Service Sector Surprises to the Upside, Growing Inflation Expectations, and Could Small Caps Finally Be Poised to Climb?

January 8, 2021 | FIRESIDE CHARTS

The ISM Services PMI offered a pleasant surprise this week as the U.S. service sector continues to expand at a promising pace. Inflation expectations are climbing as officials continue their unprecedented efforts to spark growth…will people be prepared when it finally arrives? Meanwhile, as mortgage rates hit another record low, office vacancies in Manhattan soar to a record of their own. And following a tumultuous week that—among other headline events—saw Democrats win a majority in the Senate, we’re looking at return patterns established during similar governing scenarios to see what may be in store come January 20th.

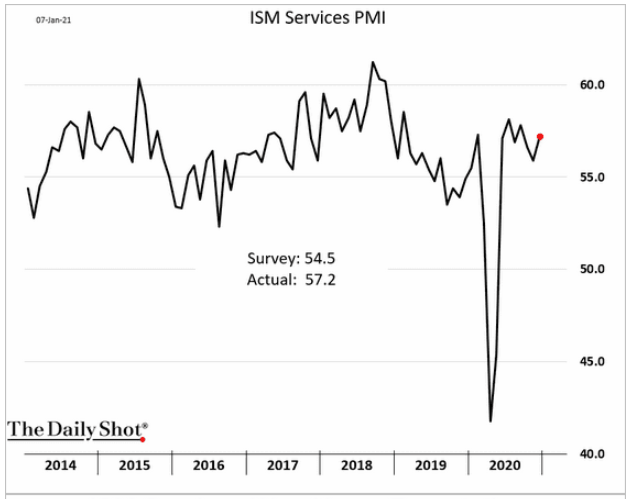

1. Since about 70% of our economy is based on services, this is great news in the face of the pandemic…

Source: The Daily Shot, from 1/8/21

2. Market inflation expectations spent much of 2020 recovering, then consolidating, and now appear to be in another up-leg. Inflation is not fun, so we (and the Fed) should be careful what we wish for…

