“Stagflationary” Signals, Suppressed Consumer Confidence, and the Bond-Yield Spike

September 29, 2021 | FIRESIDE CHARTS

Manufacturing activity is slowing across the U.S.—including slipping into contraction in the Mid-Atlantic—and paired with climbing prices, it’s sending ominous “stagflationary” signals of what may lie ahead for the economy. Is this part of what’s dragged down consumer confidence and reignited the divergence from equity performance? And what will it take to close the gap, particularly as we head into the holiday season? Meanwhile, as yields climb and the short-term treasury curve inverts, we’re seeing a few select equity sectors benefit even as the broad market struggles. Finally, amid increased tech regulation, a crypto and energy crackdown, and the Evergrande saga, China’s been no stranger to headlines in September. How have their markets reacted and is more fallout yet to come?

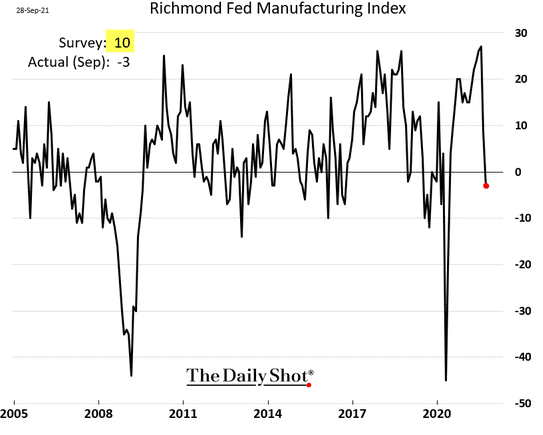

1. The Mid-Atlantic regional manufacturing fell into negative territory last month. Slow growth ahead?

Source: The Daily Shot, from 9/29/21

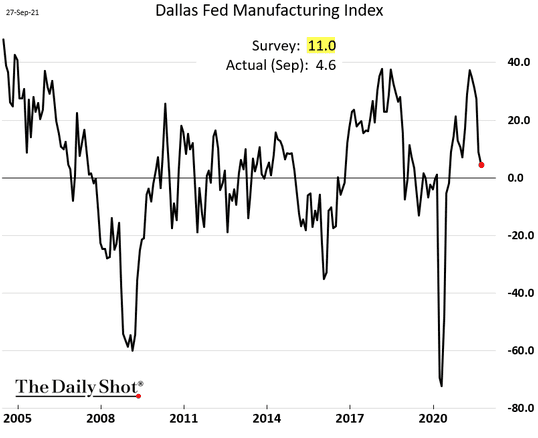

2. The Dallas Fed survey showed a significant slowdown into slow-growth territory:

Source: The Daily Shot, from 9/28/21

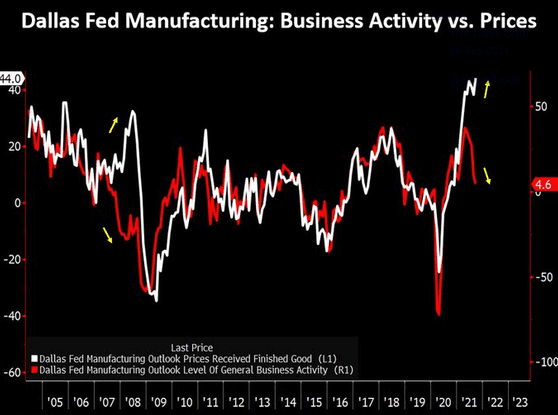

3. Prices are rising and economic activity is slowing. This is the definition of “stagflation”:

Source: The Daily Shot, from 9/28/21

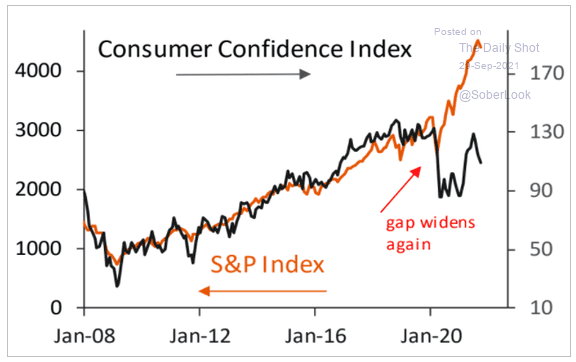

4…While price increases remain robust. Again, Wikipedia defines stagflation as “recession-inflation is a situation in which the inflation rate is high, the economic growth rate slows, and unemployment remains steadily high.”

