SMID Caps Climb, a Look at Risk and Reward in Fixed Income Markets, and Commodities Move Higher

December 21, 2020 | FIRESIDE CHARTS

Small and mid-cap stocks reached new highs last week on the back of progress towards both a stimulus deal and approval of the Moderna vaccine. With both hopes realized, will it be enough to sustain the momentum through the news of a second—more virulent—Covid strain? And as corporate debt issuance hits new highs and yields continue to slump, are fixed income investors being appropriately compensated for the risks they’re taking? Meanwhile, the USD has also continued to sink, which has given a boost to commodities. But is it enough to spark inflation?

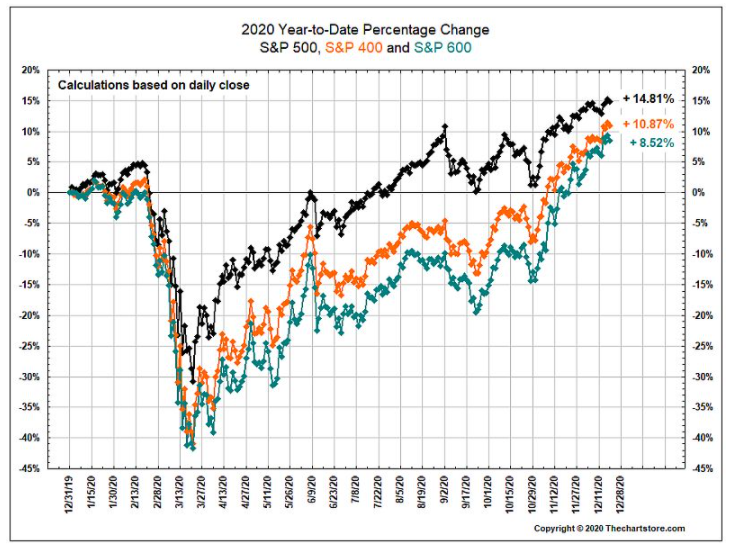

1. The SMID rally continued last week with many new all-time highs, yet the new Covid strain in the U.K. will test the markets resolve this week…

Source: The Chart Store, from 12/21/20

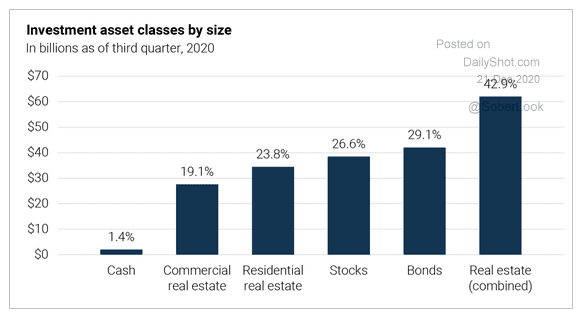

2. While Real Estate only makes up ~3.8% of the S&P 500® Index, it is the largest asset class by far…

Source: The Daily Shot, from 12/21/20

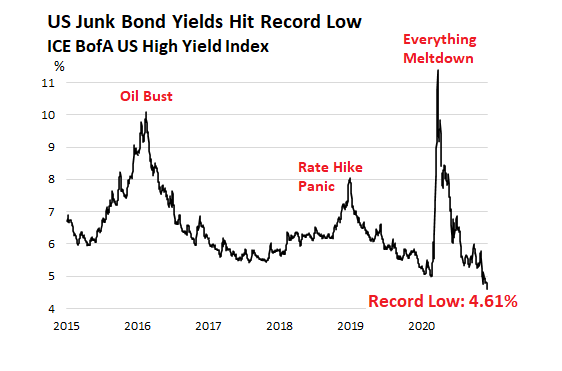

3. The “desperation” for yield has made many ignore the obvious: is a ~3.75% yield enough reward over the 10-year UST to compensate for ten years of credit and inflation risk?

Source: The Daily Shot, from 12/21/20

4. The need to pay down the Covid credit lines plus ultra-low rates has driven corporate debt issuance to new highs…

Source: The Daily Shot, from 12/21/20

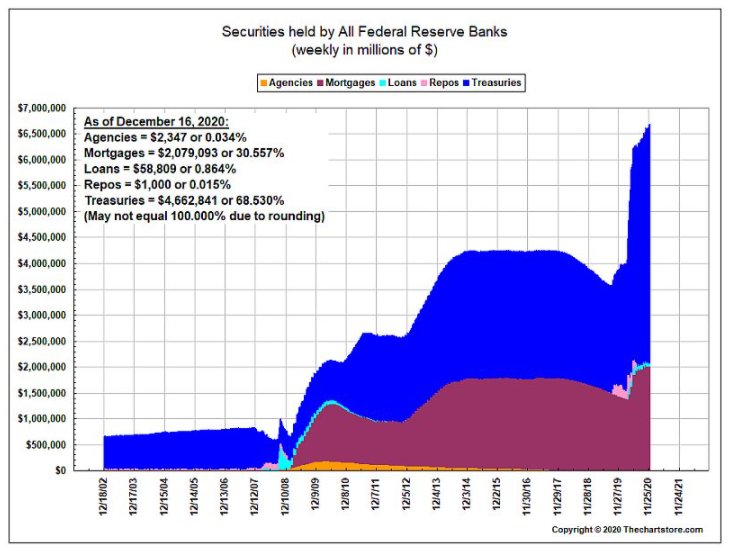

5. The Fed’s latest QE is largely in the longer end of the curve as they seek to “enforce” their near-zero rate policy through 2023…

