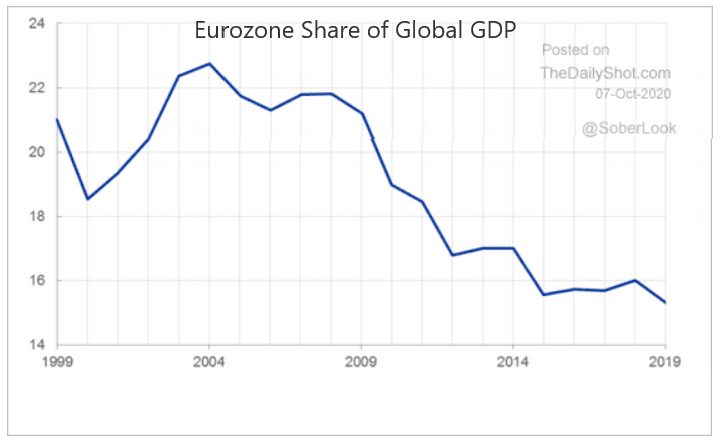

6. Europe’s economy is shrinking relative to the rest of the world. When will the trend reverse?

Source: The Daily Shot, from 10/7/20

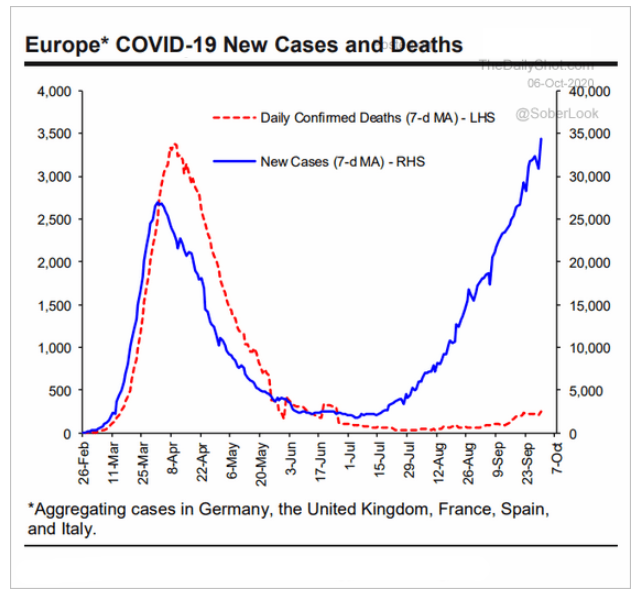

7. Europe’s second wave of Covid is already exceeding the first…

Source: Scotiabank, GMB Potfolio Strategy; Bloomberg, from 10/6/20

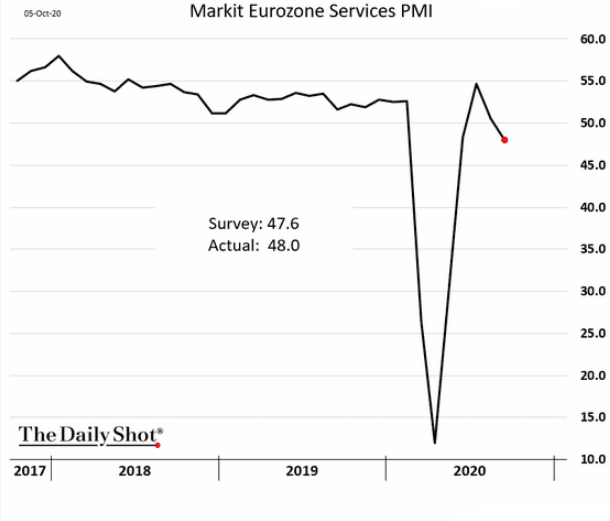

8. …This may be hindering their services PMI as consumers hunker down again…

Source: IHS Markit, from 10/6/20

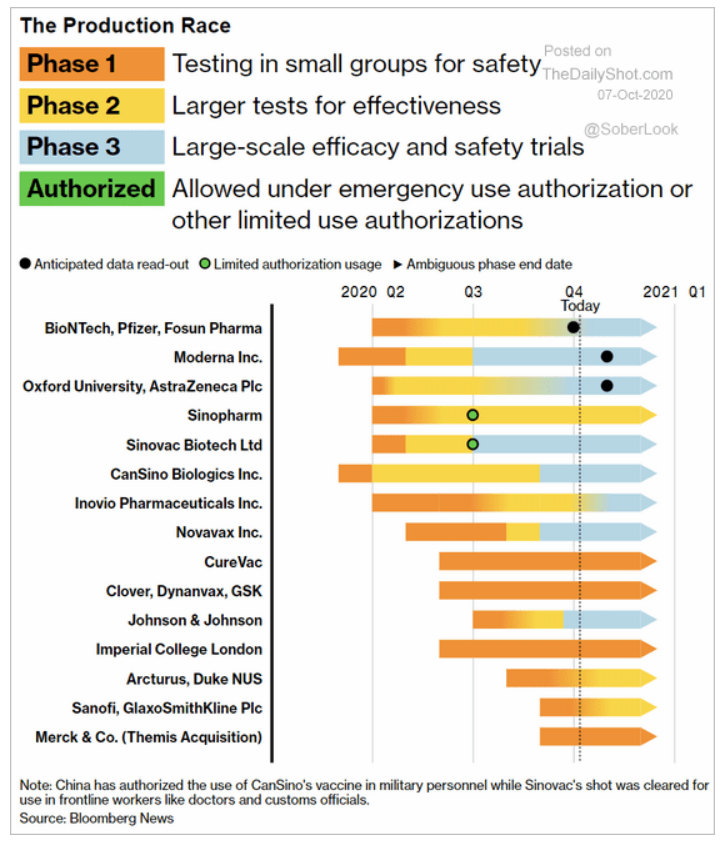

9. An update on the race for a vaccine:

Source: The Daily Shot, from 10/7/20

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.