Core CPI Softer than Expected, Americans Revisit a Pre-Financial Crisis Trend, and Yields Climb Yet Again

March 12, 2021 | FIRESIDE CHARTS

U.S. core CPI growth remained sluggish in February—working to calm the inflation fears that have been driving market movement in recent weeks—and the Dow hit a new record in response. Did the effect carry through to treasury yields though? The decline in used vehicle purchases contributed to the weakness in core CPI and it has us wondering how other industries that thrived during the early days of the pandemic will fare through the recovery. Meanwhile, the $1.9 trillion stimulus bill became law yesterday on the one-year anniversary of the pandemic. While the percentage of stimulus checks destined for savings and investment accounts remains a concern, unemployment continues to weigh heavily on the U.S. and we’re hoping the package will offer the 1 million+ new weekly filers and nearly 20 million continuing filers some relief. Especially as it appears a growing number of Americans could be revisiting a pre-financial crisis trend in the search for funding… U.S. value stocks, meanwhile, are having one of their best stretches in nearly two decades. Will it continue as the nation begins to emerge from the Covid crisis?

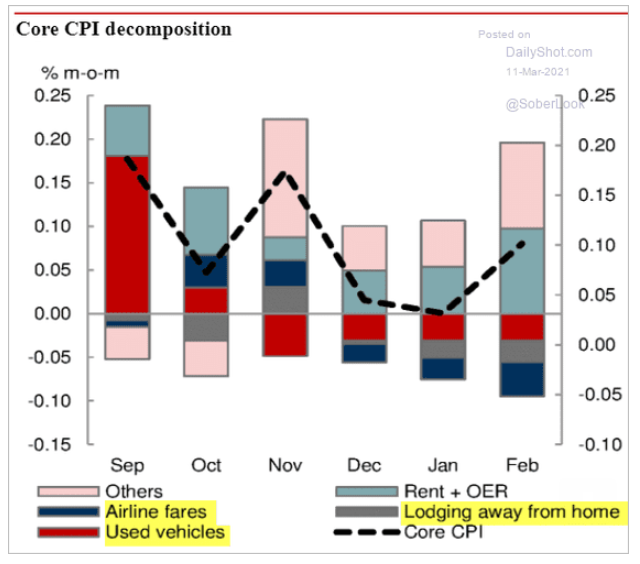

1. While the headline CPI rose as expected to 1.7%, the core CPI was a bit softer, weighed down by the Covid factor in obvious industries.

Source: The Daily Shot, From 3/11/21

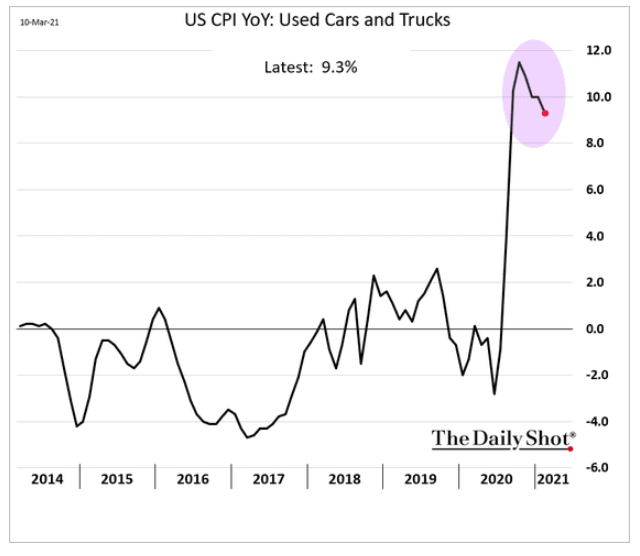

2. Some segments of the economy saw intense Covid-induced surges. Will this pulling sales from the future affect other industries that thrived under Covid?