Source: The Daily Shot, from 9/29/21

5. When and what will cause these “jaws” to snap shut? The consumer makes up ~70% of the U.S. economy…

Source: The Daily Shot, from 9/29/21

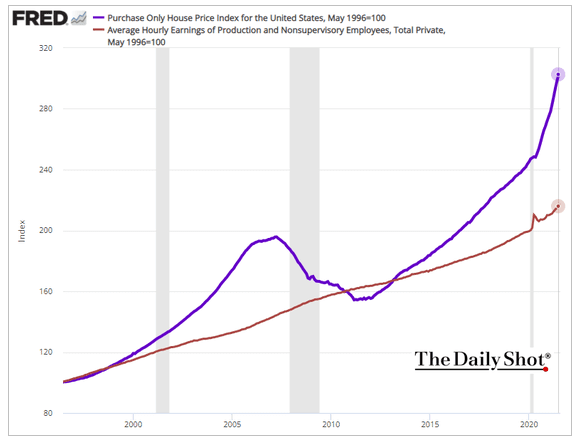

6. The housing price spike may put the housing sector in a more vulnerable position if interest rates rise:

Source: The Daily Shot, from 9/29/21

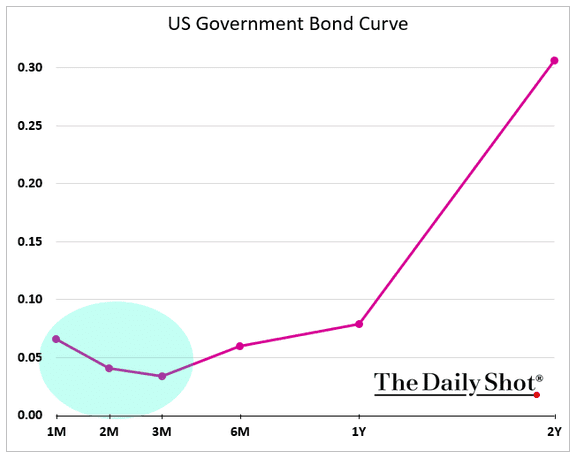

7. As a government shutdown/technical default looms (Senate rejected debt limit and funding increase yesterday as it blocks the $1 trillion+ transportation and $3.5 trillion social bills), short term treasury yields inverted.

