BCM 1Q23 Market Commentary: Rapid Rate Hikes and their Role in the Banking Crisis

April 17, 2023 | TIMELY PM UPDATES

Market Outlook:

We remain in a somewhat uncharted investment environment with new crises occurring almost quarterly. These have been catalyzed in some part by the Federal Reserve’s obsession with inflation and their urgent and incessant hiking of interest rates. The ongoing demand/supply disruptions caused by the unprecedented COVID lock downs are also continuing to ripple through the economy.

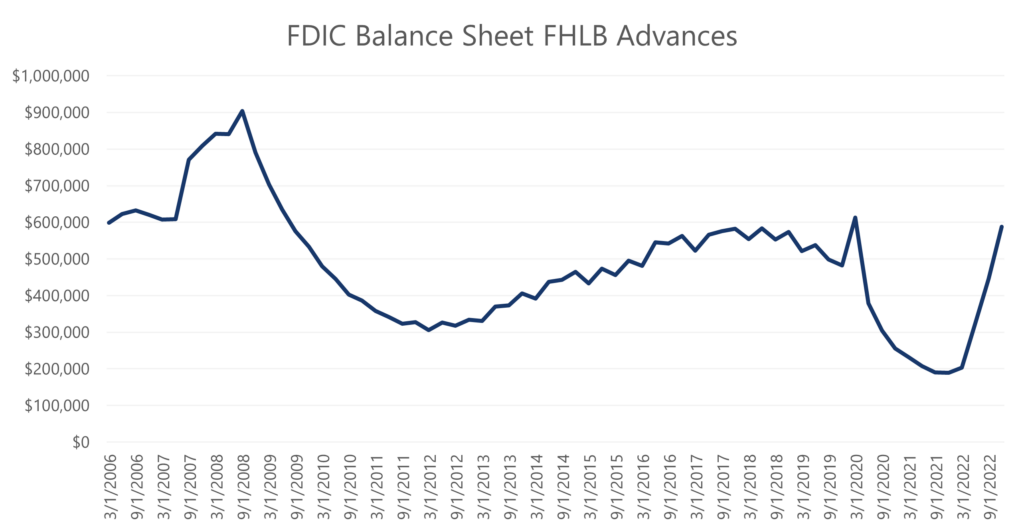

It is often said that the Fed hikes until something breaks. This quarter made good on that adage as we saw historic deposit flight and ultimately the demise of four large financial Institutions[1] and relatively widespread bank runs precipitating a huge wave of federal support.

Source: Bloomberg. Data for the period 3/31/2006 through 12/31/2022.

In our view, the Fed has done too much too fast. Catapulting interest rates 4% from near zero in a single year on an economy that was calibrated for a decade on diminutive interest rates wreaks havoc on the present value of every asset class and multiplies the interest expense line for firms with debt. The devastation of the rate hikes on bank investment portfolios was hiding in plain sight. The Federal Reserve’s own portfolio shows a loss in excess of $1 trillion—or -13%.[2]

Does the Recent Banking Crisis convert the “Rolling Recession” into a prototypical one?

Recently we have referred to the current economic situation as a “rolling recession” in which industries like housing, technology, and semiconductors experienced a revenue downturn and quickly reconfigured their capacity to the new circumstances. We believe this rolling recession environment was propelled by two major factors:

- A lack of excess leverage within the private sector (both consumers and businesses)

- Global interconnectedness and technology improving the reaction time of businesses

