From the Desk of the PM – Update on Market Selloff and and Coronavirus Fears

February 27, 2020 | TIMELY PM UPDATES

With the sudden drop in the global equity markets, we thought it might be helpful to remind everyone about where we have been, where we are now, and share some helpful source information.

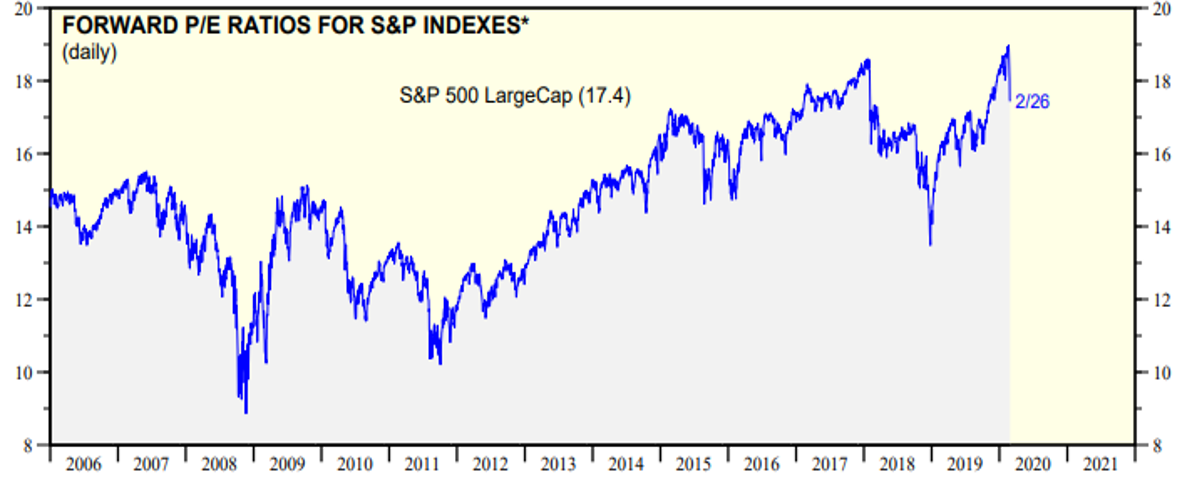

Before we discuss the virus, let’s go back and remind everyone that U.S. large cap stocks, after demonstrating a decade of leadership, may have gotten ahead of themselves from a valuation standpoint. As the chart below from Ed Yardeni Research shows, the forward P/E of the S&P 500 reached 19X—which is a level not seen since the Dot.com bubble in the late 1990’s—and, depending on the timeframe, about 1-5 times higher than historical averages. As of yesterday, the S&P 500’s forward P/E has pulled back to 17.4X as of close on 2/26/2020. So the market was likely due for a rest; we just did not know the catalyst.

