Manufacturing Hits 15-Year High, the Aftermath of Near-Zero Interest Rates, and Checking in on China’s Recovery

March 3, 2021 | FIRESIDE CHARTS

The manufacturing resurgence continued in February as the sector climbed to a 15-year high, and phenomenon isn’t just limited to the U.S. Climbing costs though could ultimately put pressure on margins and/or make their way through consumers and add yet another inflationary pressure. Meanwhile, with such a massive—and growing—divergence between tax revenue and spending, it stings to see the percentage of stimulus funds being directed toward investments and savings over their intended purpose. Is a lower income cap the answer? Yields jumped yet again this week, prompting a response from equities, but how have stocks typically performed in the long-term following a yield spike? And should we expect the same this time around or will context have something to say on the matter? 2020’s near-zero interest rates have more than one consequence after all… Over in China, manufacturing has lost some momentum and the renminbi impressive appreciation has continued; how will these developments affect the future of their economic recovery?

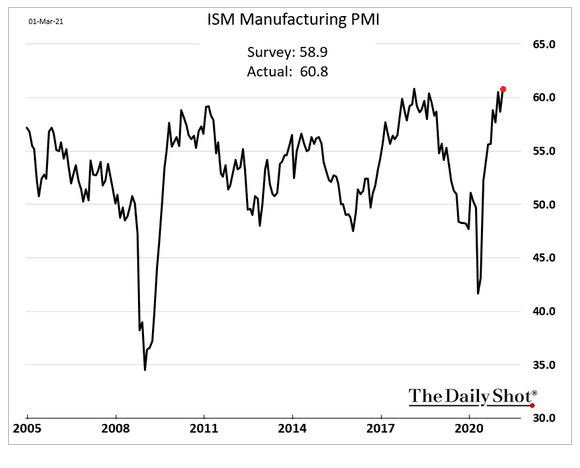

1. The manufacturing sector, ~11.4% of total GDP, is at a 15-year high:

Source: The Daily Shot, from 3/2/21

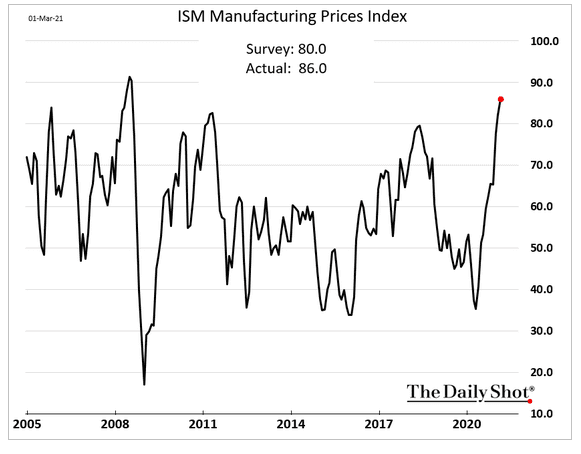

2. Commodity price increases are certainly affecting manufacturer’s cost of goods sold; will these costs get passed through to consumers, lessen profits, or a little of both?