Source: The Chart Store, from 12/21/20

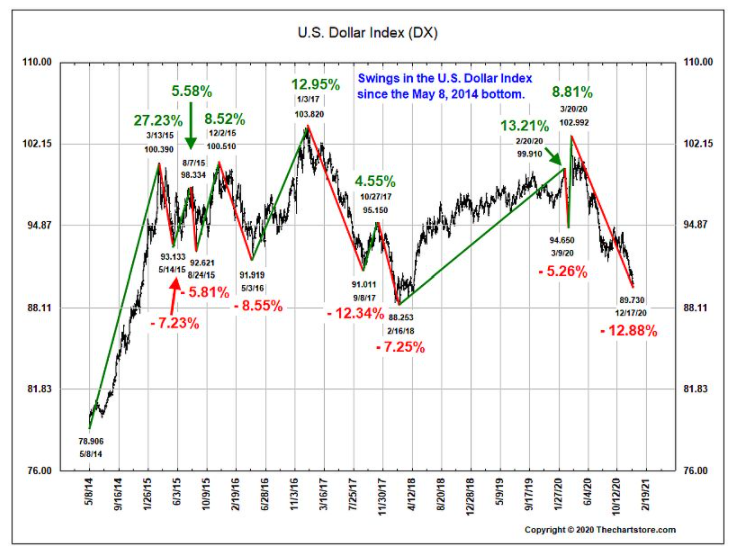

6. The dollar’s decline re-accelerated last week…

Source: The Chart Store, from 12/21/20

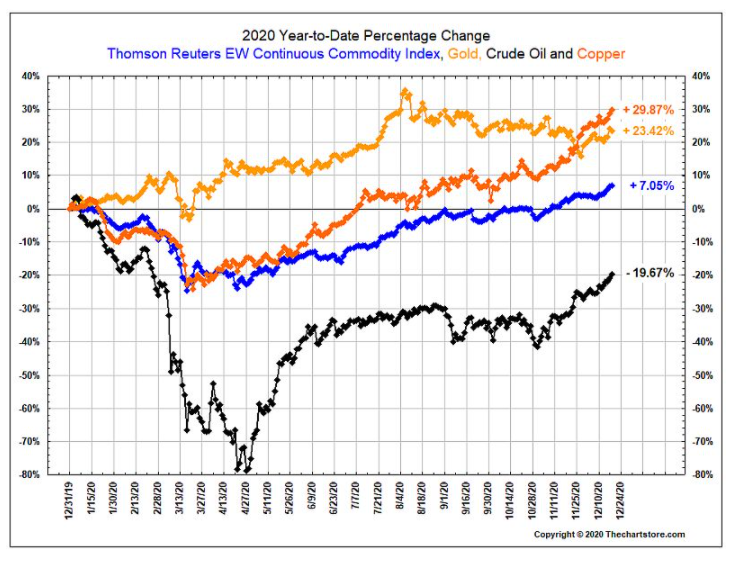

7. A weaker USD is helping give a bid to commodities and Int’l equities…

Source: The Chart Store, from 12/21/20

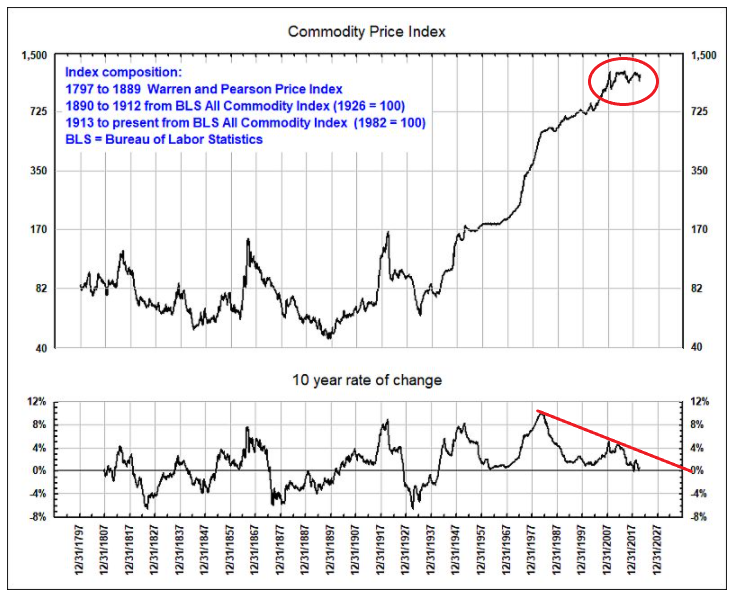

8. Commodity-driven inflation has not been seen in decades and has been flat-to-down since the Great Recession…

Source: The Chart Store, from 12/21/20

9. If you think 2020 is difficult here, try the U.K. where you have to add the BREXIT strife and now this…

Source: The Daily Shot, from 12/21/20

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.