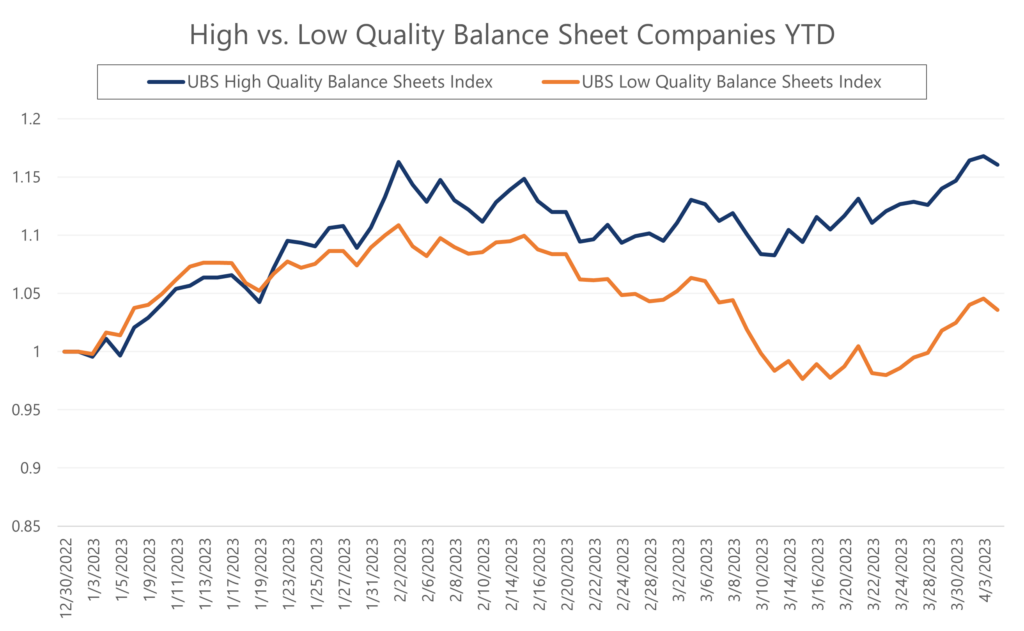

The recent banking crisis is likely to result in a tightening of credit as banks become much more precautious. The tightening of financial conditions has the potential to threaten the first of these factors as the businesses that do have debt or must access capital markets will do so at substantially elevated costs, increasing their overall business risk. Equity markets have already reflected this as businesses with the worst balance sheets have experienced a stark divergence in performance from their peers since the crises.

Source: Bloomberg. Data for the period 12/30/2022 through 4/4/2023.

Unfortunately, it’s likely that the U.S. banking industry will be permanently scarred by the recent crisis and the resultant changes in consumer perceptions. At a minimum, we expect increasing regulation, most likely rising capital and liquidity requirements, which will lower banks’ earnings and willingness to take risks.

One caveat to all of this is the Federal Reserve can quickly fix (reverse) the “unrealized losses” problem in the banking system by lowering interest rates. Towards the end of the quarter, markets did this for them as the 2-year yield fell over 100 basis points in the week following Silicon Valley Bank’s collapse.

Sectors to watch:

The U.S. office real estate sector is in distress from the combination of people working from home, partially or full-time, resulting in declining occupancy rates and the depressive effects of rising interest rates on the present value of income streams. Since Regional banks are the primary lender to this sector, there is the potential for a systematic problem.

Continued cautious optimism.

In the last five quarters, the economy has weathered a record 20% drawdown in the bond market, a similar drawdown in equities, the zombification of the housing market and commercial real estate, a war in Ukraine resulting in a surge in energy prices, the collapse of profitless unicorn stocks, the FTX scandal which imploded the decentralized finance industry, and at least 5 banks required additional capital or shut down to meet their customers’ deposits.[3]

Despite those preceding events, as well as the united efforts of Global Central Bankers to defeat inflation by slowing the economy, unemployment remains near 20-year lows in the U.S, Europe, and Japan. Clearly, today’s globally connected, rapidly adaptive, information-based economy is remarkably resilient.

The surprising resilience of the economy to the Fed’s war on inflation and all the other shocks, coupled with the ever-increasing pace of technological innovation (e.g. ChatGPT, MRNA, Obesity drugs), and a recent wave of cost-consciousness at the most influential companies (layoffs at technology firms), keeps us cautiously optimistic for equities near-term and especially optimistic long-term.

Despite our cautious optimism, we are on high alert for any signs of unanticipated economic strain or contagion. Our latest generation of Decathlon algorithms is ever more sensitive to subtle changes in market dynamics. We will respond quickly to de-risk.

Looking ahead.

We wish the Federal Reserve would have been more patient and acted in accordance with its own dogma that “monetary policy acts with long and variable lags”. Perhaps history will show that the post-Covid inflation was “transient” after all, if we assume a multi-year horizon is appropriate for the world economy to renormalize from a once-in-a-century pandemic. Now that short-term interest rates are higher than the latest inflation run rates[4], we believe that interest rates are properly calibrated, and the Federal Reserve need not do more.

With interest rates at substantially higher levels than any time in the last ten years, it’s an uncommonly attractive time for balanced investment strategies like BCM’s Decathlon strategies, which should provide a reliable core return at each risk-level, hopefully enhanced by opportunistic purchases of sector, country, and thematic ETFs.

