Household Debt Hits Record $14.6 Trillion, Climbing Yields & Inflation Anticipation’s Effect on Equities, and Potential Trend Reversals

February 24, 2021 | FIRESIDE CHARTS

Personal savings may have reached new heights in 2020, but the pandemic-era housing boom ensured household debt wasn’t far behind; totals hit a record high of $14.6 trillion near the close of the year as mortgage debt surpassed $10 trillion for the first time. And retail sales surprised with 5.3% growth in January, but a breakout by type paints a more nuanced picture in an illustration of the “Covid Factor’s” ongoing influence. Meanwhile, climbing Treasury yields and inflation expectations continue to influence the equity markets, sparking losses yesterday—and the hashtag #buythedip to trend on Twitter. Fed Chair Jerome Powell’s testimony helped calm the waters though, sparking a late-session rally that brought the Dow and S&P 500® Index to end the day in the green. And is change in leadership in the cards as momentum and growth stocks ease off the gas and small caps continue to outperform?

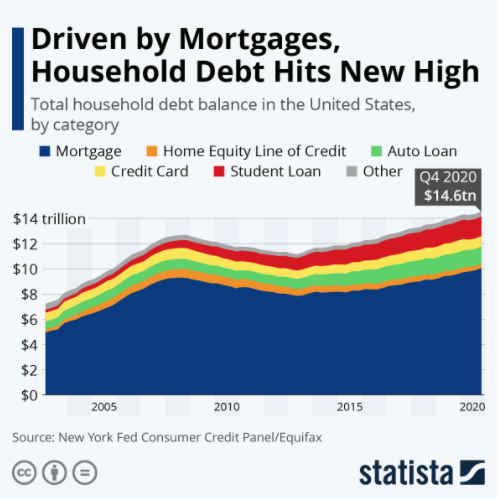

1. Before we all get too complacent, compare current levels to 2007…

Source: Statista, from 2/23/21

2. A powerful display of the “Covid factor’s” effect on the retail economy.

Source: The Daily Shot, from 2/23/21

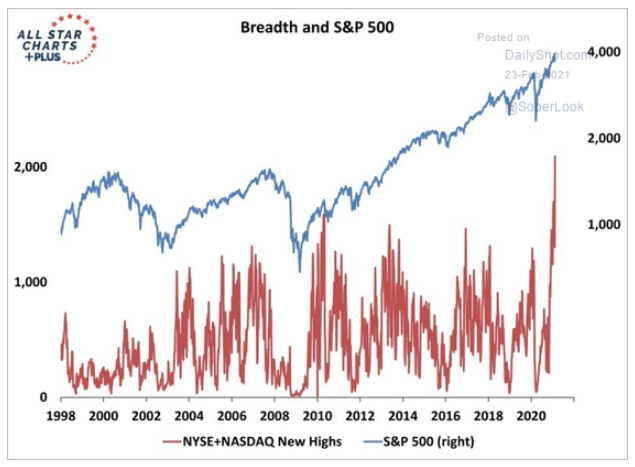

3. The markets, and the momentum issues in particular, are taking a well-earned respite. Or are we in the beginning of a leadership change?

Source: The Daily Shot, from 2/23/21

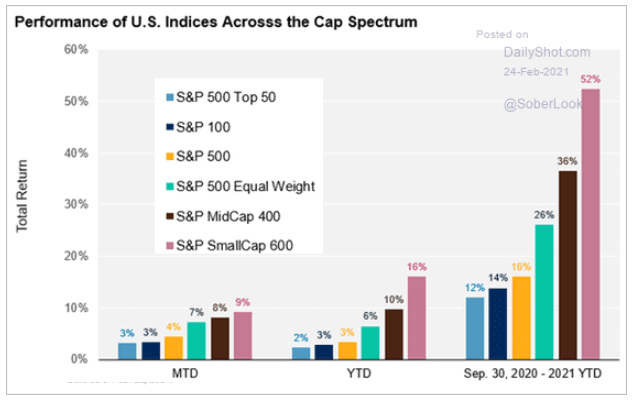

4. After years of large-cap leadership, smaller sized companies have been leading the charge for the past 4+ months:

Source: Dow Jones Indices, as of 2/22/21

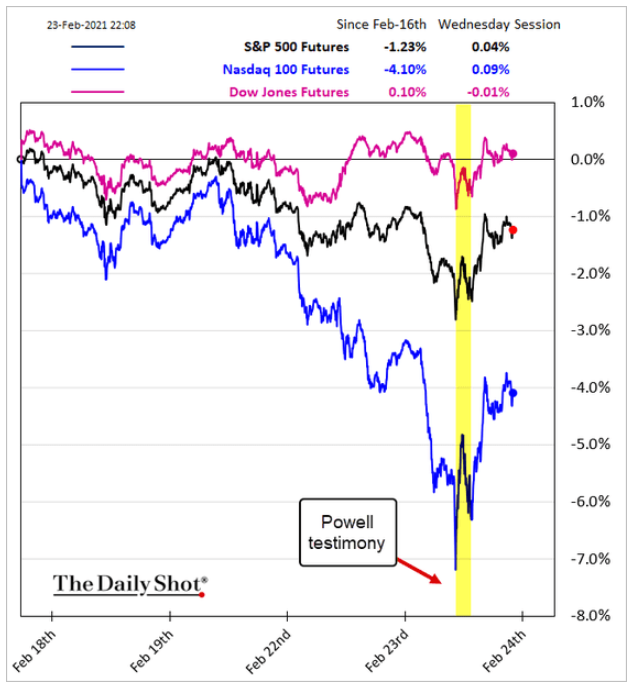

5. Fed Chair Powell confirmed the Fed’s policies will continue as previously outlined…no reduction in QE and near-zero policy rates through 2023. Markets, spooked by inflation worries, rallied…