Source: Yardeni Research, Inc., from 2/26/2020

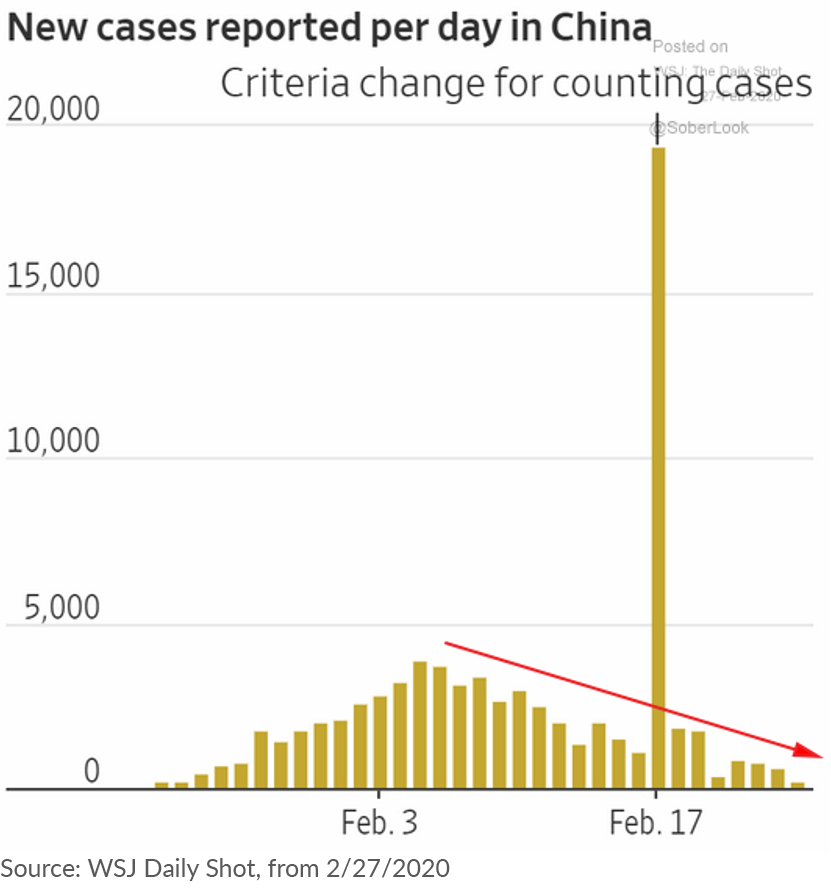

The current coronavirus, named COVID-19, has certainly provided the catalyst. We caution our readers and investors from succumbing to fear based on the press—whose job is to entertain—and, as a result, often foment fear and greed. If you would like facts, we urge you to go to the Center for Disease Control’s (CDC) website or to the World Health Organization’s (WHO) website to obtain as much factual information as possible. The WHO publishes a daily situation report on the number of cases and their locations. Most readers are aware that China was the epicenter and by far the country that has been most affected so far. As of 2/26, there were 78,191 confirmed cases, many of whom have fully recovered. We hear about the 2,718 deaths, but not the 96.5% who have survived. One has to give the Chinese government kudos for the quarantine actions that have affected tens of millions of Chinese citizens. As the next chart shows, the number of new daily cases has been declining steadily and China appears to have the situation under control at this time.

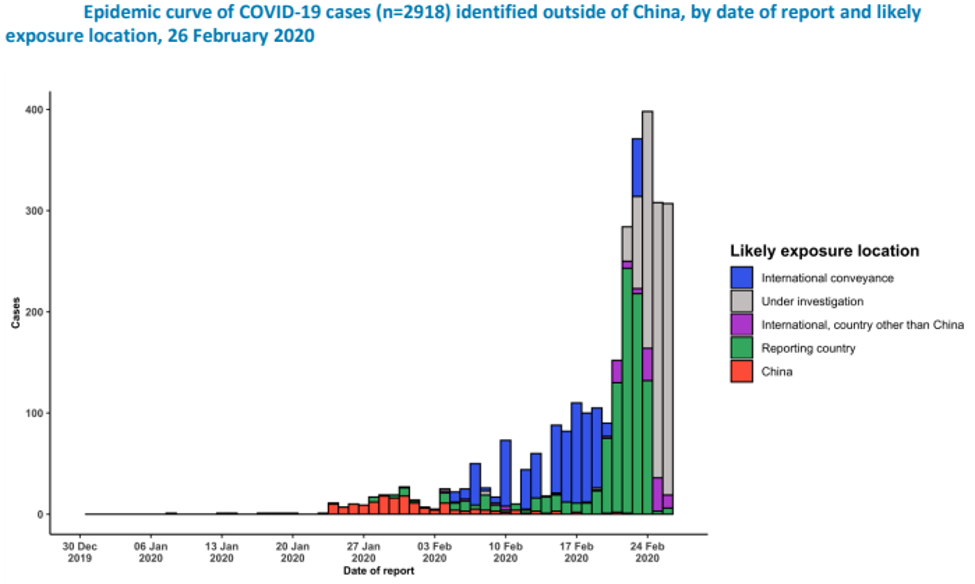

What seems to have spooked the global markets so is the spread of the disease outside China. As of the 26th, there are now 2,918 total cases outside China, resulting in 44 fatalities. COVID-19 has now spread to 37 countries, with particular outbreaks in Italy (322 cases and ~10 villages under quarantine), Japan (164 cases and new quarantine measures announced today), and Iran (95 cases). The unfortunate people stuck on the Diamond Princess cruise ship anchored in Japanese waters account for another 691 cases. Closer to home, there are 53 confirmed cases in the United States, 10 in Canada and none in Mexico. Here is what it looks like graphically: (Note the dark blue is all from the cruise ship)

Source: World Health Organization Situation Report-37, 2/26/2020.

What is clear is COVID-19 is not going to be a quick, transient event like many had hoped. It is unrealistic to think that tens of millions of workers can be quarantined in the world’s second largest economy, for a month or longer, without an effect on the global supply chain and economy. Earnings warnings have already been shared. Certain industries such as the airlines will suffer. Demand for oil and raw materials will take time to recover. Small businesses in effected regions generally do not have a lot of cash on hand. Their fixed costs remain but their income is muted at best. Manufacturing will have disruptions and trade may be subdued… for a while.

So far, China’s central bank (PBoC) and the Hong Kong government have taken steps to aid their economies. Various rate cuts and stimulus packages are already in the works. The CDC and WHO are working to alert and prepare the healthcare systems across the globe. Now that we know what we are dealing with, which China did not in the early weeks of the outbreak, we can prepare and deal with it accordingly. Will COVID-19 spread? Probably. Is it worth the level of fear and panic currently present in the markets? Probably not.

