Trade Deficit Now Largest on Record, Putting Inflation in Context, and Equities’ Historic 12-Month Run

March 29, 2021 | FIRESIDE CHARTS

The trade deficit widened 2.5% in February to hit a record high of $86.7 billion and the budget deficit is feeling its own strain as stimulus payments go out and QE reignites. At long last though, consumer spending does look to be responding to stimulus payments in a trend we hope will continue. As much as the economic recovery has stoked inflation anxiety—putting pressure on both the equity and fixed income markets—are the 5-10 year expectations really any higher than long-term averages? And if inflation does take off, could a look at asset class performance during the ‘70’s offer any insight into what may lie ahead? Meanwhile, as indices hit new record highs yet again, with Dow Transports and S&P 400® Index mid-caps both seeing 120%+ gains from their print lows last March, we’re wondering if we’re seeing more cases of “too far, too fast”. Is it time for a cooling off period?

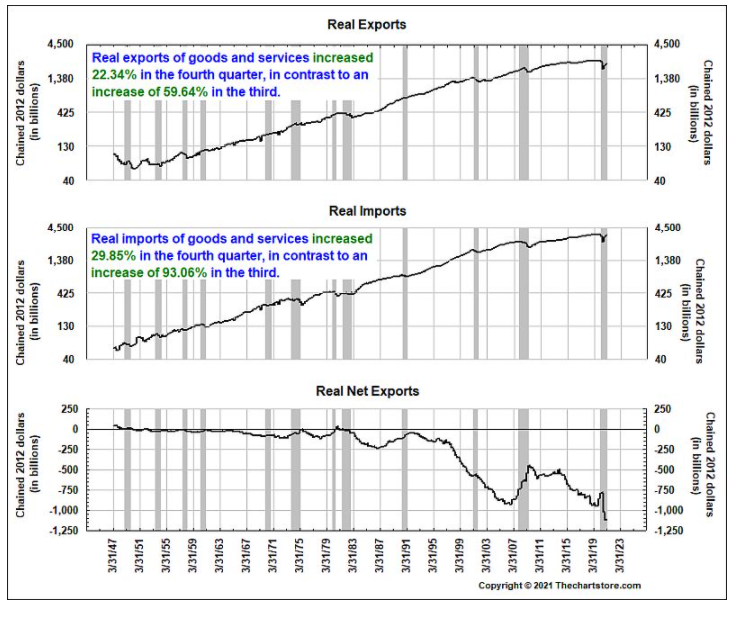

1. Remember the trade war(s)? Our trade deficit is now the largest it has even been:

Source: The Chart Store, from 3/29/21

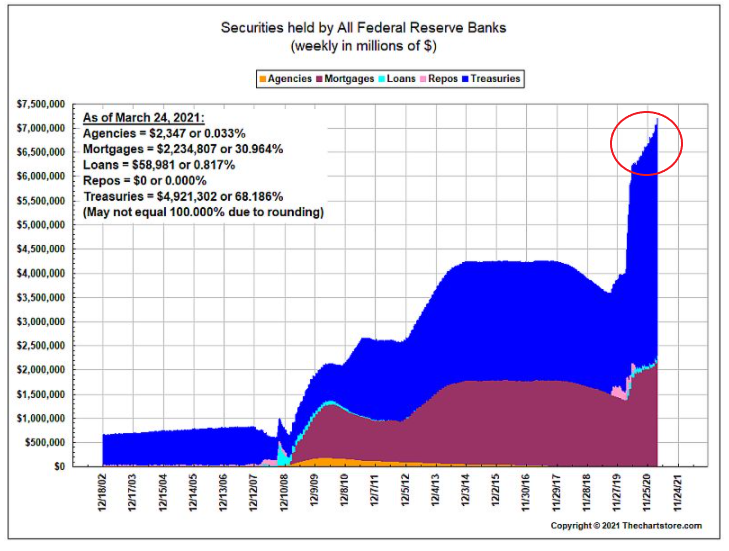

2. The FED’s QE machine has kicked in again to help finance the new $1.9 trillion of stimulus.

Source: The Chart Store, from 3/29/21

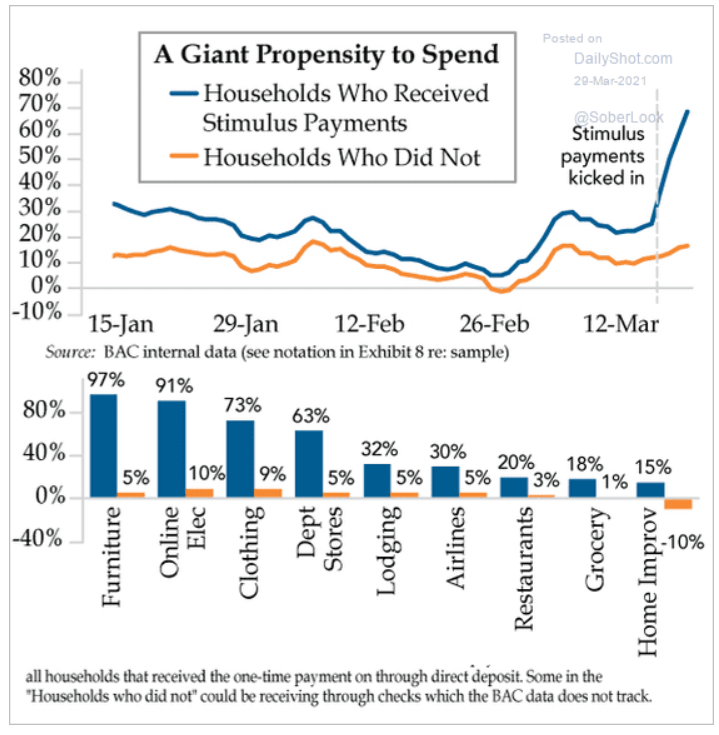

3. With light at the end of the Pandemic tunnel, will Americans actually spend their stimulus this time?

Source: The Daily Shot, from 3/29/21

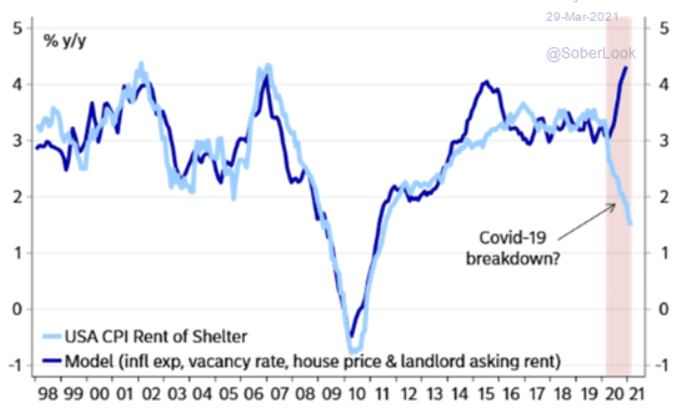

4. More evidence that the Covid factor is affecting CPI…

Source: The Daily Shot, from 3/29/21