Source: The Daily Shot, from 2/24/21

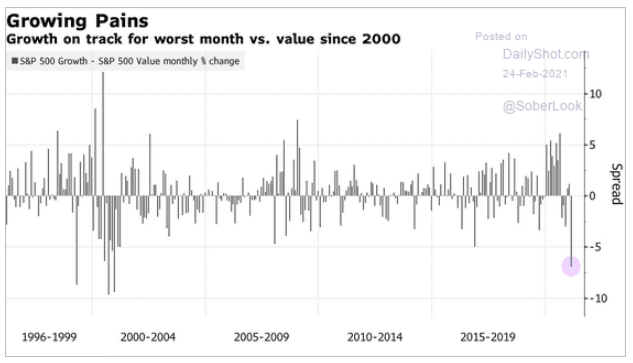

6. The same inflation worries have given growth stocks a “bloody nose”. We are watching for trend reversals versus a well-deserved respite. Nothing can go straight up indefinitely!

Source: Bloomberg, from 2/24/21

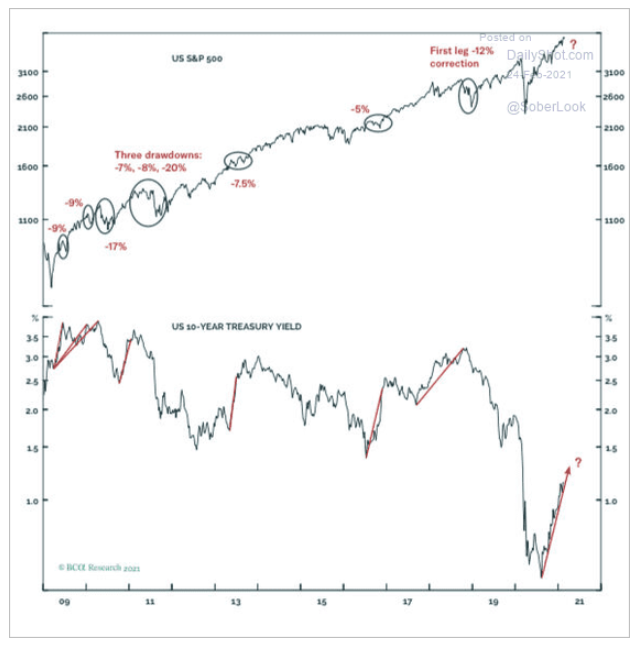

7. During the last decade, rising interest rates have mattered to stock prices/valuations. Yet due to the near-zero starting point, will this increase have a muted effect until they reach the 1.5% range?

Source: The Daily Shot, from 2/24/21

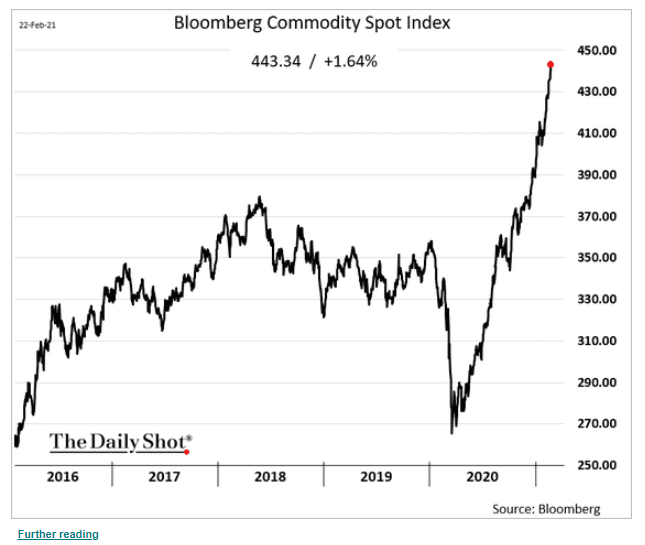

8. A quiet but definitive build in momentum. Part value, part currency, part inflation hedge, part economic recovery. It bodes well for resource-rich emerging market economies…

Source: Bloomberg, from 2/23/21

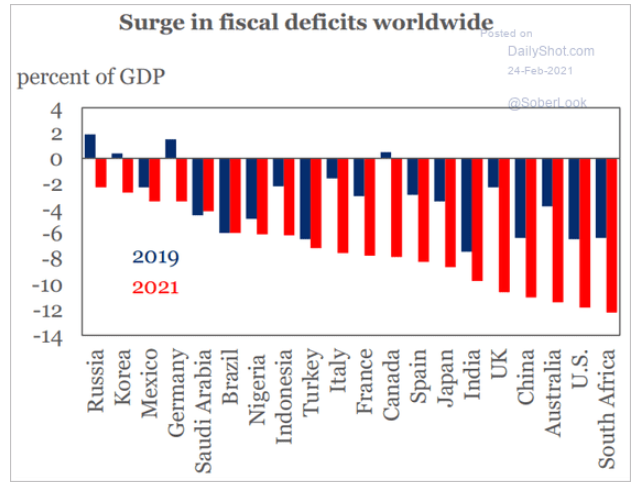

9. A reminder that all this deficit spending has to be paid back, defaulted on, or reduced through currency devaluation.

Source: The Daily Shot, from 2/24/21

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.