U.S. PPI Drops in September, Fed Intervention Kicks into High Gear, and LEI Index Sparks Some Hope

October 14, 2019 | FIRESIDE CHARTS

Happy Monday Fireside Charts readers! Today may be a holiday, but that doesn’t mean it’ll be a leisurely week in the markets as earnings season kicks off tomorrow! Banks are up first and we’ll be keeping an eye on how they performed in this historically low interest rate environment. Producer price inflation appears weak in the U.S.—despite a strong showing from the construction sphere—as PPI for final demand goods has dropped nearly a full percentage point since July, and a 0.2% drop in PPI for final demand services has nearly erased its surprise August gain. It’s not all bad news however, as the LEIs Index appears to be maintaining positive momentum and isn’t yet mirroring behavior seen in previous recessions. Could this be a sign that Fed intervention is having its desired effect? Easing operations have totaled $180.2 billion in just four weeks, and an announcement came Friday that they will continue at least through the start of 2020. Could that be a talking point at this week’s annual gathering of the IMF in D.C.?

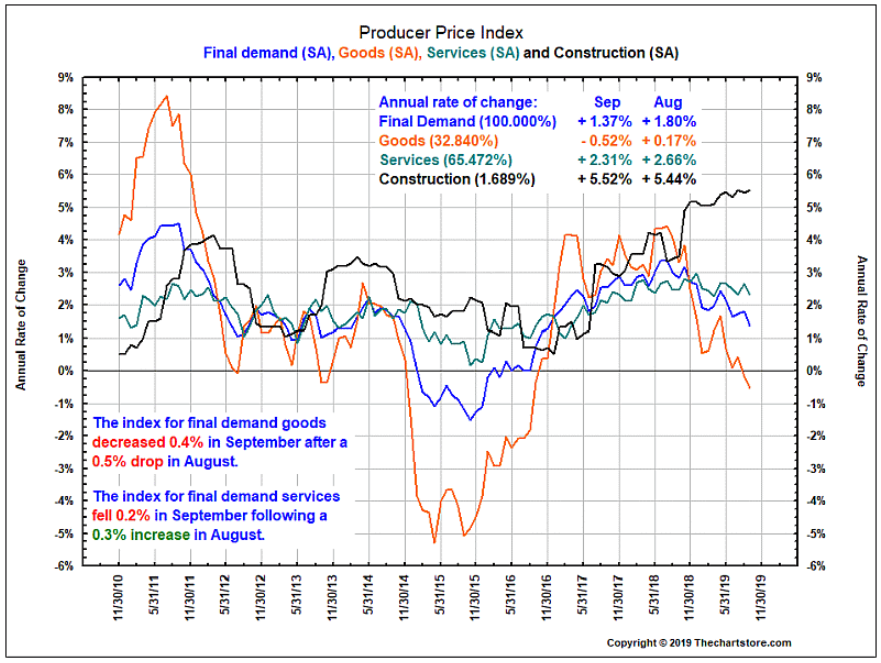

1. As the construction industry heats up, the rest of the economy continues to cool off…

Source: The Chart Store, as of 10/11/19

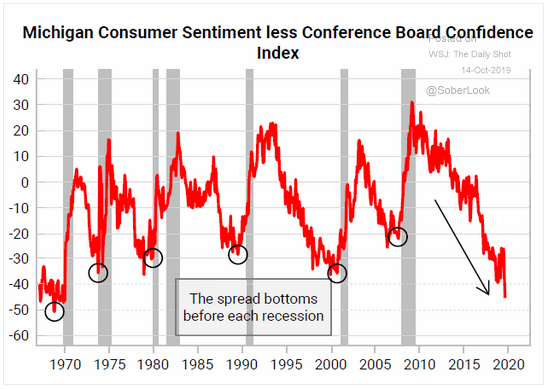

2. Yet another seemingly telling indicator?

Source: Variant Perception, as of 10/14/19

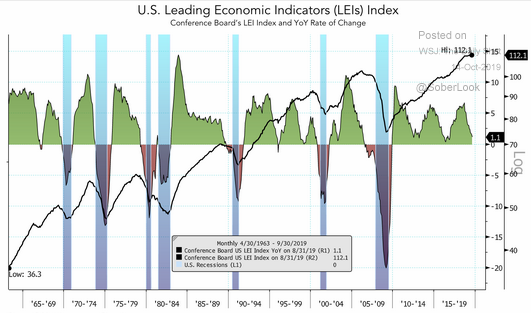

3. For every negative there is a positive…here the U.S. LEIs are shown still in positive territory…

Source: Merk Investments, as of 9/30/19

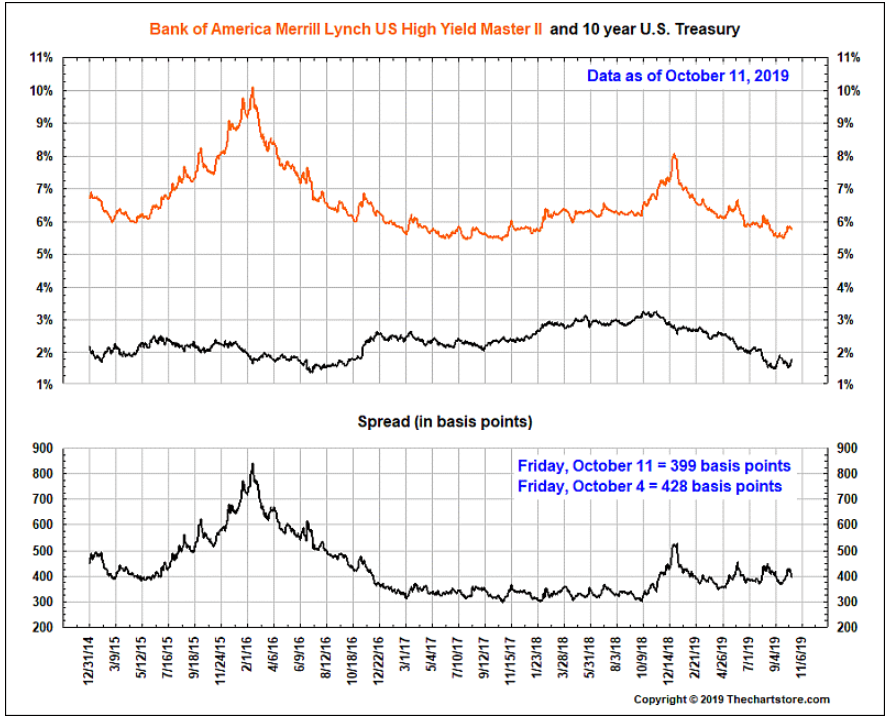

