Service Sector Growth Surpasses Forecasts, U.S.-China Trade Deficit Hits Record, and Earnings’ Diluted Effect on Pricing

October 26, 2020 | FIRESIDE CHARTS

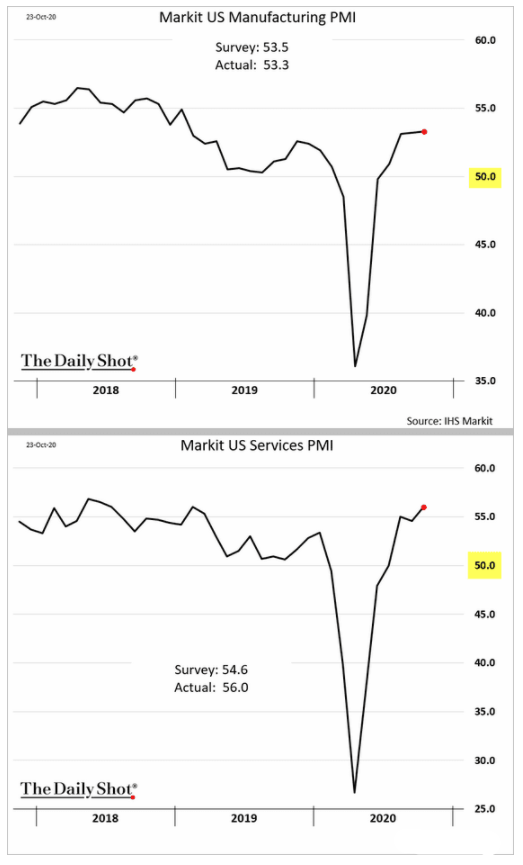

The U.S. saw continued growth in both the manufacturing and services sectors in October according to the preliminary Markit PMI report. The services sector, which has been slower to recover in the wake of the initial Covid shutdowns, exceeded forecasts to come in at 56.0. Despite the strong growth from manufacturing though, the U.S. trade deficit with China has reached an all-time high, as have Chinese exports to the U.S. And in a big week for earnings—about 30% of the S&P 500® Index reports this week—we’re seeing once again how performance can diverge dramatically from earnings. Are we poised to see more of the same this week?

1. Most of the economy, including manufacturing and services, were doing well in October. Now comes Covid test #2, or is it #3?

Source: The Daily Shot, from 10/26/20

2. Have we lost the trade war?

Source: The Daily Shot, from 10/26/20

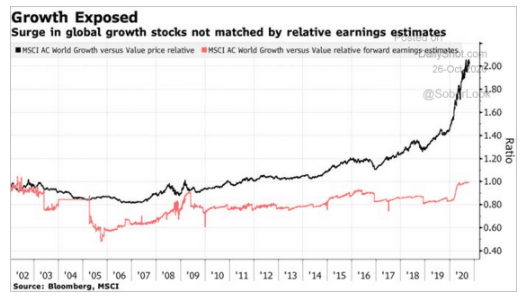

3. Looking past the pandemic is one thing, but when will the reality of earnings versus current prices kick back in?

Source: The Daily Shot, from 10/26/20

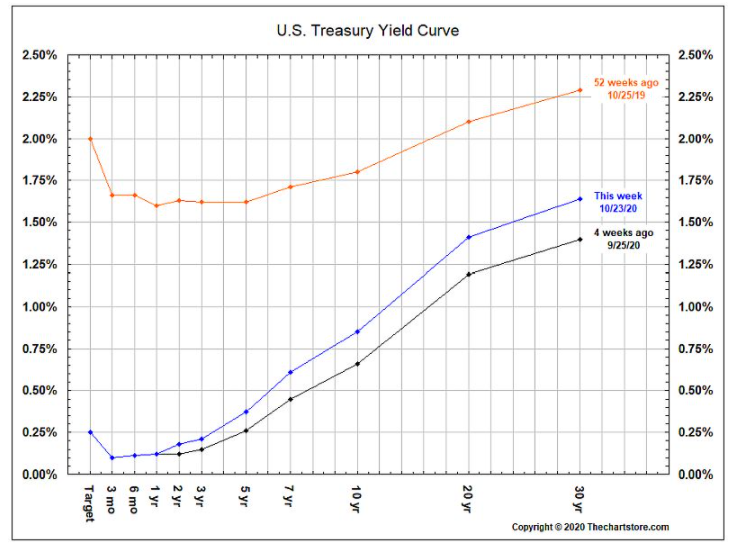

4. “Don’t fight the Fed?” The yield curve shape has “normalized” as the yield curve inversion, save for 90 days or less, has disappeared with rising rates…

Source: The Chart Store, from 10/26/20

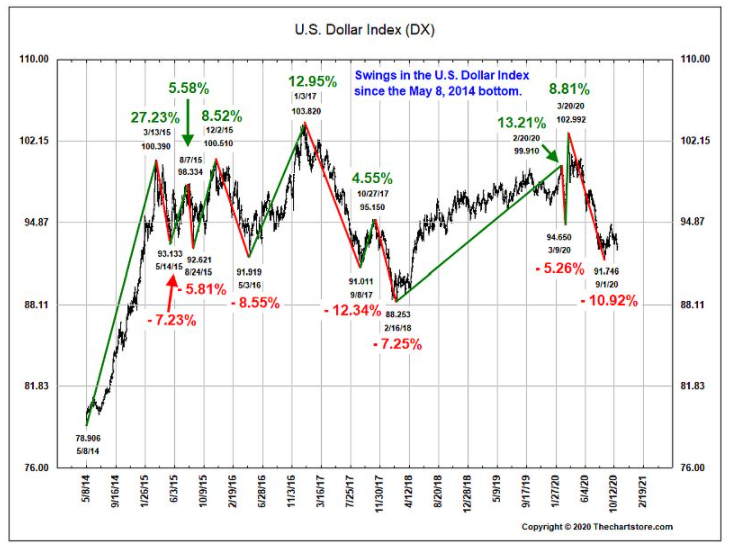

5. Will rising rates here at home put a bid under the US dollar or will the trillions of new debt win the tug-of-war?

Source: The Chart Store, from 10/26/20

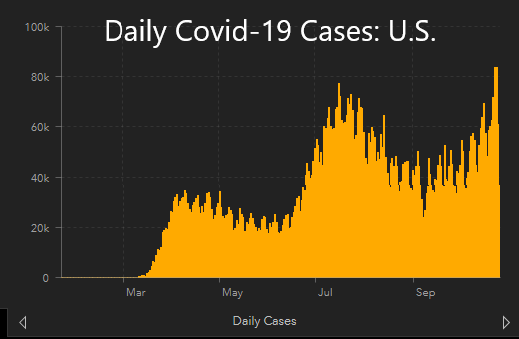

6. Saturday set the new global daily Covid case record at over 500,000. The U.S. (below) is now running 80,000+/cases a day. At this pace we will have over 1/2 million new confirmed cases this week…

Source: JHU CSSE, as of 10/26/20

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.