Source: The Daily Shot, from 3/2/21

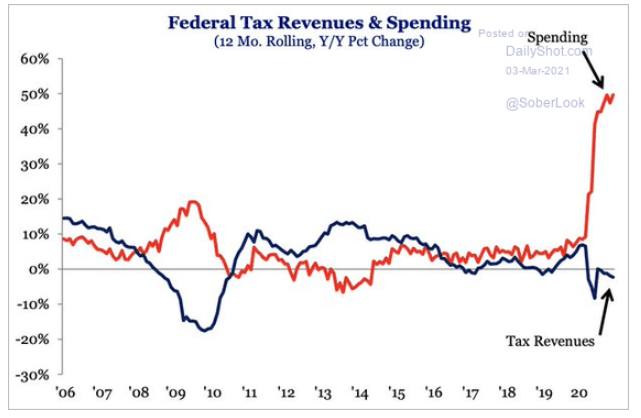

3. The “joy” of receiving free money is going to be replaced by the “pain” of paying it back with higher taxes…

Source: The Daily Shot, from 3/3/21

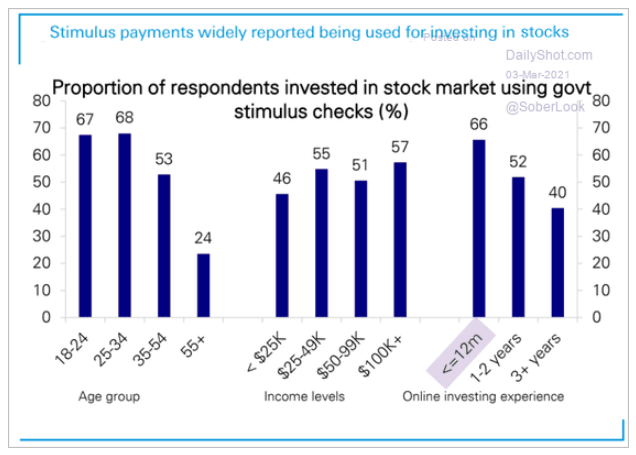

4. More evidence that the stimulus packages are missing their intended mark. Washington, please focus on those truly in need!

Source: The Daily Shot, from 3/3/21

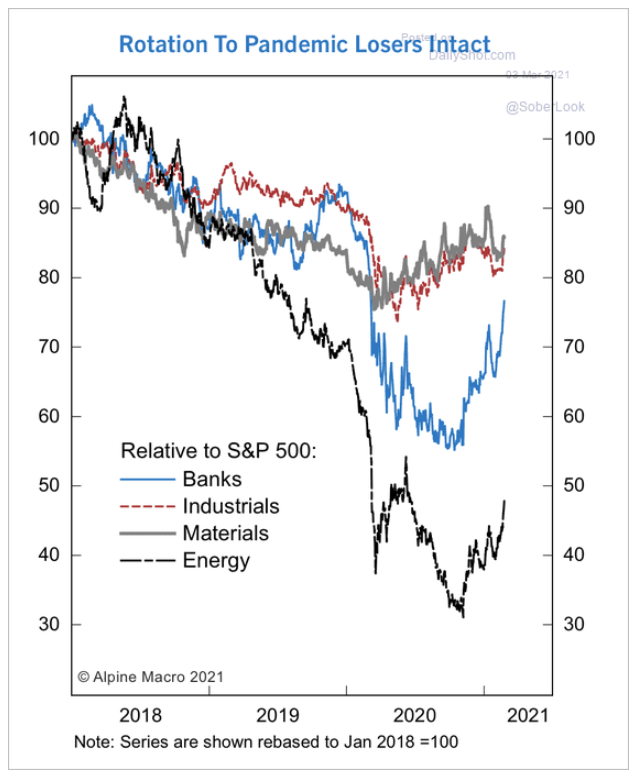

5. The reflation crowd brought some new leadership in February:

Source: The Daily Shot, from 3/3/21

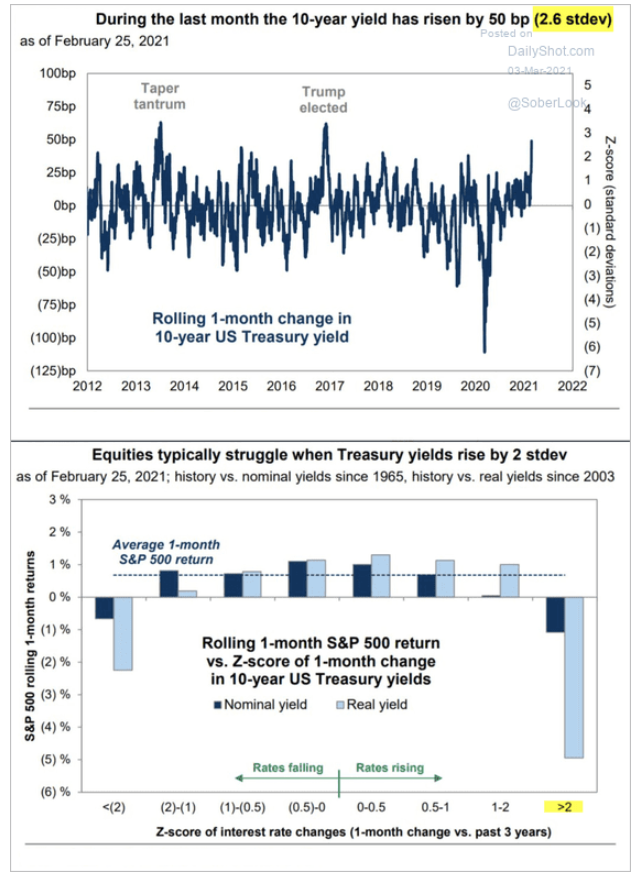

6. Historically, yield increases like we saw in February have had a negative effect on stock returns. Yet, given the near-zero start and a pandemic recovery with unprecedented stimulus, will this relationship hold?