Source: The Daily Shot, From 3/11/21

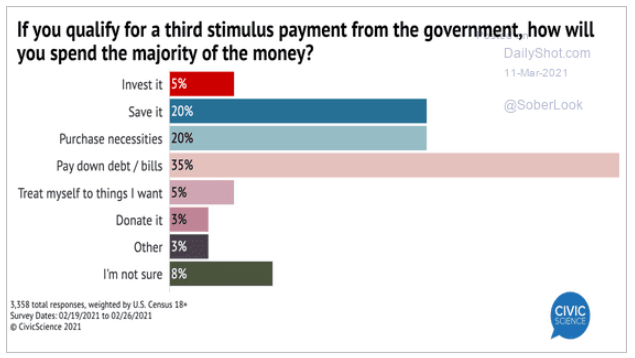

3. “Stimu-less”? Only 25% of Americans plan to spend their new checks…

Source: The Daily Shot, From 3/11/21

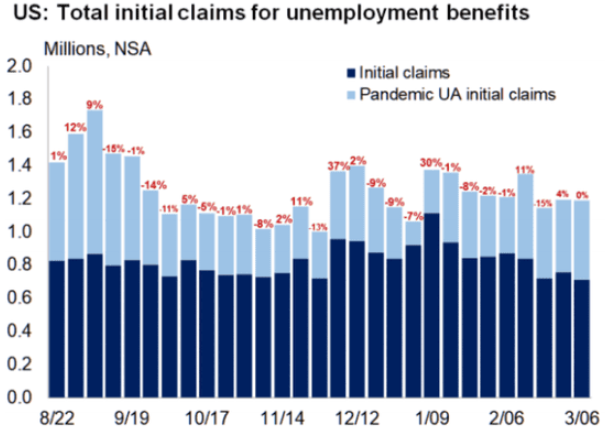

4. While U.S. unemployment is dropping, the Covid factor is still at work (pun intended) with over 1 million weekly NEW claims:

