Insights from the Survey of Household Economics and Decisionmaking

May 26, 2023 | FIRESIDE CHARTS

The Federal Reserve Board recently published the results of their “Survey of Household Economics and Decisionmaking” from October 2022. Periodically released by the Federal Reserve Board, this report offers a comprehensive analysis of critical aspects such as income, savings, debt, housing, education, and retirement. The report is split into eight sections: overall financial well-being, income, employment, expenses, banking and credit, housing, higher education and student loans, and retirement and investments. In lieu of the normal chart blog, today we’re going to highlight charts from each of these sections that we found interesting. The full report can be found on the Federal Reserve’s website.

In the executive summary, the Federal Reserve Board noted that self-reported financial well-being fell sharply and was among the lowest observed since 2016. Consumers are spending more due to rising costs while feeling that their retirement savings are no longer on track due to lower asset prices. The labor market remains a notable bright spot with workers able to exercise more power in the workplace.

1. Overall Financial Well-Being: Inflation is the biggest financial challenge for consumers, who have a negative view of the overall economy despite doing at least okay personally.

2. Income: More adults are seeing their monthly income increase, but higher prices impact everyone and budgets are stretched as a result.

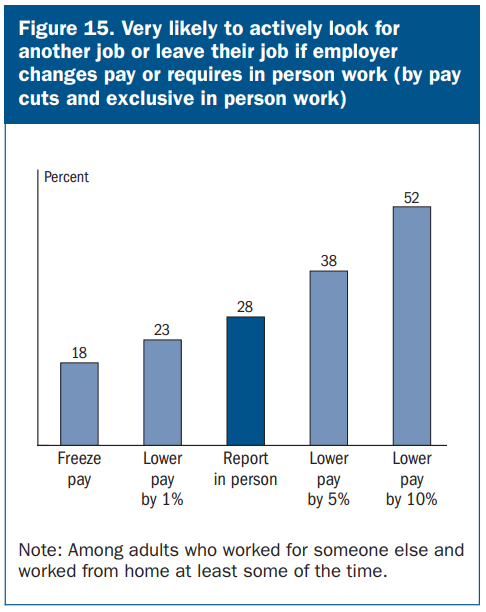

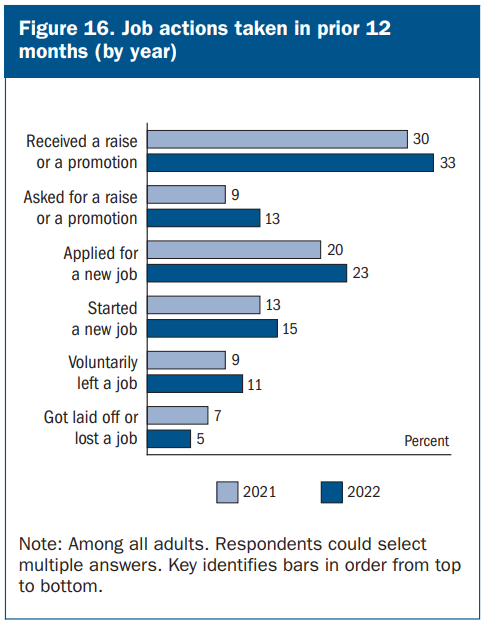

3. Employment: Employees view ending hybrid work arrangements as equivalent to a 2 to 3% pay cut and feel secure enough in their employment prospects to push for the work arrangement they want.

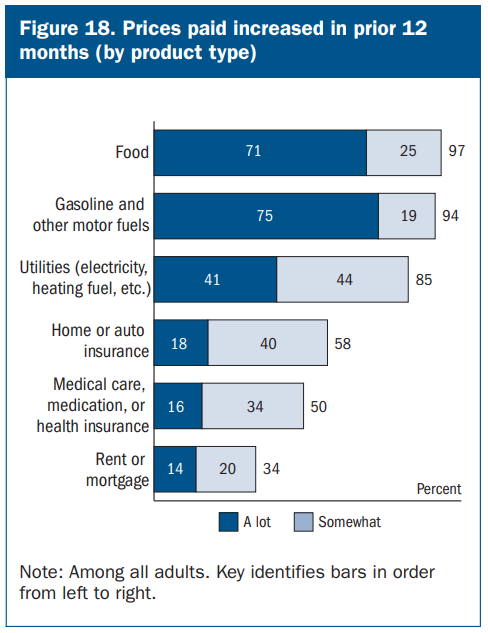

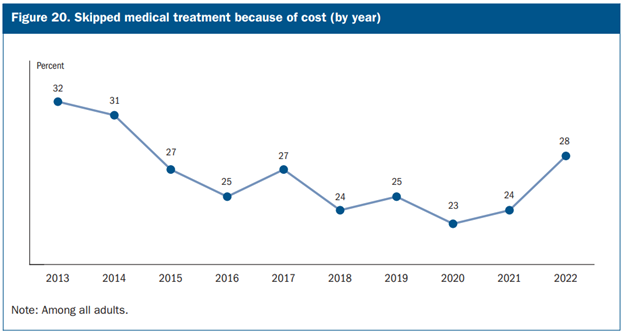

4. Expenses: Consumers are paying a lot more for food and energy and, concerningly, more adults reported skipping medical treatments because of costs.