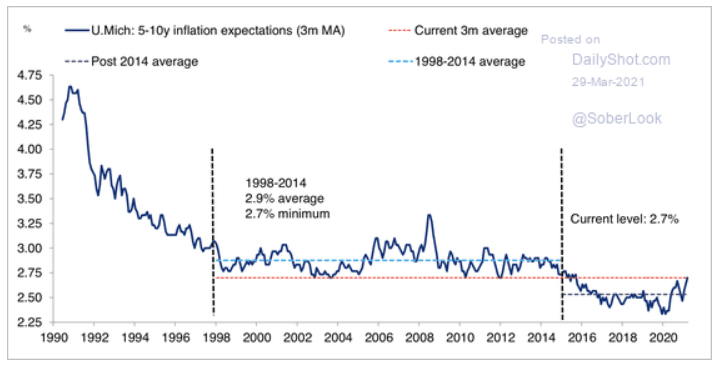

5. Historically, what are our inflation expectations?

Source: The Daily Shot, from 3/29/21

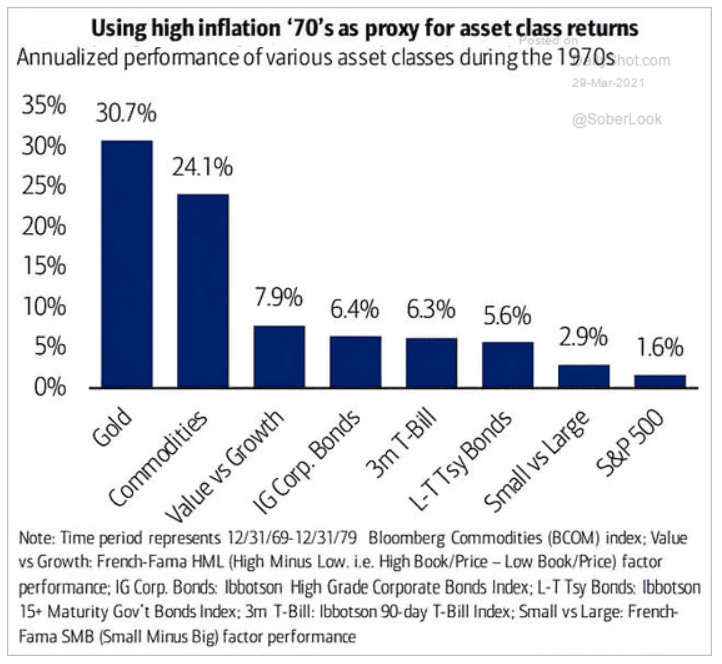

6. Interesting, but so much has changed….

Source: The Daily Shot, from 3/29/21

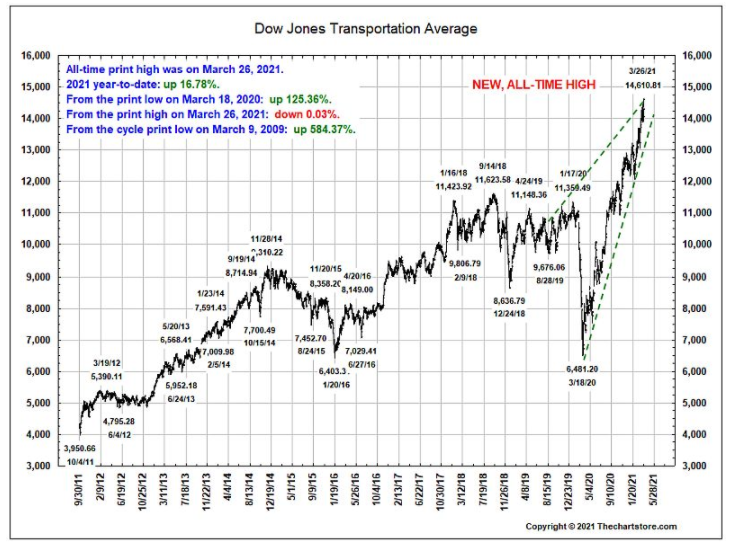

7. The stock market steam roller continues, but we note that no market can go up at a 75-degree angle “forever”…

Source: The Chart Store, from 3/29/21

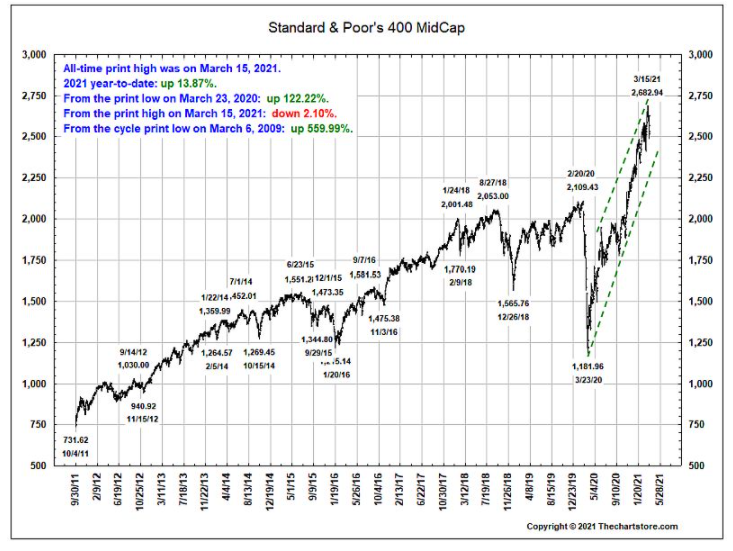

8. Doubling in 10 months, another example of too far, too fast?

Source: The Chart Store, from 3/29/21

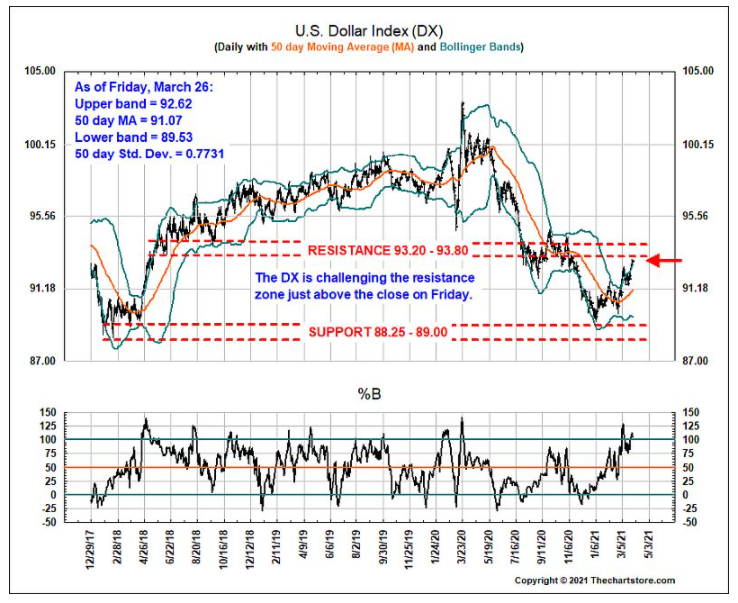

9. Relatively high interest rates and the safe-haven status have been giving the USD a bid, but it looks extended:

Source: The Chart Store, from 3/29/21

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.