Source: Oxford Economics/ Haver Analytics, From 3/12/21

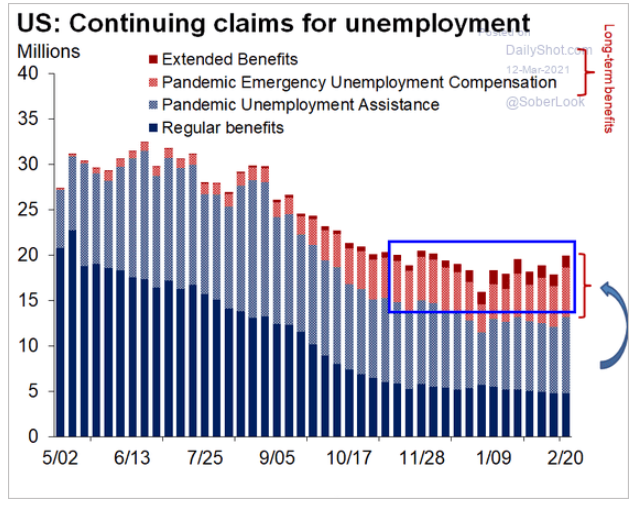

5. And almost 20 million continuing claims:

Source: The Daily Shot, From 3/12/21

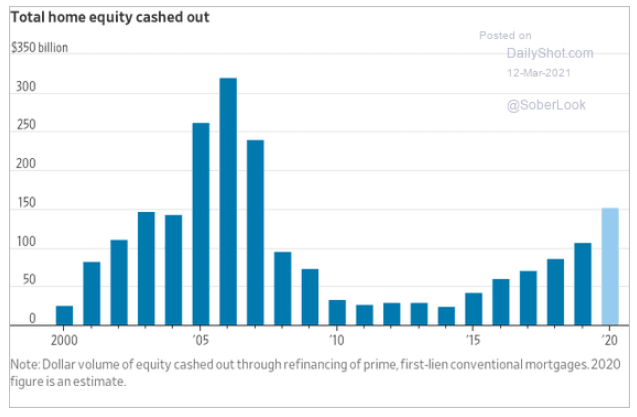

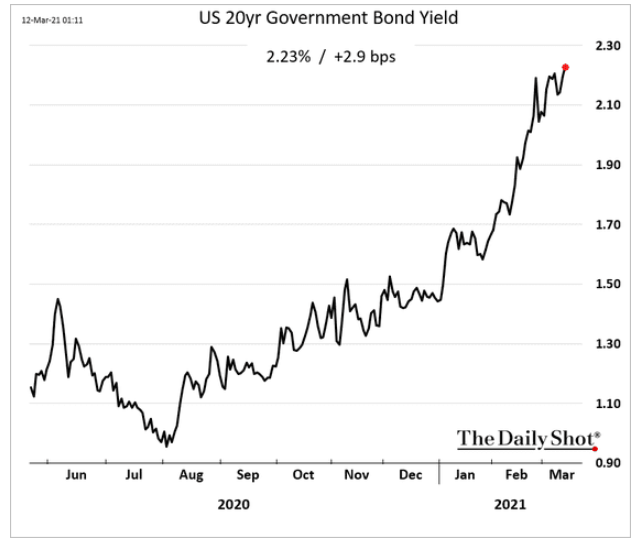

6. Oh, boy! Here we go again?

Source: The Daily Shot, From 3/12/21

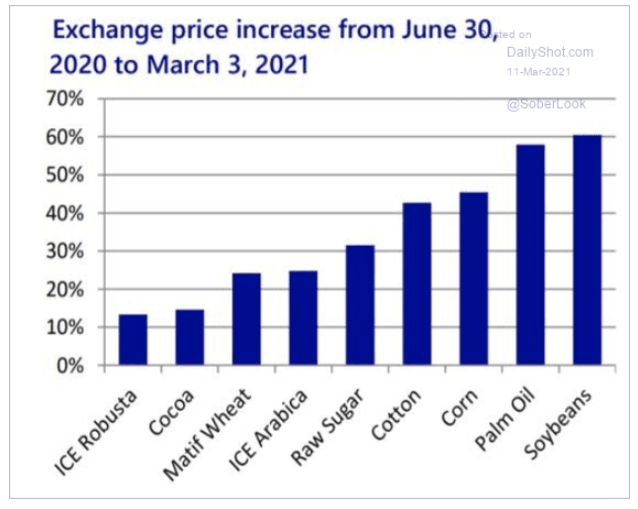

7. Good news for our farmers, bad news at the supermarket:

Source: The Daily Shot, From 3/11/21

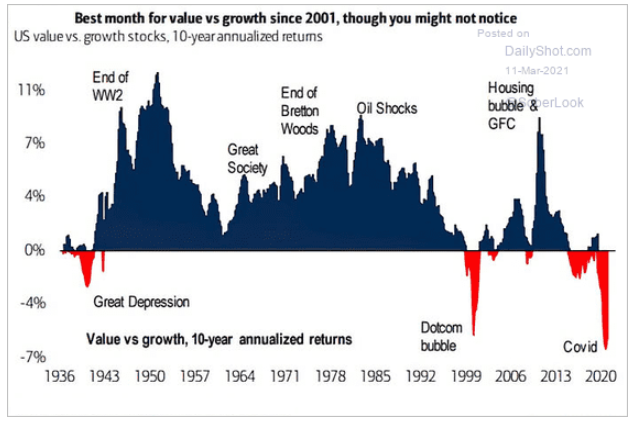

8. A great historical perspective on growth versus value:

Source: BofA Research, From 3/11/21

9. Last night the Bank of England became the second central Bank to take action against rising rates by extending their QE program. Yet U.S. yields resumed their ascent with the ten year UST hitting 1.6% and longer yields rising as well. Yes, rates matter as the NASDAQ futures are off 1.8% this morning…

Source: The Daily Shot, From 3/12/21

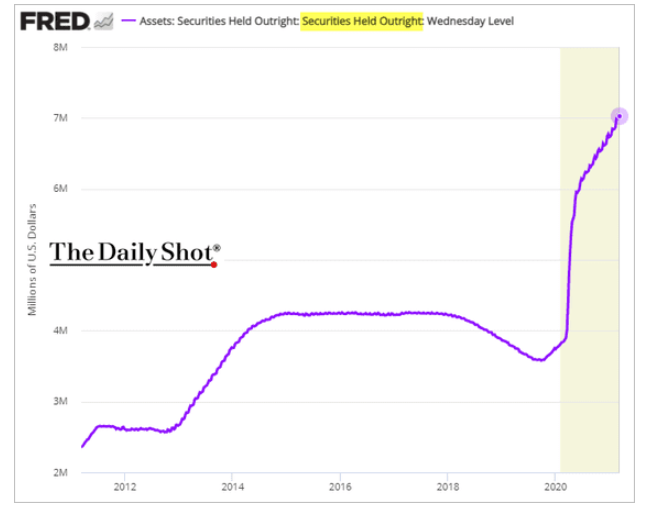

10. The FED also continues its own QE, but with $1.9 trillion of new financing required by the latest stimulus package, the markets “are fighting the FED”…