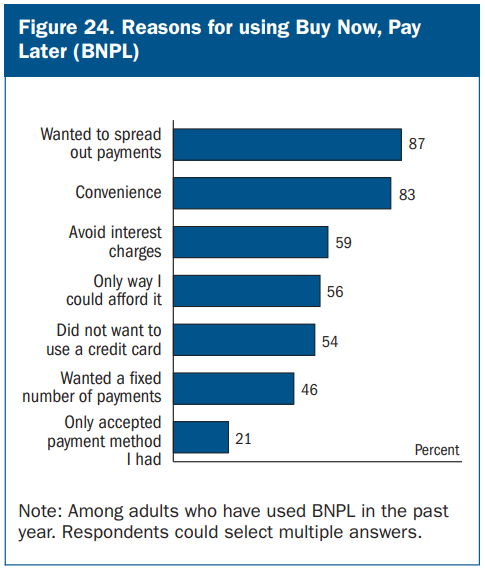

5. Banking and Credit: Consumers like the convenience of Buy Now, Pay Later (BNPL) and are using it in place of a credit card for purchases they couldn’t afford otherwise.

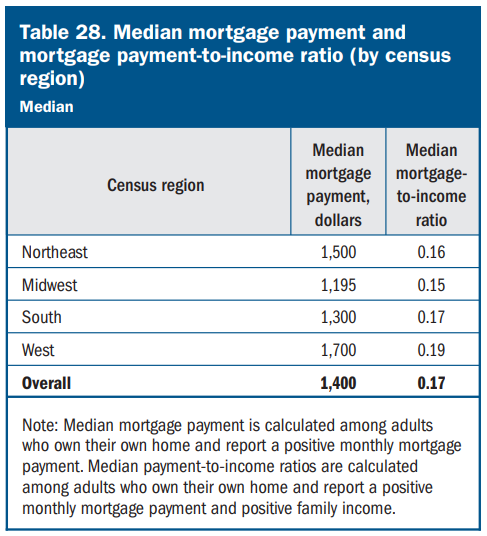

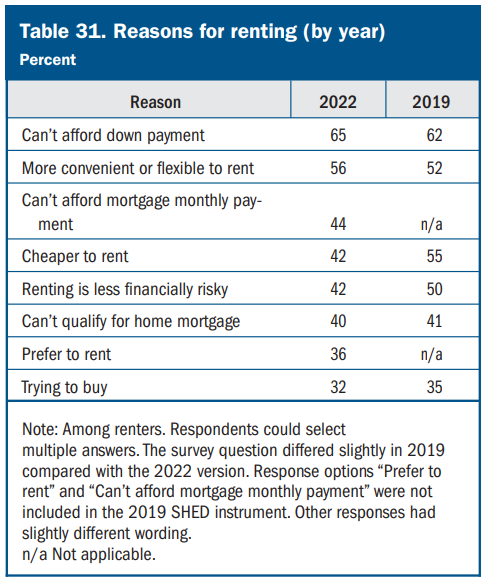

6. Housing: Existing homeowners are locked-in to low monthly payments relative to their incomes, and the top reason for continuing to rent is the inability to afford a down payment.

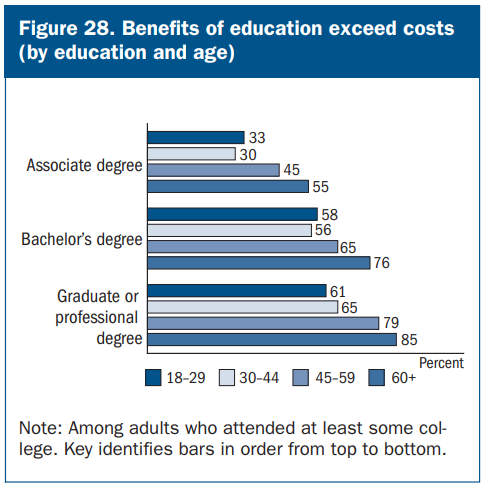

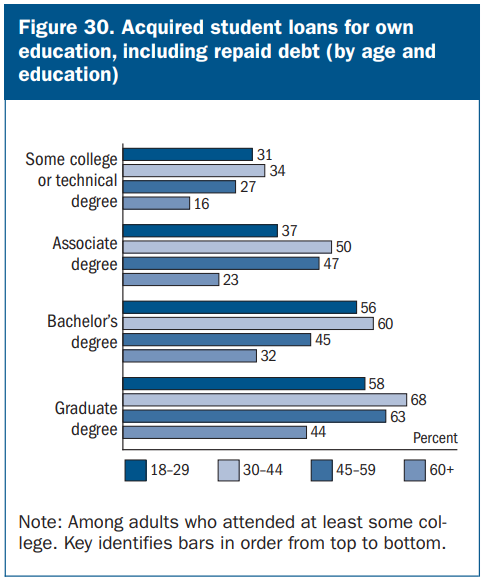

7. Higher Education and Student Loans: Younger generations are less confident that the benefits of higher education will exceed the costs as the median amount of debt among those with outstanding student loans is between $20,000 and $24,999.

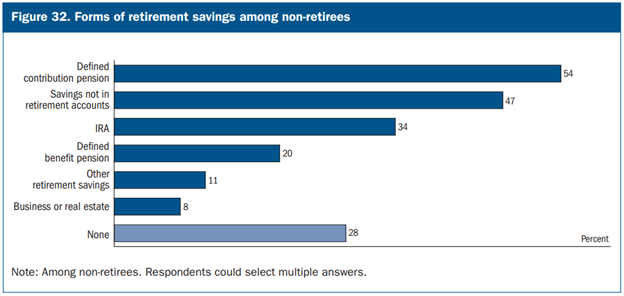

8. Retirement and Investments: Defined contribution plans are the most prevalent method of saving for retirement but nearly a third of adults, mostly between the ages of 18 and 44, don’t have any form of retirement savings.

Source: All Charts and Data from the Federal Reserve Board’s “Economic Well-Being of U.S. Households in 2022” report published in May 2023.

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.