Yield Curves Flatten, Household Equity Allocations Soar Higher, and Potential Trend Reversals

June 21, 2021 | FIRESIDE CHARTS

The newly hawkish tone from the Fed sent yield curves flatting last week as they continue working to keep rates low… and the effect wasn’t limited to the U.S. Will additional insight be offered when Chairman Powell heads to Capitol Hill tomorrow to discuss the economic recovery? Renewed fears around inflation and rate hikes meanwhile helped push the major indices to close lower Friday and the Dow to have its worst week since October—surely a pain point for many as household equity allocations in the U.S. remain at record highs. Commodities also hit the pause button after this year’s furious rally—is a true trend reversal in the cards or is it just a temporary downshift? All of this, in addition to a still-climbing PPI, is pushing the USD higher. Is it the start of a true rally or just a reactionary head fake?

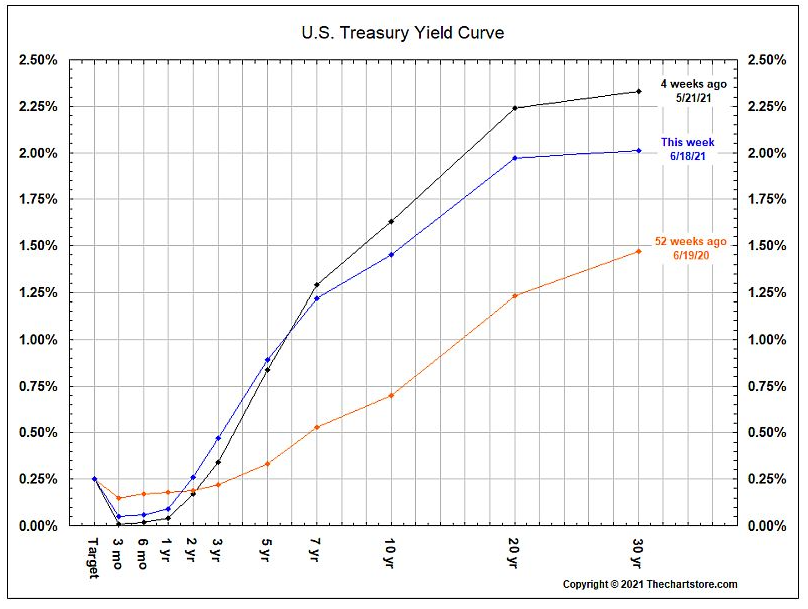

1. Hawkish Fed speak gave all the markets something to digest. Bonds did the expected in the 1-3 year range, yields rose; but the long end of the curve saw yields decline significantly:

Source: The Chart Store, from 6/21/21

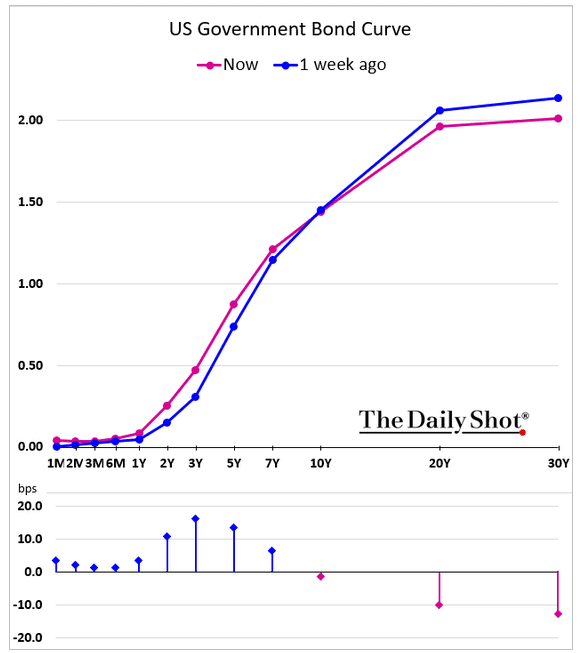

2. Was Thursday and Friday a bit of an over-reaction? Bond curves are flattening across the globe.

Source: The Daily Shot, from 6/21/21

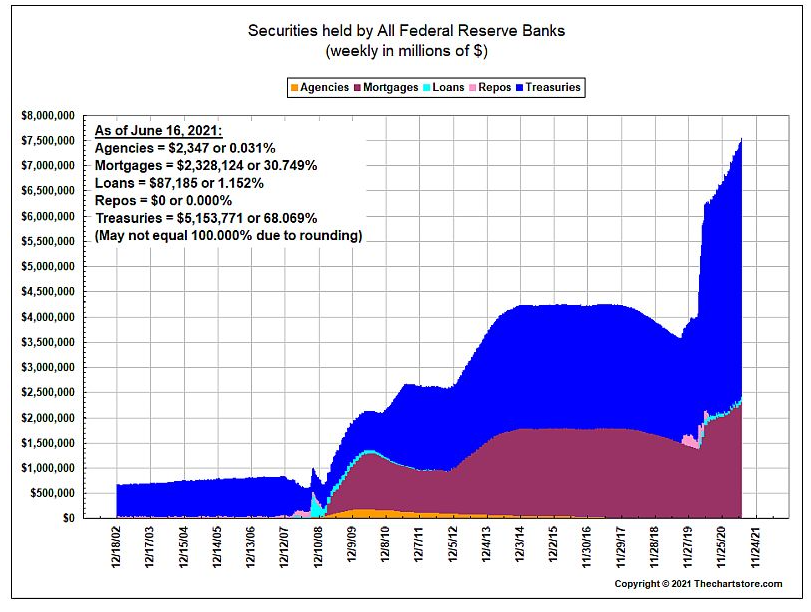

3. As suspected, the Fed was buying in the open market last week to keep rates low:

Source: The Chart Store, from 6/21/21

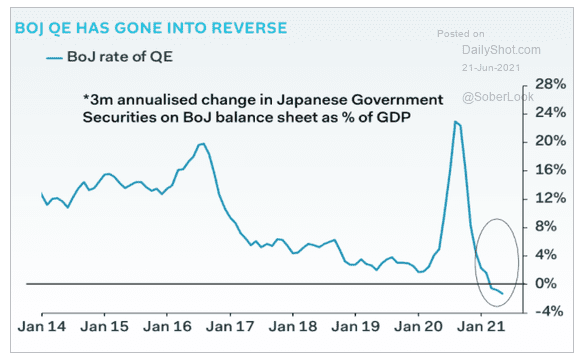

4. Other central banks are or are preparing to reverse QE as well:

Source: The Daily Shot, from 6/21/21

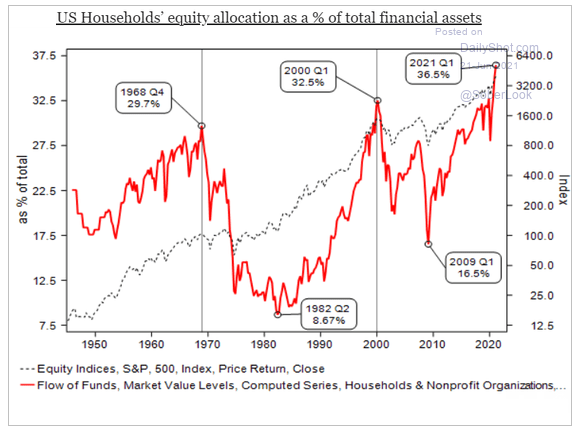

5. Since the “heard” is all in, is it time to seek the sideline?