Source: The Daily Shot, From 3/12/21

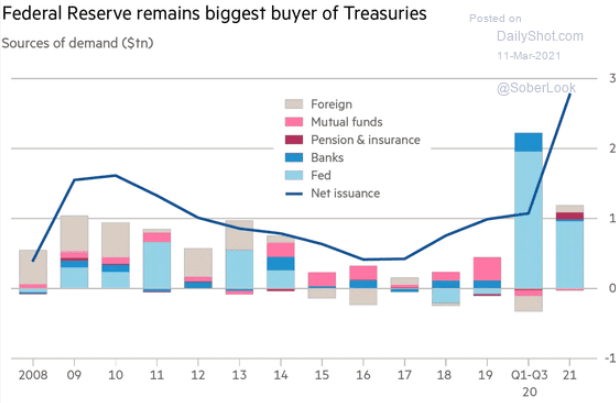

11. Who is going to buy the next $1.9 trillion?

Source: The Daily Shot, From 3/11/21

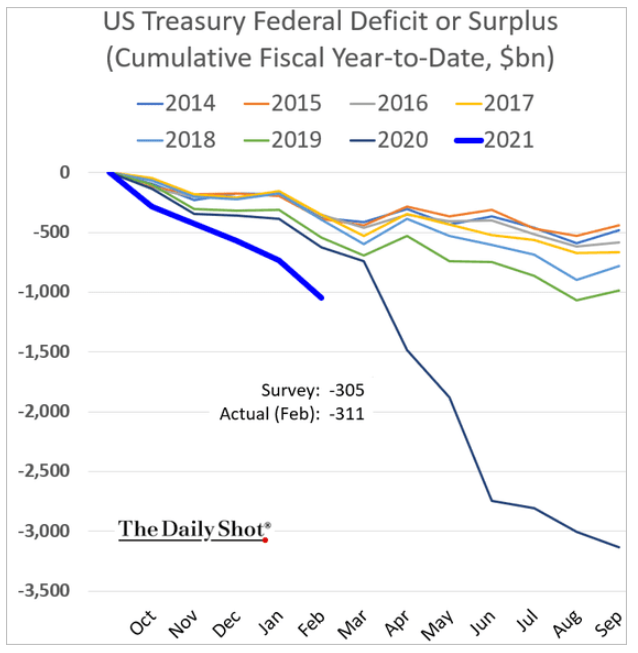

12. It is mid-March and our government’s deficit spending has already exceeded every full-year deficit pre-Covid. This is not free money, we will have to pay it back…

Source: The Daily Shot, From 3/11/21

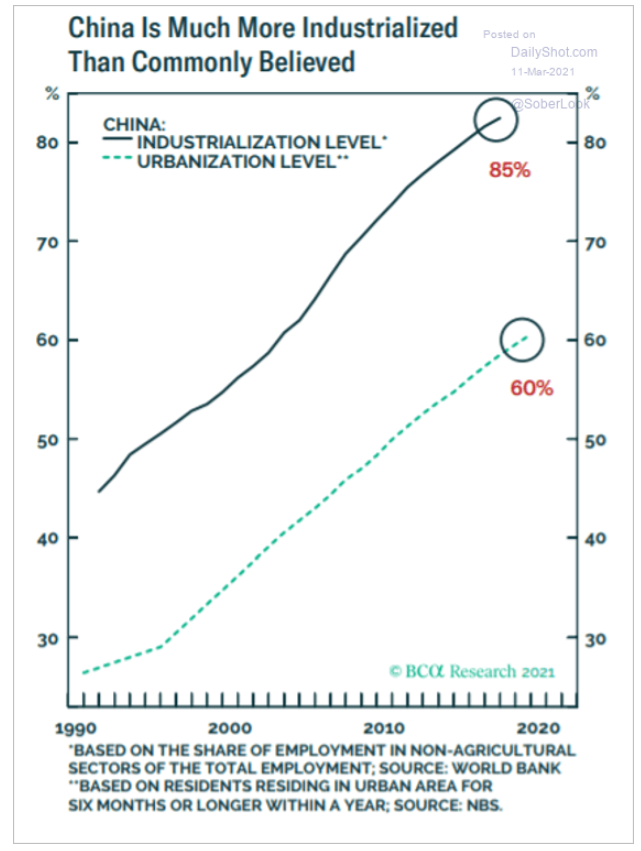

13. Is it time to recategorize the world’s largest economy from emerging to developed?

Source: The Daily Shot, From 3/11/21

14. And we get frustrated by cell phone chargers!

Source: The Daily Shot, From 3/12/21

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.