Source: Goldman Sachs Investment Research, as of 2/25/21

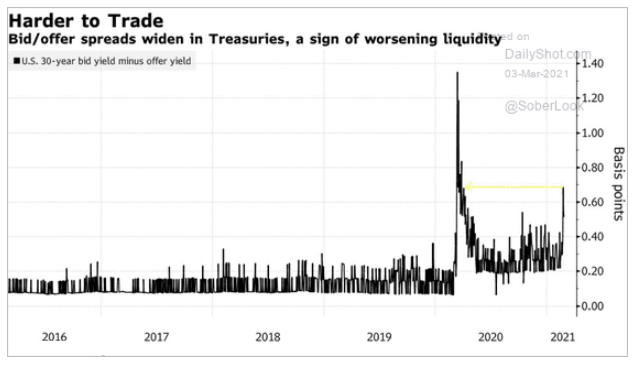

7. Ultra-low coupon bonds are harder to sell when rates rise. Remember the 10-year UST had a record-low yield of 0.052% It is almost triple this now…

Source: The Daily Shot, from 3/3/21

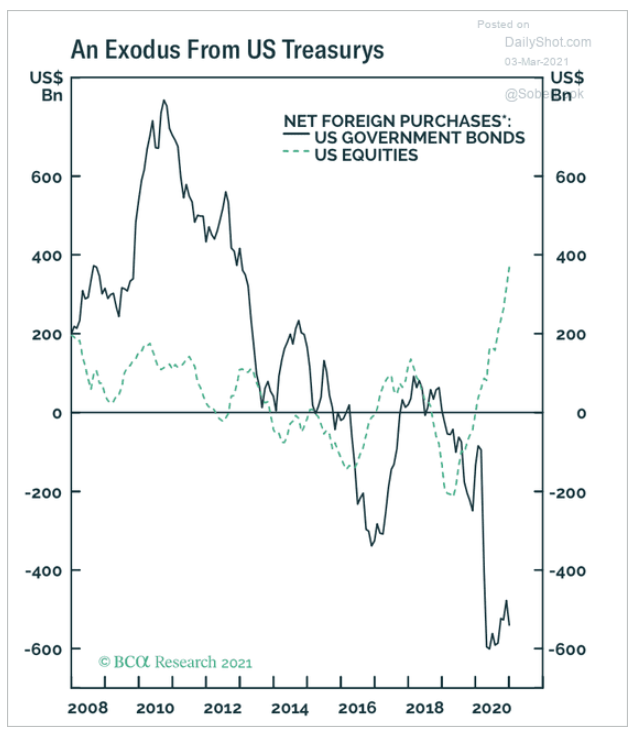

8. The near-zero rate policy had an unintended consequence: Treasury yields were too low to attract foreign buyers…

Source: The Daily Shot, from 3/3/21

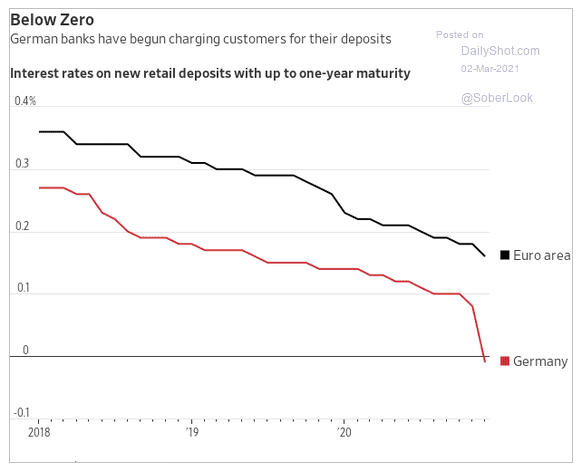

9. Negative rates are not rational over the long term. Here is one result:

Source: The Daily Shot, from 3/2/21

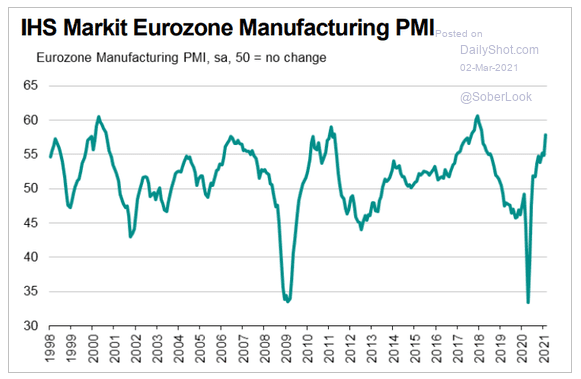

10. The manufacturing resurgence is not confined to the U.S. Here is Europe:

Source: The Daily Shot, from 3/2/21