Source: The Daily Shot, from 1/7/21

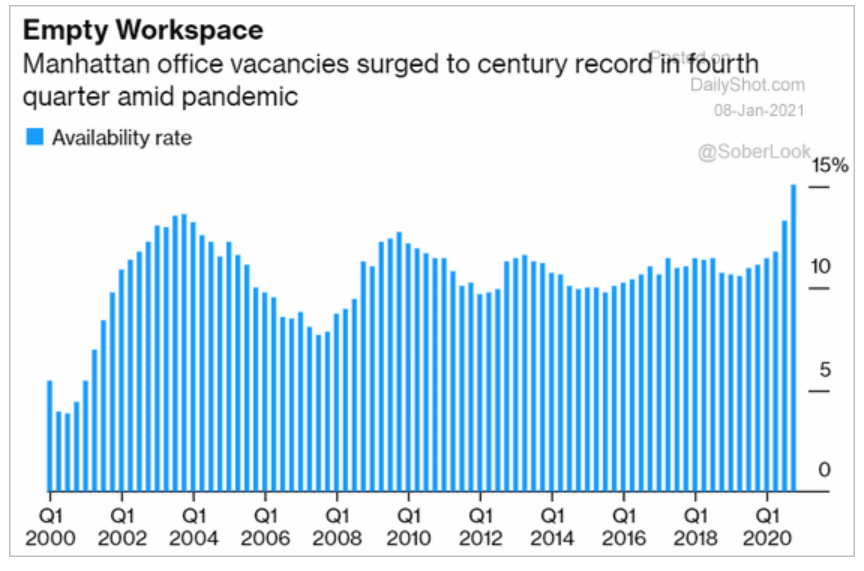

3. What will the long-term implications be on rents and office space?

Source: The Daily Shot, from 1/8/21

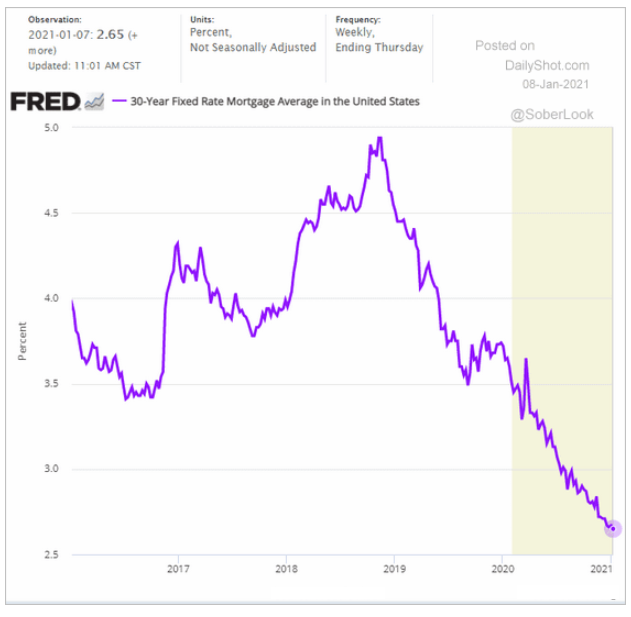

4. Despite longer-term interest rates edging higher, mortgage rates continue to move lower?

Source: Freddie Mac, from 1/8/21

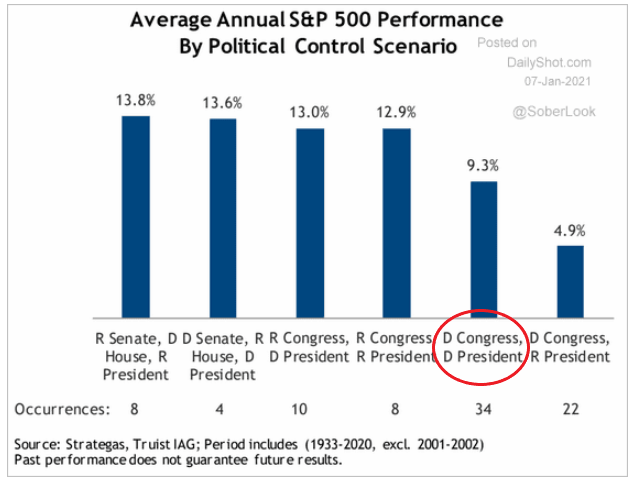

5. Now that the elections are complete, here is a look at the historic average returns under each governing scenario:

Source: The Daily Shot, from 1/7/21

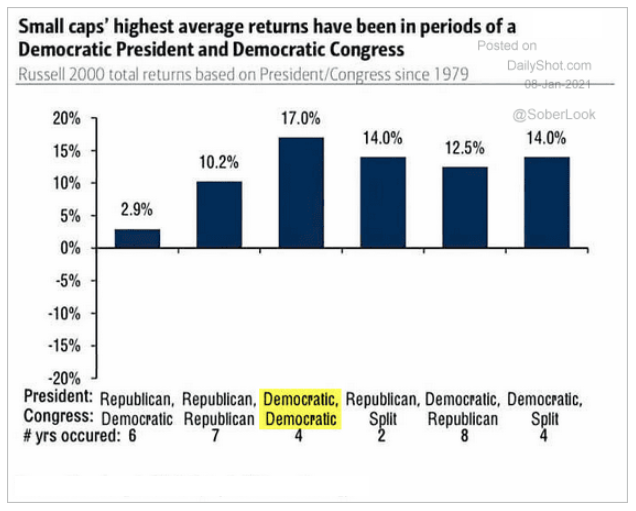

6. Unlike the broader markets, small caps have historically performed well under a Democratic President and Congress…

Source: Bloomberg, BofA Equity & US Quant Strategy, from 1/8/21

7. A modern Dutch bulb mania? At least tulips look nice when they bloom…

Source: The Daily Shot, from 1/7/21

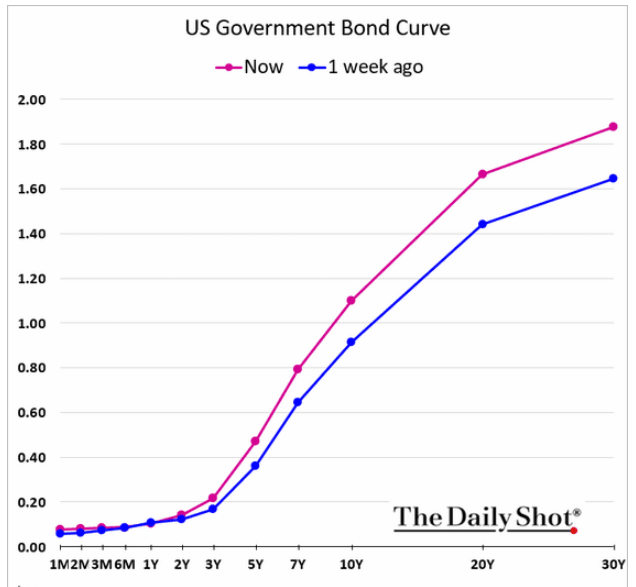