4. High yield (junk) bonds are still signaling an “all-clear”…

Source: The Chart Store, as of 10/11/19

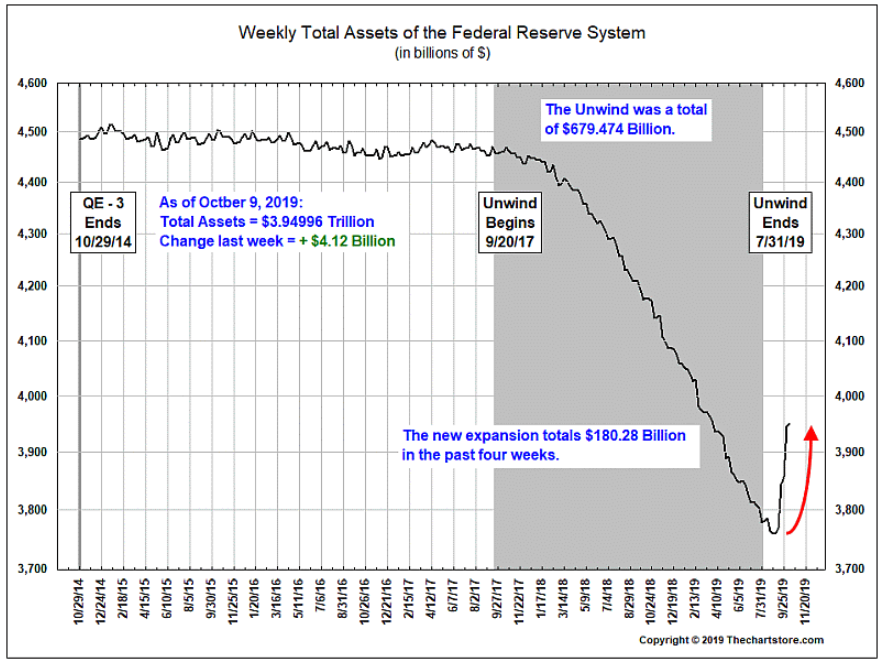

5. Is the Fed launching an unofficial QE program?

Source: The Chart Store, as of 10/11/19

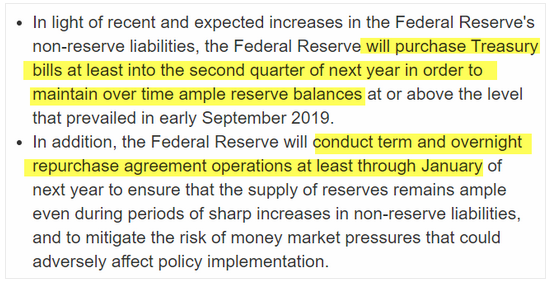

6. Indeed they are…

Source: The Federal Reserve, as of 10/11/19

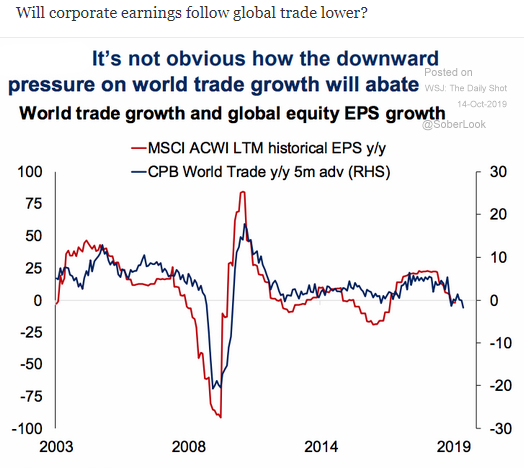

7. A darn good question!

Source: Oxford Economics, as of 10/14/19

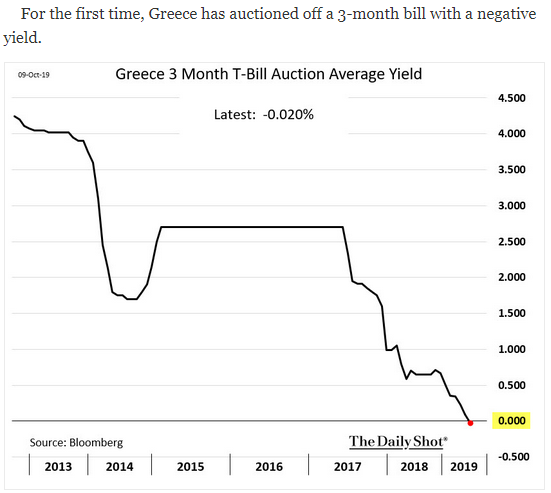

8. Would you pay the Government of Greece to hold your money, even for three months?

Source: WSJ Daily Shot, as of 10/14/19

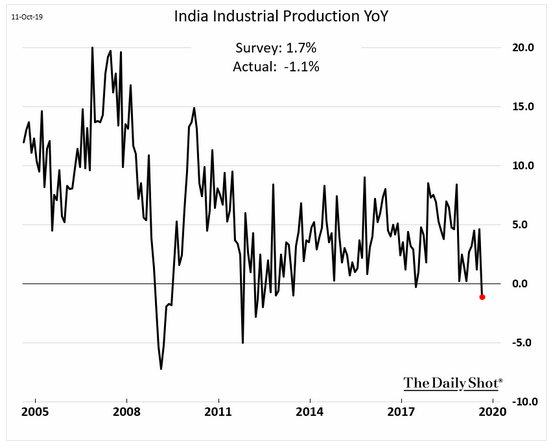

9. “Another one bites the dust”…

Source: WSJ Daily Shot, as of 10/14/19

10. Worth a smile…

Source: WSJ Daily Shot, as of 10/14/19

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.