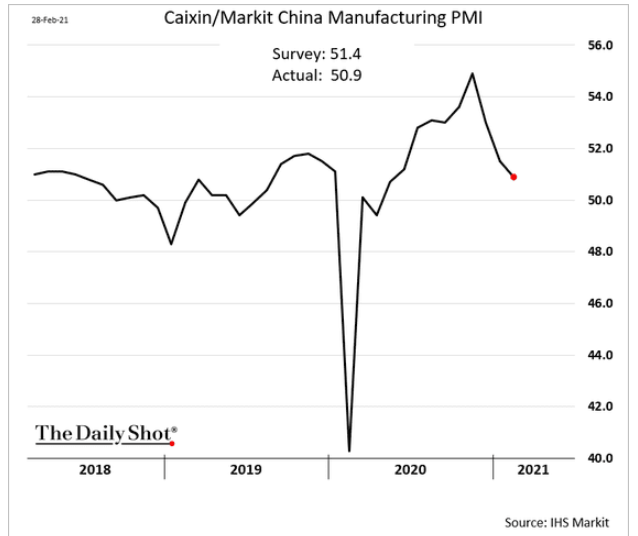

11. Now that the rest of the world has “caught up”, China’s manufacturing sector is cooling off:

Source: The Daily Shot, from 3/3/21

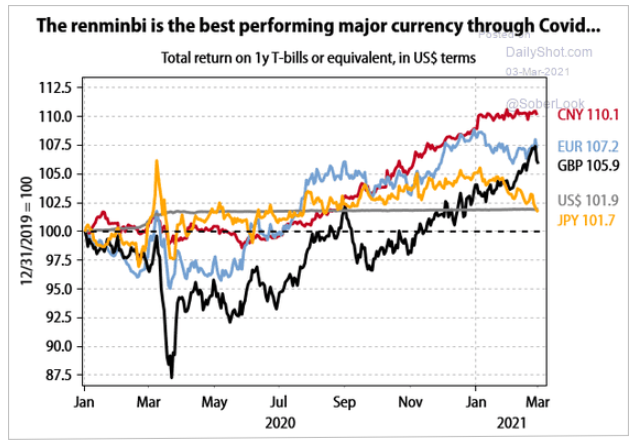

12. The Yuan’s appreciation has not helped Chinese competitiveness…

Source: The Daily Shot, from 3/3/21

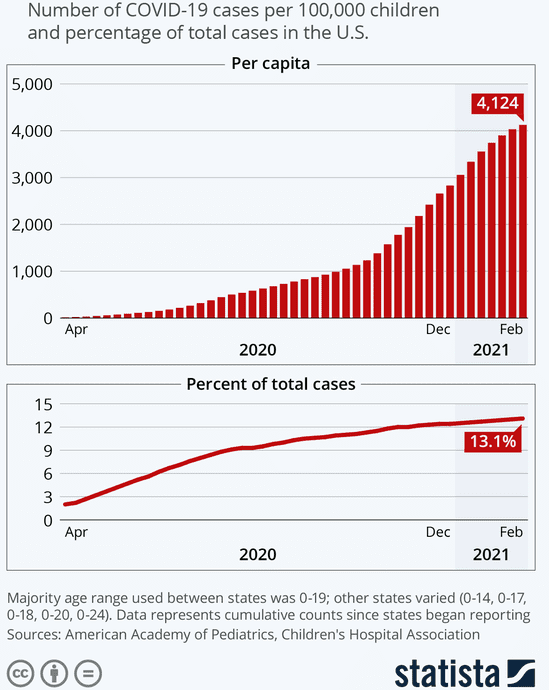

13. Children get Covid just like adults, albeit usually with much less severity, but we rarely tested them. Now that schools have started large scale testing:

Source: The Daily Shot, from 3/2/21

14. We could all add a few more humorous responses…

Source: The Daily Shot, from 3/2/21

More Articles You Might Like

Disclosure: The charts and infographics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.