8. The long end of the yield curve steepened substantively over the past week. How will the Fed, with a near-zero policy declared through 2023, respond?

Source: The Daily Shot, from 1/7/21

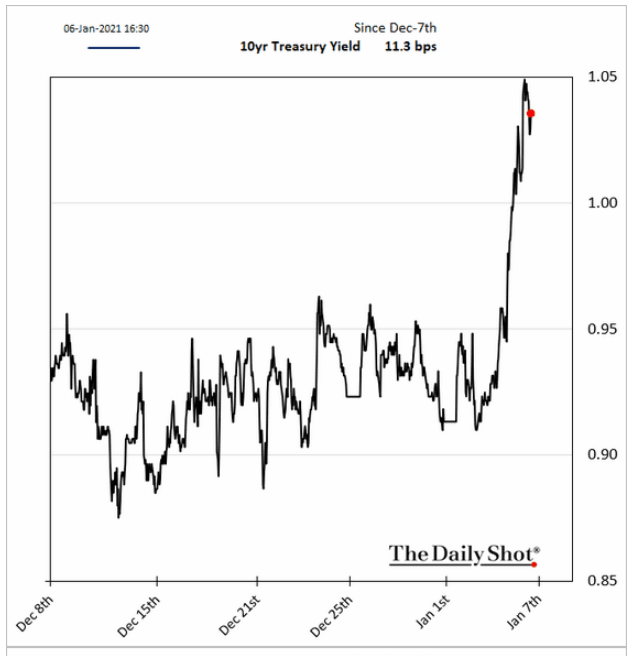

9. The Democratic sweep has many thinking of multiple scenarios that contribute to inflation/reflation. The bond markets responded by closing the 10-year UST yield above 1% for the first time since March 2020…

Source: The Daily Shot, from 1/7/21

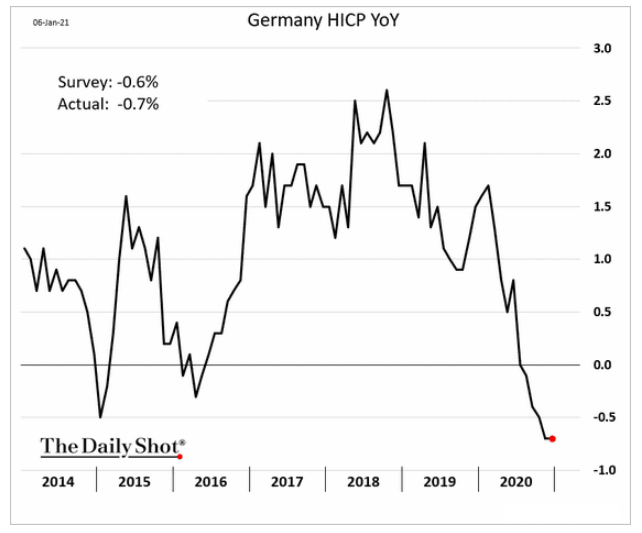

10. Inflation is subdued or even negative in Europe. Currency movement on both sides of the Atlantic is having an effect on inflation. As the USD weakens, foreign goods and services become more expensive and thus inflationary (The U.S. has a $1 trillion annualized trade deficit, exacerbating the effect). To Europeans, the strengthening Euro makes imports less expensive stoking lower inflation…