Source: Longview Economics/ Macrobond, from 6/21/21

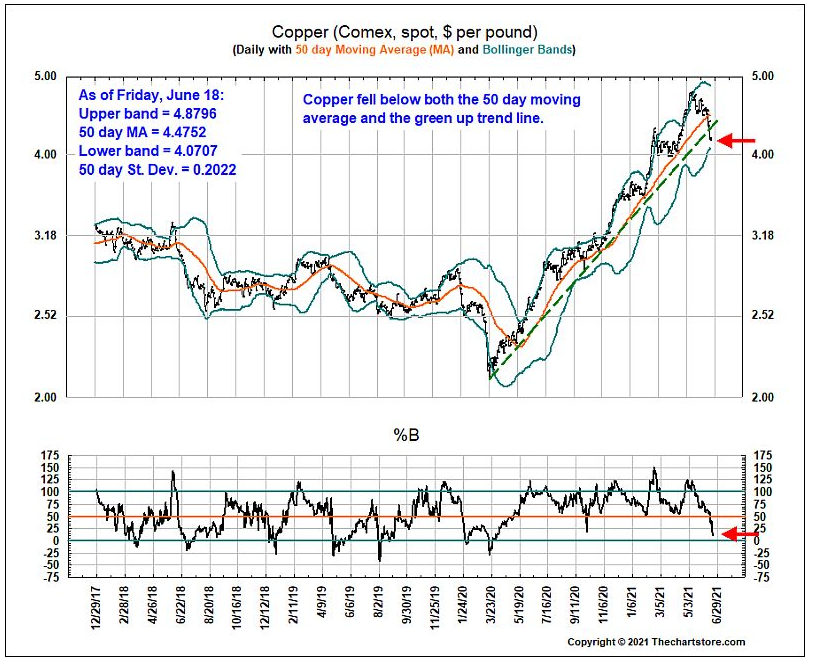

6. “Dr. Copper” along with most commodities also pulled back. Is the rally over or just in a pause?

Source: The Chart Store, from 6/21/21

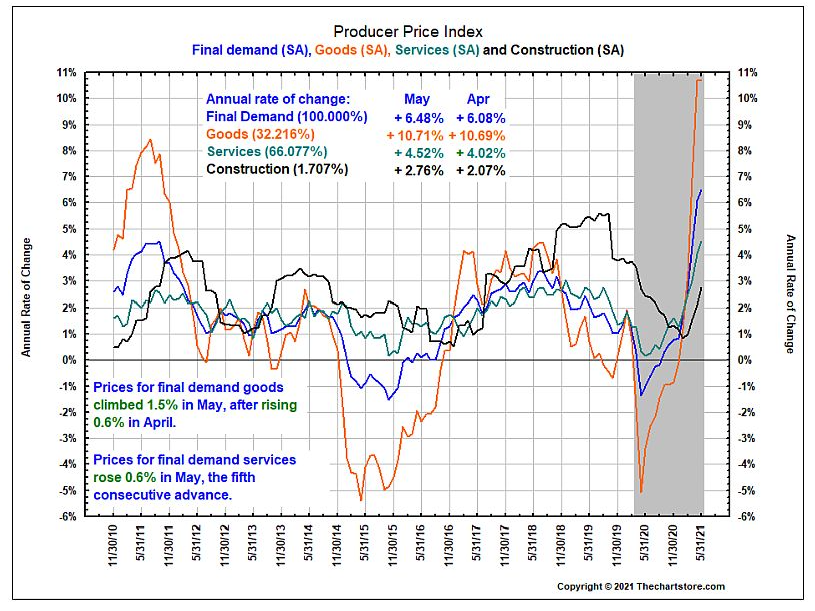

7. An intermediate-term look at PPI and it’s components:

Source: The Chart Store, from 6/21/21

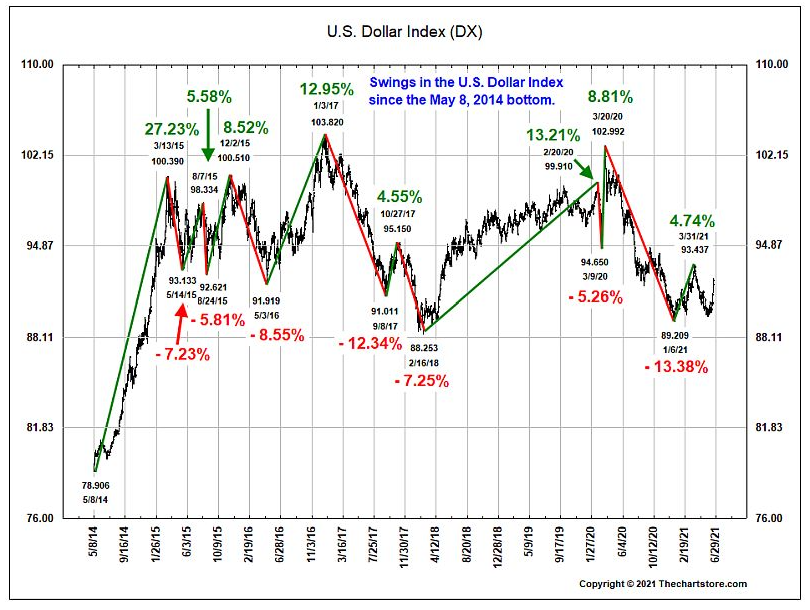

8. All the talk about inflation and higher rates put a bid under the USD:

Source: The Chart Store, from 6/21/21

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)