Addendum – Rolling Recession:

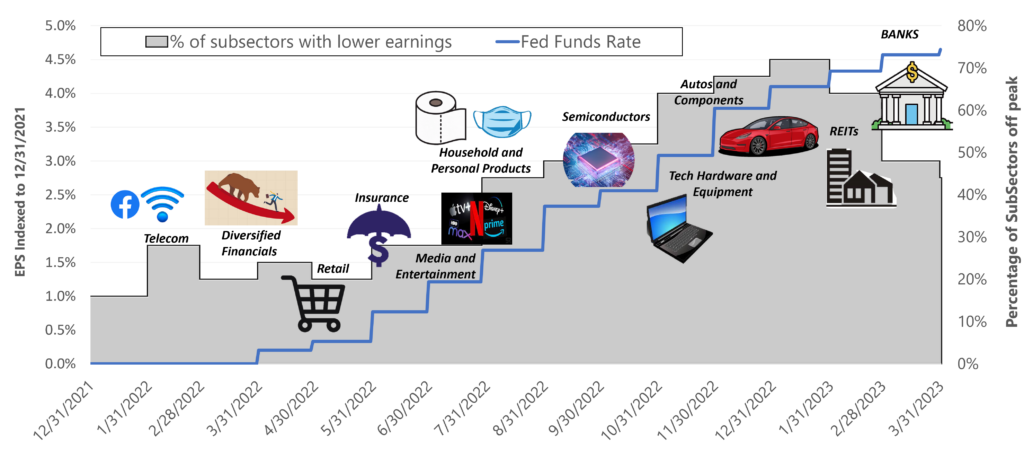

The chart below illustrates the timeline of what we have referred to as a “rolling recession”. The area in the chart that builds through time is the percentage of Industry Groups, Level 2 of the GICS classification system, whose aggregate earnings are >5% off their recent peak. The Effective Federal Funds Rate is also shown marching upwards in synchrony. The images and named industry groups are depicted on the chart corresponding with the point at which their earnings fell.

Source: Bloomberg data on GICS level 2 subindustries. 12/31/2020 through 3/31/2023. Subindustries are displayed on the chart at the period in which their trailing earnings fell >5% off their high.

Our takeaway is that some industries had more immediate supply/demand imbalances or more direct exposure to higher rates and fell into decline much sooner while other economically sensitive industries had a more delayed response as their supply chains may have had longer lead times or the impact of higher rates might have taken longer to affect them. We believe the sectors which were impacted the earliest were generally the first to take corrective measures and as a result will be the first to rebound as well. You can see some sectors did resume growth into 2023 as the percentage of sectors in decline receded prior to the March Banking crises. We also believed that sectors which had yet to be affected entering the year might be in the most danger. In many cases these “holdout” industries were simply defensive categories such as Consumer Staples and Defense companies, but banks were one notable outlier. They got an immediate benefit from higher rates in the form of higher interest margins but have recently suffered from depositors demanding higher rates as well, creating the opposite impact on their interest margins. This has been even further exacerbated in some cases by the recent deposit flight at regional banks spurred by liquidity fears which are a direct result of higher rates decreasing the mark-to-market value of their balance sheets.

[1] Silvergate Capital, Silicon Valley Bank, Signature Bank, and Credit Suisse all had their market equity wiped out between 12/31/22 and 3/31/23.

[2] As of 9/30/22, the last reported financial statements, The balance sheet of the Federal Reserve Banks had $8.634 Trillion in assets with an unrealized loss of $1.125 Trillion or 13%.

[3] Thompson, Mark. “Global banking crisis: What just happened?” CNN.com, 3/20/2023. https://www.cnn.com/2023/03/17/business/global-banking-crisis-explained/index.html

[4] Annualized CPI over a 1,3 and 6 month period is 4.4%, 4.1% and 4.3% respectively

Copyright © 2023 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The Cboe Volatility Index (VIX) is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index (SPX℠) call and put options. The “Fed Funds Rate” or Federal Funds Rate refers to the target interest rate set by the Federal Open Market Committee (FOMC). This target is the rate at which commercial banks borrow and lend their excess reserves to each other overnight.

For Investment Professional use with clients, not for independent distribution.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC

125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)