Source: HIS Markit, from 1/7/21

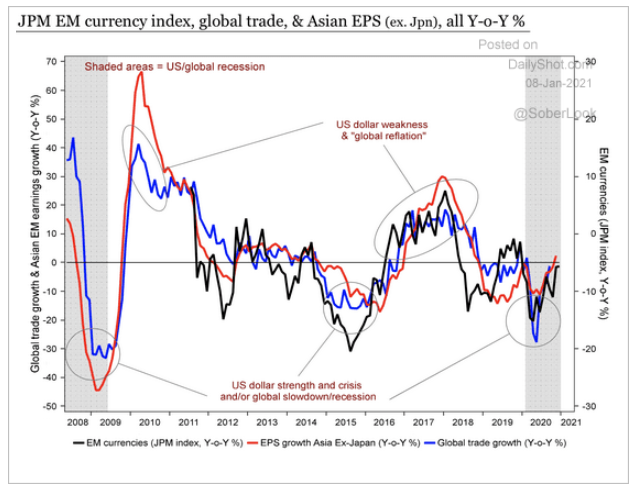

11. EM earnings, trade and currencies are all heading towards growth mode. Will this trend continue? Is it (finally) EM’s time to shine?

Source: The Daily Shot, from 1/8/21

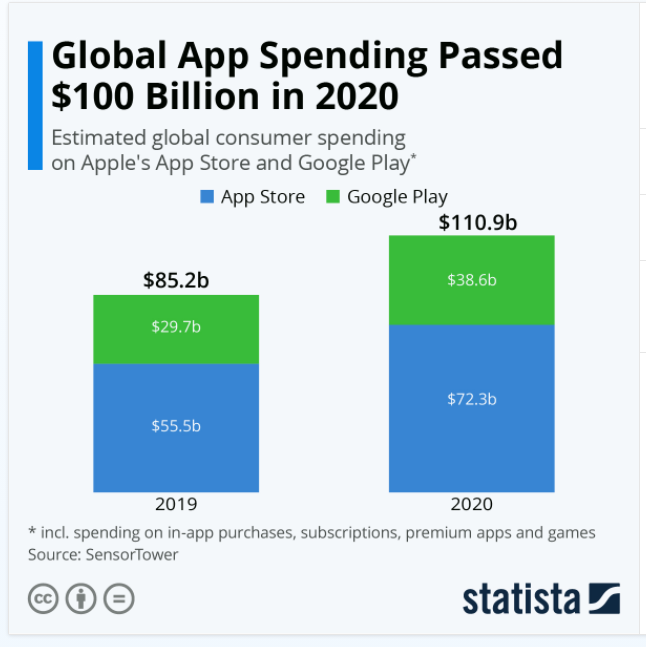

12. Natural market expansion, future sales being pulled forward, or a little of both?

Source: Statista, from 1/8/21

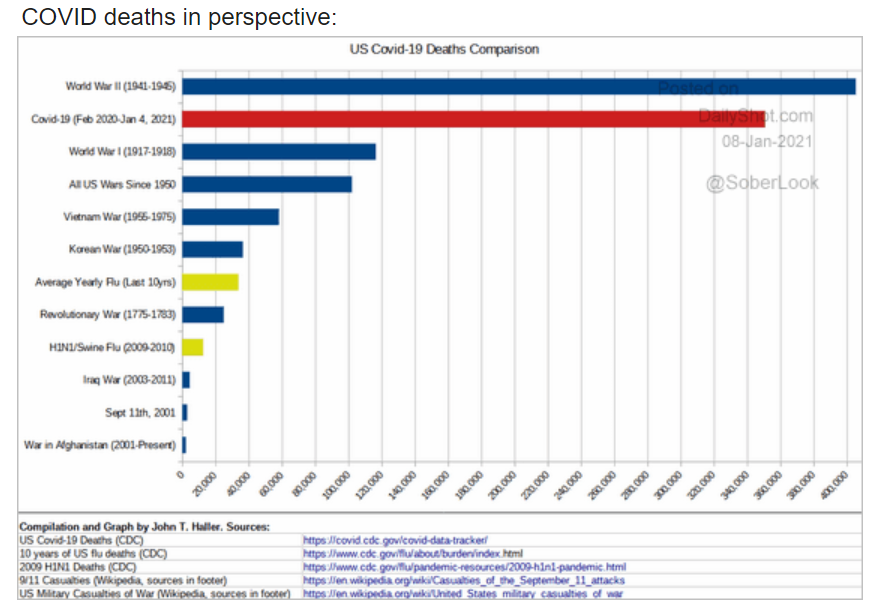

13. We are all exhausted by Covid protection protocol, but we need to remember why:

Source: The Daily Shot, from 1/8/21

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)