Source: The Daily Shot, from 9/29/21

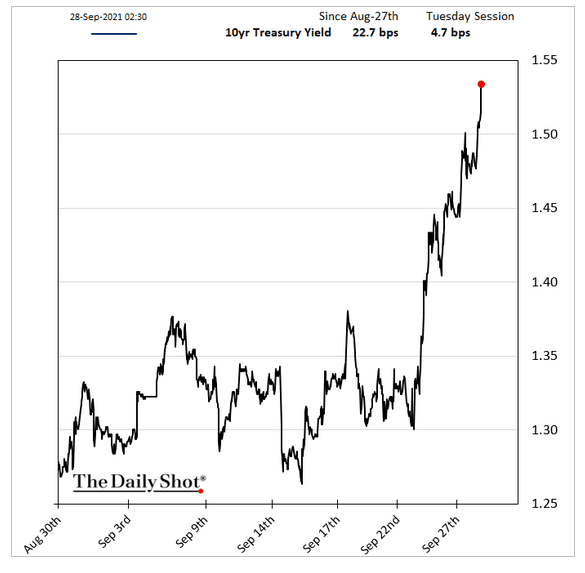

8. This time the Fed’s prompts/warnings/guidance has the markets attention. What would this look like without QE?

Source: The Daily Shot, from 9/28/21

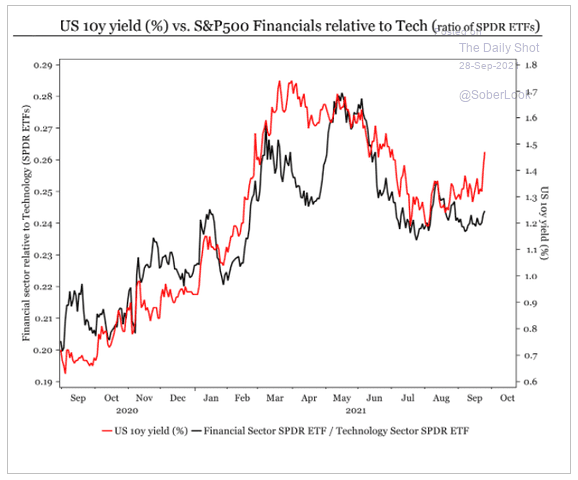

9. Higher yields are benefiting the sectors that historically provide better performance in the face of inflation: Energy, Materials, Financials and small caps.

Source: Longview Economics, from 9/28/21

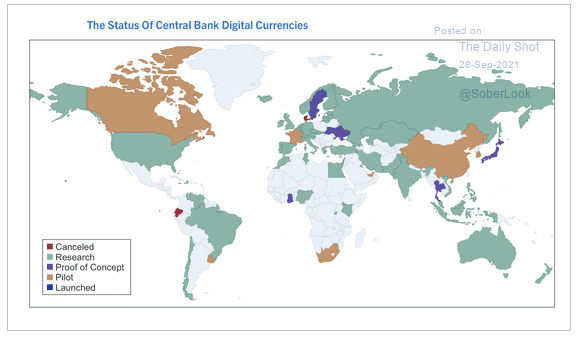

10. Historically, sovereign nations (or a confederacy of nation states) have issued and controlled currencies. China may not be alone in banning crypto as it challenges sovereignty and control, control (economic, political and criminal):

Source: The Daily Shot, from 9/28/21

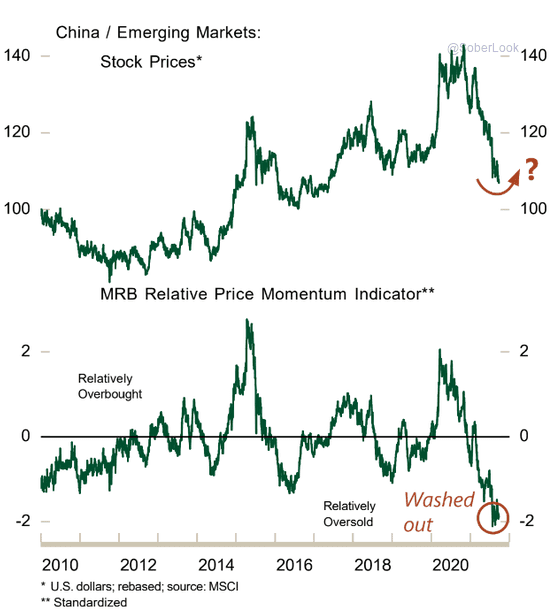

11. Historically, Chinese equities would appear oversold. But the government’s crackdown is not a historical norm…

Source: The Daily Shot, from 9/29/21

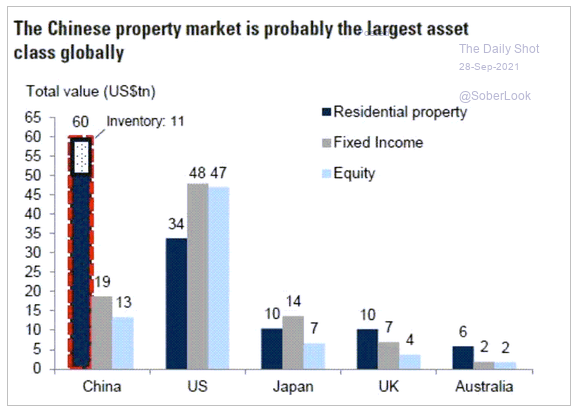

12. As Evergrande, Sunac and others falter, it is important to note the size of the market in question:

Source: Goldman Sachs, from 9/28/21

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.