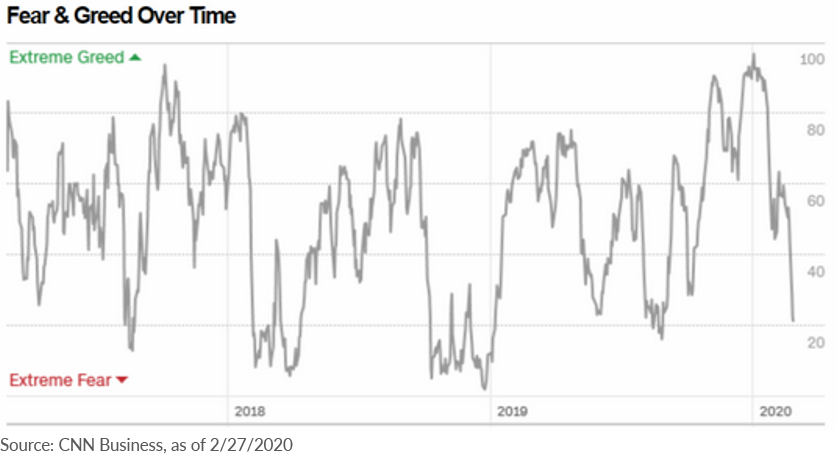

At the risk of breaking our own advice, the following is CNN’s Fear and Greed Index over time. We started the year with a reading of extreme greed; 6 weeks later we are approaching maximum fear.

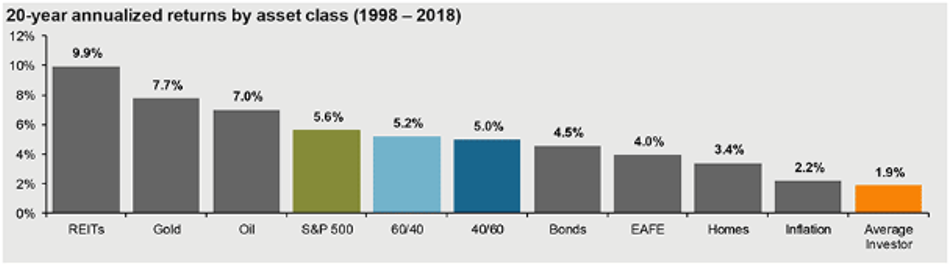

At BCM we designed our management systems to remove emotion from the investment process. The main reason is that emotions lead to poor decisions at the investor level. As the chart below outlines, over the last 20 years, the average investor has underperformed all major asset classes as they sell low and buy high throughout the market cycles.

Source: J.P. Morgan Asset Management Guide to the Markets – U.S., data as of 1/31/2020

Indices used are as follows: REITS: NAREIT Equity REIT Index, EAFE: MSCI EAFE, Oil: WTI Index, Bonds: Bloomberg Barclays U.S. Aggregate Index, Homes: median sales price of existing single-family homes, Gold: USD/troy oz., Inflation: CPI, 60/40; A balanced portfolio with 60% invested in S&P 500 Index and 40% invested in high-quality U.S. fixed income, represented by the Bloomberg Barclays U.S. Aggregate Index. The portfolio is rebalanced annually. Average asset allocation investor return is based on an analysis by Dalbar Inc., which utilized the net of aggregate mutual fund sales, redemptions and exchanges each month as a measure of investor behavior. Returns are annualized (and total return where applicable) and represent the 20-year period ending 12/31/18 to match Dalbar’s most recent analysis.

This having been said, we stand by, ready to act, should the markets continue to deteriorate. Our systems are showing signs of shifting to a more conservative posture, but we do not want to jump the gun and invite whipsaw. We will follow our rules and make changes as the systems dictate. Our growth strategies do not try to avoid all losses, but rather large losses. The declines have been swift and certainly made the headlines, but as of close on 2/26/2020, the S&P 500 was down about 3.3% YTD with a drawdown from its all time high of ~7.9%; the MSCI world index was down ~4% YTD with a 7.2% drawdown, and the MSCI World ex-U.S. index was down ~5.2% YTD with a total drawdown of ~8.5%. None of these indices are in a correction let alone a bear market… yet.

As always, we thank you for your business and support. Please reach out to your BCM regional or internal consultant if you have any questions or concerns. Please know we are here, ready and willing to act, as necessary, to try to avoid a large bear market loss.

Sincerely,

David M. Haviland I Managing Partner & Portfolio Manager

salessupport@investBCM.com I Phone 888.777.0535

For a PDF version of this communication, click below:

Sources and Disclosures: